After the Covid-19 spread shocked investors into the fastest US equity sell-off ever recorded, the stabilization of the pandemic and aggressive policy stimulus produced an epic reversal of fortunes. In fact, over Q2 2020, major indices such as the S&P 500 and NASDAQ staged their best quarterly performance in decades, paring most of the previous losses or even in some cases reaching new all-time highs. The recovery of US equities led not only other markets but also broader global economic indicators.

As the US and other key economies “re-open,” supporting a recovery in consumption and employment, how are US risk assets expected to react? Can the bullish action persist for longer?

While appropriate policy responses should provide a stable support for the US economy and markets over the intermediate term, three factors are pointing to short-term equity market vulnerabilities.

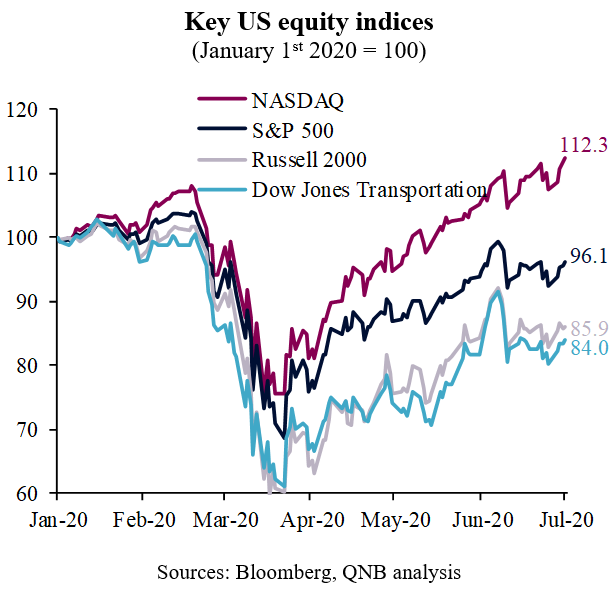

First, despite the strong performance of both the S&P 500 and the NASDAQ, a deeper look “inside of the equity market” suggests a very different picture. While the general market has been propped up by a handful of tech-intensive mega caps and biotech stocks, cyclical equities or stocks that are more sensitive to changes in the real economy are pointing to a much more challenging environment. These cyclical stocks, including small-caps (Russell 2000) and transportation players (airlines, trucking, marine transportation, railroad and delivery companies), whose performance tend to lead significant periods of sustained economic recovery, are not only lagging the general market but had recently started to stagnate and even decline.

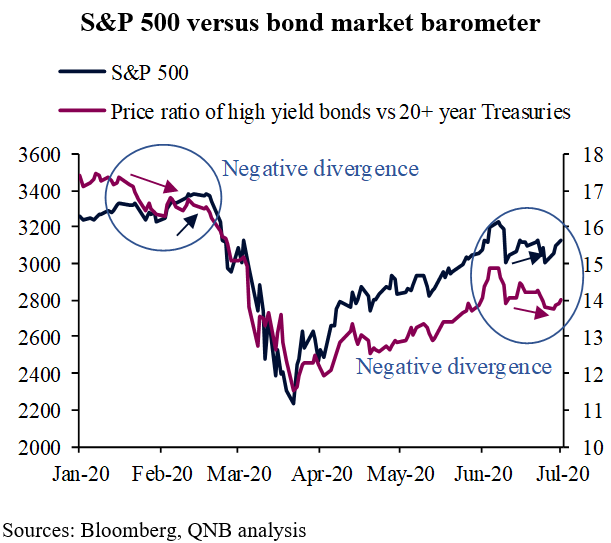

Second, the more macro-sensitive bond and commodity markets are also flashing warning signs. US Treasury yields are still low and do not point to any significant growth reflation or inflation pick up. Even more importantly, the price ratio between high yield corporate bonds and long-dated government papers started to decline, implying increased risk aversion of bond investors. Bond markets tend to lead equity markets. Similarly, commodity markets are also suggesting weakness. Despite a general recovery in commodity prices, gold, a safe-haven precious metal, has started to outperform cyclical commodities again, reinforcing the risk-off tone of the bond markets.

Third, a plethora of high and rising political, geopolitical and other tail risks are still threatening global economic conditions, making risk assets vulnerable to sudden sell-offs. The most important “known unknown” at this point is the path of the global pandemic and the potential for second waves of new cases across different countries and regions. Additional sources of risk include trade tensions amongst major economies, broad-based strategic rivalry between the US and China, a polarized election in the US and the potential for post-Covid-19 civil strife.

All in all, US equity markets are now particularly vulnerable to potential bouts of negative news flow or the materialization of risks. However, the willingness and ability of economic authorities to support the market should place a floor on risk assets. Should major financial dislocations occur again, the US Federal Reserve and the US Treasury will do “whatever it takes” to avoid a deflationary spiral of depressed asset prices, deteriorated balance sheets and private sector austerity.

Download the PDF version of this weekly commentary in English or عربي