As the majority of analysts anticipated, the US Federal Reserve (Fed) at its September meeting delivered a 75 basis point (bp) interest rate hike, thereby continuing its aggressive normalisation of US monetary policy. In this meeting, the Fed also provided a quarterly update of their own outlook for GDP, inflation as well as the policy rate. In this week’s article, we look at the Fed’s outlook.

Sources: Bureau of Economic Analysis (BEA), Fed, QNB analysis

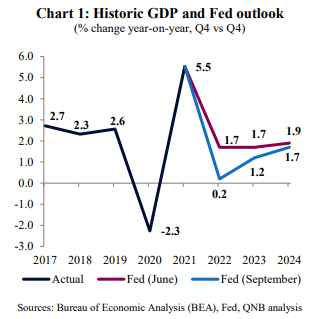

First, we consider US economic activity, as measured by Gross Domestic Product (GDP), where the Fed made a significant downward revision to its outlook. The Fed has slashed its forecast for this year to just 0.2% and to 1.2% for 2023 (Chart 1). This means that the Fed is clearly acknowledging that their aggressive interest rate hikes are likely to push the economy close to a recession by the end of 2022. In other words, they are not afraid to cause a recession, if that is what is necessary to bring inflation back under control.

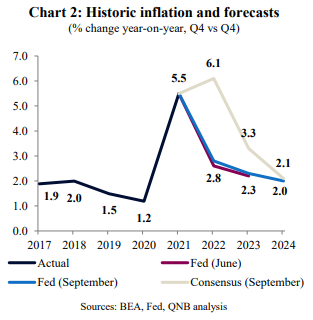

Second, the Fed’s outlook for inflation has barely changed (Chart 2). This is remarkable, given that the Fed has already started to hike interest rates aggressively and just made a significant downgrade to the outlook for GDP. It tells us that the Fed is deeply concerned about how high and sticky (i.e., difficult to lower) inflation has already become. However, the majority of professional forecasters expect inflation to remain even higher for longer than the Fed. This suggest that the Fed will potentially need to hike interest rates even more aggressively, and for longer, to ensure that inflation will fall back to their 2% target.

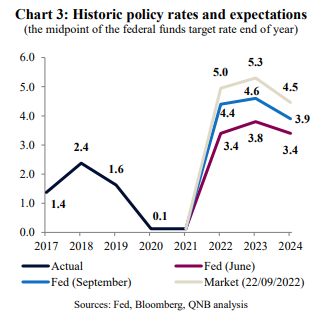

Finally, we turn to interest rates. The combination of low growth and high inflation that we have observed is called stagflation and is challenging for central banks to deal with. Stagflation forces an inflation-targeting central bank to hike interest rates enough to control inflation, despite the risks to the outlook for GDP. Given the uncomfortably high level of inflation, it is no surprise that the Fed raised their projection for interest rates (Chart 3). The Fed now expects interest rates to end the year a full 100bp higher than they did in June, with an expected peak of over 4.5% in 2023. However, markets are pricing in even higher rates, with a peak of over 5% in 2023.

The direct impact of this higher path for interest rates is that US GDP growth will continue to slow, even more sharply than we has previously expected.

However, the impact on the outlook for global GDP may be even more significant. Foreign central banks will be forced to raise their own interest rates further and faster to avoid excessive weakening of their currencies vis-à-vis the USD. This will in-turn drive their own GDP growth lower and hence pull down on global GDP growth relative to our, already weak, expectations for 2023.

Download the PDF version of this weekly commentary in English or عربي