The Bank of Japan (BoJ) has historically been at the forefront of radical monetary policy experimentation. In the aftermath of the Nikkei crash and the burst of the Nipponic asset price bubble of the late 1980s, the BoJ became the breeding ground for monetary policy innovation. In order to tackle a long-lasting debt deflation spiral (1987-2013), BoJ officials were the first to launch unconventional monetary measures such as zero or sub-zero policy rates and quantitative easing (QE) or large-scale purchase of domestic securities. These policies were only incorporated in the toolkit of other major central banks after the global financial crisis of 2008-09.

In 2012, Japanese Prime Minister Shinzo Abe started to promote a bold economic plan to support higher nominal GDP growth. Commonly known as “Abenomics,” the plan also aimed to push domestic prices up. More price inflation was a tall order in a country where long-lasting deflation created a “memory” of flat prices that became entrenched in the behaviours of households and corporates. Hence, “Abenomics” required ever more aggressive actions from the BoJ, including negative interest rates, broad-based asset purchases and yield curve control measures that cap long-term rates at low levels.

More recently, in the immediate post-pandemic period, the combination of robust demand growth with pandemic-related supply constraints led to a significant spike in global inflation. As a result, major central banks have enacted “hawkish” moves. The BoJ has been so far the notable exception to this trend as deflationary forces were still prevailing in Japan until early last year.

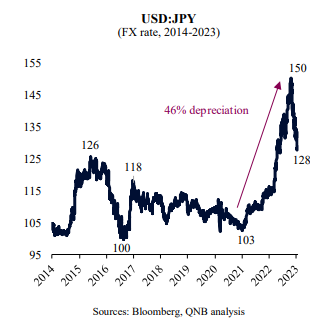

However, things started to change in recent quarters. BoJ’s ultra-loose stance amid a period of aggressive tightening by the US Federal Reserve and European Central Bank favoured capital outflows from Japan. This affected the Japanese Yen (JPY), which depreciated and, at the point of maximum pressure, in October last year, was down by 46% against the USD from recent highs. The sharp depreciation of the JPY added to other global supply-side shocks, such as the Ukraine War and chip shortages, to push Japanese prices higher.

Inflation in Japan

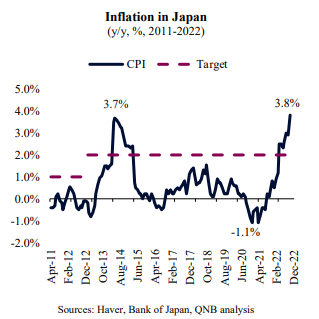

Japan’s consumer price inflation reached multi-decade highs late last year, surpassing the BoJ target for eighth straight months. As a response, the BoJ started a cautious but historical departure from radical, ultra-easy monetary policy. In late December 2022, during the BoJ’s monetary policy meeting, officials decided to change the cap for long-term rates for the first time ever, from 25 basis points (bps) to 50 bps. The decision came as a surprise to market participants as BoJ’s governor, Haruhiko Kuroda, had recently denied the idea of changing or flexibilizing the monetary policy framework. Moreover, the move came just ahead of an expected “change of the guard” within the BoJ’s senior leadership team, as the term of the governor and the Board is set to expire this summer.

In our view, this is just the beginning of a historical move. There is scope for some more significant changes in the BoJ’s monetary policy stance over the next few quarter, both before and after the “change of the guard.”

On the inflation front, there is a significant risk of further price acceleration. This is due to strengthening activity in emerging Asia, still elevated commodity prices and the lagged effects of last year’s sharp currency depreciation. This may trigger price-wage spirals that could break the persistent deflationary feedback loop of low spending, low mark ups, low wage growth and overall cost-consciousness in Japan.

In a symbolic move early this year, Uniqlo, the leading Japanese fashion retailer, announced a Japan-based staff salary raise of up to 40%. Japanese authorities are calling for similar actions from the rest of the private sector, as consumers suffer from higher imported prices and less disposable incomes.

All in all, after many years at the frontier of monetary policy accommodation, the BoJ seems to be ready to follow the path of other major central banks in tightening policy. This is expected to contribute to contain inflationary pressures. Moreover, it should also provide for a more orderly transition towards a new BoJ leadership team later this year. We expect to see further moves over the next quarters, particularly the potential abandonment of negative interest rates.

Download the PDF version of this weekly commentary in

English

or

عربي