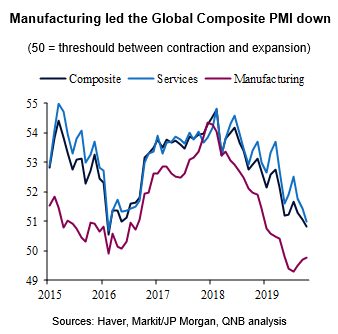

The global economy has clearly slowed over the last couple of years. During this period, global manufacturing led the way in creating demand weaknesses, eventually pushing the more resilient service sector with it. The Global Manufacturing Purchasing Managers’ Index (PMI), which captures information on output and employment, peaked in December 2017 before slowing to the sub-50 contractionary mark in May this year.

Manufacturing represents a large share of the global economy (16%), and the idyosyncrazies of the sector make it particularly cyclical. As most manufacturing products are durable goods (e.g., autos, smart phones, and computers) that retain their value for far longer than other products or services, a period of booming industrial sales is normally followed by a glut in supply and lower production levels. Over the last 40 years, this dynamic has created a series of three-year long manufacturing cycles (peak-to-peak) that are typically equally split in expansion/deceleration phases.

The latest manufacturing cycle included the expansion that started in 2016 and the current deceleration. The current deceleration has been amplified by a plethora of headwinds, including the emergence of trade conflicts, financial deleveraging in China, the US-led financial tightening and negative idiosyncratic shocks in the auto and semiconductors sectors. After 19 months of steep deceleration, however, global manufacturing is starting to produce signs of a turning point towards another period of expansion. Our analysis delves into those signs as well as the likely drivers of the upcoming expansion.

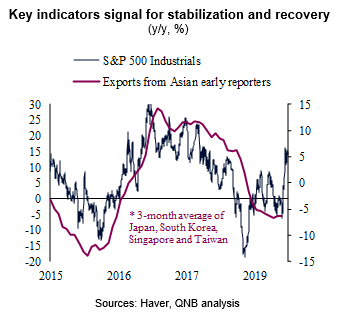

The Global Manufacturing PMI has bottomed in July and improved thereafter, nearing the expansion/contraction threshould at 49.8 in the latest October read. Other coincident and forward-looking indicators are also pointing to a stabilization or even recovery of global manufacturing. Exports of early-reporting and highly open economies of East Asia, which are a reliable gauge of manufacturing demand, finally started to stabilize after almost two years of deceleration and decline. Equity price changes of the S&P 500 Industrials, which normally lead the manufacturing cycle, have recently surged after eight months of consolidation. A sharp recovery in prices of trucking and semiconductor equipment companies also bode well for the manufacturing outlook.

The potential expansion of manufacturing activity is set to benefit from four tailwinds. First, the build up of inventories related to preventive measures against disruptions in US-China trade relations should drawdown, requiring new orders. Second, the easing of global financial conditions following the US Federal Reserve’s “dovish pivot” should start filtering through the real economy over the coming months, stimulating demand. Third, a potential “first phase” trade deal between the US and China will likely moderate uncertainty, further supporting the stabilization or recovery of capital expenditure. Fourth, the implementation of 5G technology is set to boost the battered industry of semiconductors.

All in all, we expect to see the beginning of a manufacturing rebound over the coming months, which should support a moderate acceleration of headline GDP growth in 2020. However, significant risks to the outlook persist, including a potential disruption of US-China trade negotiations and negative surprises from key central banks.

Download the PDF version of this weekly commentary in English or عربي