Every summer, the US Federal Reserve (Fed) organizes a coveted economic policy symposium in Jackson Hole, Wyoming. The event is one of the longest-standing central banking conferences in the world, bringing together top economists, bankers, market participants, academics and policy makers to discuss long-term macro issues.

While the Jackson Hole Symposium always looms large in the economic agenda of investors and policy makers alike, this year the importance of the event was paramount. It followed the Covid-19 shock and months of extraordinary actions from major central banks. Moreover, it focused on the Fed’s new monetary policy framework.

After conducting a comprehensive review of different strategies, tools, and communication practices, Fed officials decided to announce adjustments to their monetary policy framework in Jackson Hole. They decided to substitute the “flexible inflation target strategy” of the past few decades to a “flexible average inflation target strategy.” The key word of the change is “average.”

Under the previous strategy, the 2% inflation target was forward looking, i.e., focused on deploying policy tools to anchor inflation expectations or future inflation, irrespectively of the evolution of prices in the recent past. Under the new “flexible average inflation target strategy,” the 2% target should be achieved over the business cycle, which implies that past inflation deviations from target have to be partially or fully compensated in the future or “avaraged.” In other words, the new approach does not have a purely forward looking character anymore. When it comes to inflation, bygones are not meant to be bygones anymore.

According to Chairman Jerome Powell, the Fed now “seeks to achieve inflation that averages 2% over time, and therefore judges that, following periods when inflation has been running persistently below 2%, appropriate monetary policy will likely aim to achieve inflation moderately above 2% for some time.”

Despite the success of the previous set up during the decades preceding the Lehman Brothers collapse in 2008, two motivations have underpinned the decision to change the monetary policy framework to an “average” inflation target regime.

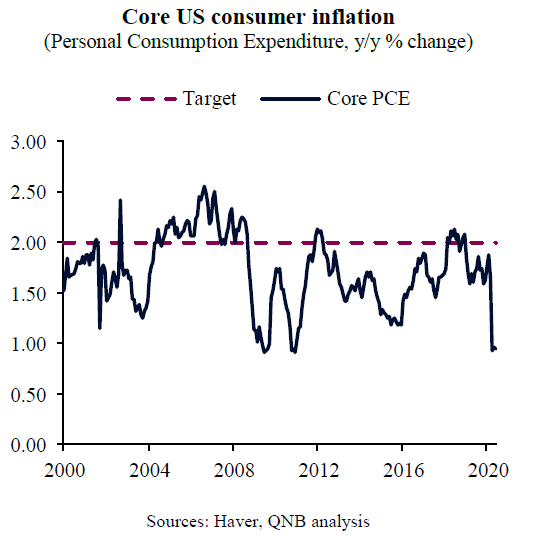

First, the Fed has been failing to deliver 2% inflation since 2008. In fact, the core personal consumption expenditure price index (PCE) has averaged 1.6% over the last 10 years, with inflation rarely hitting the 2% mark. Persistent periods of below target inflation pose concerns about the possibility of a Japenese-style deflationary trap, i.e., a negative feedback loop of low inflation, low interest rates, limited monetary policy space, deeper and longer recessions, and then even lower inflation.

Second, the Fed needed to formally review and evaluate the use of unconventional monetary policy tools, especially the extraordinary ones deployed in response to large shocks such as the Global Financial Crisis and now the Covid-19 Global Pandemic. Unconventional tools include both quantitative easing (QE or large-scale asset purchases) and forward guidance (central bank communication about the likely future path of policy rates). As the US policy rate reached the effective lower bound of close to zero in recent months, the role of unconventional tools in future policymaking is set to become even more important, especially with this new hard commitment of 2% average inflation.

All in all, the timing is favourable for a new monetary policy framework, as the Covid-19 shock imposes additional demands on economic policymakers. Under the new framework, the monetary policy stance is expected to remain accommodative or ultra-easy for longer, among others through low or zero interest rates for years and several additional rounds of QE. The level of tolerance to inflation will increase, fueling a longer economic expansion cycle. Should this new framework be successfully implemented, the US will avoid the deflationary trap, providing a policy blueprint for other deflation stricken economies such as Japan and the Euro area.

Download the PDF version of this weekly commentary in English or عربي