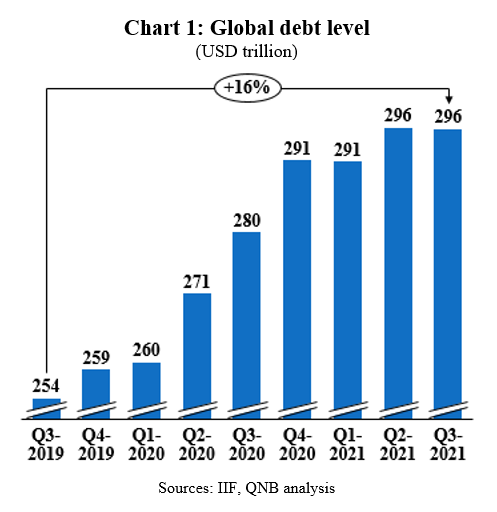

The global pandemic has caused the largest surge in debt since World War II. Indeed, according to the Institute of International Finance (IIF), global debt rose by 16% to USD 296 trillion between Q3 2019 and Q3 2021 (Chart 1), taking it to over 350% of global GDP. Unprecedented monetary and fiscal support increased both supply and demand for debt as the world was hit by a global health crisis and a deep recession. Debt levels were already elevated before the pandemic, but now policymakers must navigate a world of record-high public and private debt levels, new virus mutations, and rising inflation.

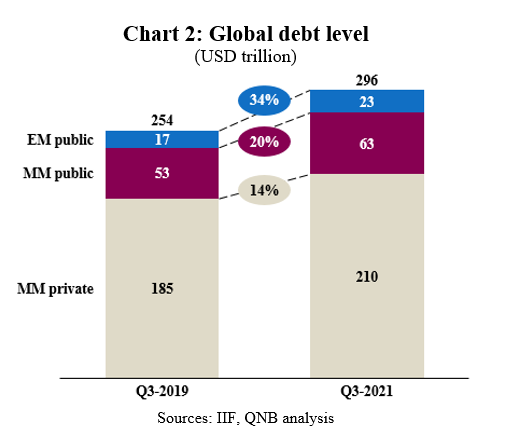

The increase in debt was broad based across government and private debt, domestic and external debt, and most countries. However, over 70% of global debt is issued by the private sector and this has increased more slowly than public sector debt (Chart 2). It is also worth noting that public sector debt has grown more rapidly in emerging markets (EM) than mature markets (MM).

This week we delve into the factors driving private debt, MM public debt and EM public debt as they have different implications for financial stability and economic growth as interest rates rise.

First, private sector debt rose by USD 25 trillion (14%) over the past two years (Chart 2). Firms and households needed government support to seem them through a sharp, but in most cases temporary, reduction in revenues and income. As a result, massive fiscal and monetary support was required. Direct fiscal support came in the form of grants, guarantees, stimulus cheques, furlough schemes and unemployment benefits. Whereas, monetary support included interest rate cuts, asset purchases and regulatory forbearance to support the supply of credit by banks. This extensive support has enabled firms and households to survive the worst of the pandemic and then recover rapidly from the pandemic in most cases. Indeed, the majority of the private sector should be able to service the higher debt burden, thanks to rising revenues and incomes as the recovery continues, even as interest rates rise. However, some redundancies, bankruptcies and debt restructurings are inevitable, especially in sectors that bore the brunt of the pandemic, such as the international travel and tourism industry.

Second, public sector debt in MM saw a larger rise than private sector debt, increasing by USD 10 trillion (20%) over the past two years. This is no-surprise as it is the other side of the balance to fiscal support provided to firms and households. Indeed, exceptional monetary policy caused government borrowing costs to fall to record low levels, making debt-financed government spending and support attractive. Most MM governments borrow at long-maturities and have relatively modest amount of debt to finance in the short-term. However, rising interest rates, and therefore debt service costs, may still force MM governments to reduce spending and investment, which will act as a drag on GDP growth.

Third, public sector debt in EM saw a larger rise than MM, increasing by USD 6 trillion (34%) over the past two years. Indeed, some EM are particularly vulnerable to the risk of sudden stops of capital flows leading to a currency crisis. Countries that have considerable foreign currency debt, overvalued exchange rates, and fragile financial systems are particularly vulnerable. Fortunately the majority of EM debt issuance over the past two years, indeed the past decade, has been in local currency rather than foreign currency. However, EM are still vulnerable to rising USD interest rates, whilst the Fed is naturally focused on domestic conditions in the US economy when making decisions. Therefore, the Fed may raise interest rates at the right pace for the US, but too fast for some EM and unintentionally trigger currency crises in the most vulnerable EM.

Tightening monetary policy and financial conditions are necessary to avoid inflation expectations becoming de-anchored in response to the highest inflation since the 1990s in many countries. However, reducing the pace of asset purchases and raising interest rates will put considerable pressure on borrowers and is a risk for financial stability given record high global debt levels.

Our view is that EM governments are most exposed to rising interest rates, which may cause a sudden stop to capital flows and currency crises in the most vulnerable EM. MM governments will also find rising interest rates uncomfortable, but the pain will be focused on the need for fiscal austerity. The majority of the private sector in MM should be able to accommodate rising interest rates, but will find fiscal austerity uncomfortable and debt restructuring will be required in some sectors. For example, many services firms in city centres will struggle as many office workers will continue to spend more time working from home in the “new normal” that is developing as the pandemic fades.

We expect some volatility in financial markets and for the most vulnerable countries, firms and households to default on their debt as interest rates rise. However, a full-blown global financial crisis is unlikely because the majority of borrowers are in a strong-enough position to handle higher debt service costs. With that said, rising interest rates and fiscal austerity will be powerful headwinds. So, we expect global GDP growth to ease back in both 2022 and 2023, slowing down from the rapid recovery in 2021.

Download the PDF version of this weekly commentary in English or عربي