The US Federal Reserve (Fed) is the main architect of the “Great Pandemic Reflation” (2020-21), a stimulus-induced recovery that brought the US economy back to life from the depths of a sharp downturn. Such a recovery will likely go down in history as one of the most dramatic macroeconomic turnarounds on record. In the process of igniting the recovery, the US Treasury issued papers, which were supported by the Fed’s large purchases of bonds. This created space for the market to absorb massive fiscal deficits, which were necessary for the financial relief programs during the pandemic.

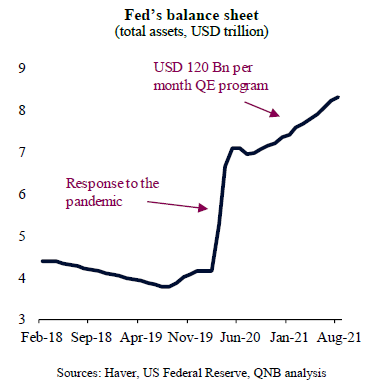

The scale of the monetary policy support was unprecedented. Interest rates were cut to close to zero and massive amounts of liquidity were injected into the financial system, either through emergency measures or through a large-scale asset purchase program (quantitative easing or QE) of USD 120 Bn a month. As a result, the Fed’s balance sheet ballooned, with its total assets growing by more than 100% in about 1.5 years, from USD 4.1 to USD 8.3 trillion.

However, as sentiment improves, investments recover and consumer demand booms, there is little necessity for the maintenance of all those extraordinary measures. This was the message that the leadership of the Fed has been trying to convey in recent weeks. In the last Federal Open Market Committee (FOMC) meeting, the Fed’s Chairman Jerome Powell changed his tone, indicating the expected timeframe of the “tapering” process, i.e., the process of scaling the support program down. According to Powell’s guidance, the Fed will likely begin to gradually reduce the amount of its long-term asset purchases next month, a process that is expected to last until mid-2022. This implies a tapering pace that reduces asset purchases by USD 15 Bn per month. With the Fed taper, the monetary policy “normalization” process officially starts.

In our view, three factors justify the Fed’s decision to start the “tapering” process as soon as next month.

First, there are no serious underlying reasons for large doses of liquidity injections in the US anymore. Investor sentiment is buoyant, financial conditions are extremely loose and the need for extraordinary deficit financing has faded. Markets are operating normally and financial institutions are not too risk averse.

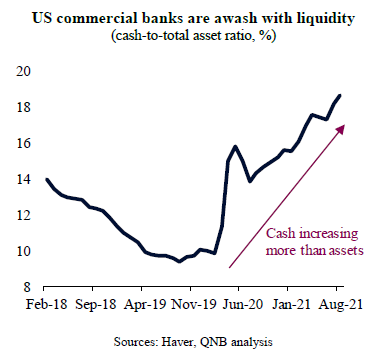

Second, to the extent that the US real economy still needs support to achieve pre-pandemic levels of employment, there is little evidence that more liquidity would be the right instrument to promote real growth and new jobs. In fact, there is evidence that money supply growth is not feeding credit growth. Excess reserves are abundant in US commercial banks. The cash-to-total asset ratio of lending institutions, which captures liquidity conditions in the banking sector, has surged to close to all time highs. This suggests that banks are now holding much more cash than they need for their commercial operations.

Third, excess liquidity in the US financial system is creating undue pressure on money market rates. Abundant reserves with banks were causing overnight inter-bank rates to drift below the Fed target and into negative territory, requiring massive intervention by the Fed to extract liquidity from the system and sustain the Fed policy rate of 0 to 0.25% per year. In recent weeks, the Fed’s actions to tackle this problem included daily reverse repurchase operations that temporarily withdrawn more than a USD 1 trillion from the system. The need for such massive operations is a clear sign that the level of liquidity is too high, and that QE is becoming counter productive.

All in all, after the full stabilization of US markets, QE is starting to create more problems than it resolves. Hence, “QE taper” is an easy point for the Fed to start its monetary policy normalization.

Download the PDF version of this weekly commentary in English or عربي