With the level of uncertainty surrounding the global spread of Covid-19 receding somewhat in recent weeks, emerging markets (EM) have benefited from a stabilization of investor risk sentiment. However, recent gains can easily be reversed should major global risks worsen, especially if a “second wave” of acute expansion of new Covid-19 cases occurs in advanced economies. New bouts of external pressure on vulnerable EM would be expected to follow any sudden reversal in risk sentiment. Hence, it is ever more important to track and analyse external vulnerability metrics of EM.

Our analysis delves into external financing requirements and foreign exchange (FX) liquidity positions of the four key emerging economies of the Association of Southeast Asian Nations (ASEAN), Indonesia, Thailand, Malaysia and the Philippines, drawing conclusions about their resilience to the current global shock.

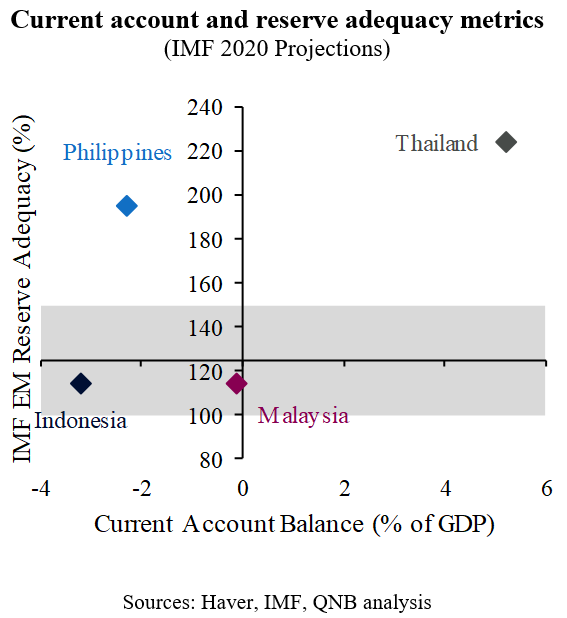

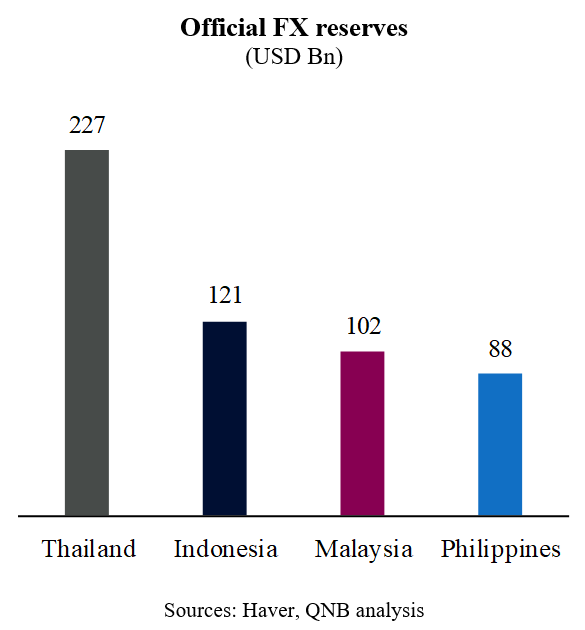

Despite a high exposure to the global economic cycle (manufacturing exports and tourism), Thailand is in a good position to weather sudden changes in capital flows. The country had run sizable current account surpluses for years and is still expected to present a healthy surplus in 2020. Terms-of-trade are also being supportive with crude oil prices and other key commodities trending downwards. In addition, Thailand has amassed USD 227 Bn in official FX reserves, which comfortably covers all relevant reserve adequacy metrics, including with 10 months of import cover, 2.7 years of short-term external debt, 35% of broad money and 224% of the composite IMF’s EM benchmark reserve adequacy ratio (IMF EM ARA metric). FX reserves are traditionally considered within adequate levels whenever they range above 3 months of imports, 1 year of short-term external debt, 20% of broad money and 100-150% of the IMF EM ARA metric.

Malaysia is another resilient ASEAN economy, even if the country is exposed to the global manufacturing cycle and negative shocks in commodity prices. The country had also run persistent current account surpluses for years, albeit not quite as pronounced as in Thailand and gradually declining since 2011. A net oil and commodity exporter, Malaysia has been negatively affected by overly weak commodity markets. In fact, the country is expected to experience in 2020 its first current account deficit in more than 20 years. Another element that exposes the country to non-resident capital flows is the fact that non-residents hold an important share of Malaysia’s local currency government bonds (about 24% of total outstanding). Malaysia’s reserve adequacy metrics are much tighter than for Thailand, with the central bank holding USD 102 Bn in total official FX reserves. This is still a relatively adequate level as it accounts for nearly 6 months of import cover, 0.8 year of short-term external debt, 22% of broad money and around 114% of the IMF EM ARA metric.

The Philippines is a net external borrower. With a large trade deficit that is currently only partially offset by sizable inflows of remittances from the community of Philippine expatriate workers, the country is expected to run a current account deficit that amounts to 2.3% of GDP. However, the deficits are mostly driven by a healthy push for much needed investment, and monetary authorities control ample FX reserves. Official reserves of USD 88 Bn account for 8 months of import cover, 4.2 years of short-term external debt, 31% of broad money and around 195% of the IMF EM ARA metric.

Indonesia is the most exposed country of our cohort to volatile capital flows. It runs persistent current account deficits on the back of both fiscal imbalances and external borrowing from the non-financial corporate sector. The current account deficit has been widening from 0.9% of GDP by the end of 2016 to an expected 3.2% of GDP this year. In addition, sensitivity to international capital flows is amplified by a significant currency mismatch, i.e., the fact that a large share of the debt from the public and corporate sectors are denominated in USD, even though a significant part of their revenues or earnings are in local currency. But it is not all doom and gloom. Indonesian official FX reserves amount to USD 121 Bn, also fulfilling the adequate criteria with 7 months of import cover, 1.8 years of short-term external debt, 26% of broad money and around 114% of the IMF EM ARA metric.

All in all, large ASEAN economies are relatively resilient to sudden changes in risk sentiment and capital flows. Such resiliency is a major source of support in a context of high uncertainty associated with the global spread of Covid-19. Buffered by moderately strong external positions, the ASEAN economies are in better shape to navigate the global shock than other more vulnerable EM.