The 2020s are proving to be a period turmoil with shocks and uncertainty. Just when the global economy was seemingly turning the page from the Covid-19 pandemic, another significant event is producing negative geopolitical and economic consequences: the Russo-Ukrainian conflict. While the seeds of the conflict have been developing for years, the bilateral disputes between Russia and Ukraine started to escalate in 2021, before breaking into an open war in late February 2022.

Following the initial military invasion, the US and the European Union (EU) decided to support Ukraine by inflicting comprehensive economic pain to Russia via embargoes, sanctions and trade bans. With this, the Russian economy was quickly disrupted and to a large extent disintegrated from the rest of the world in less than a month.

In this piece, we highlight the main points about the economic consequences of the Russo-Ukrainian conflict.

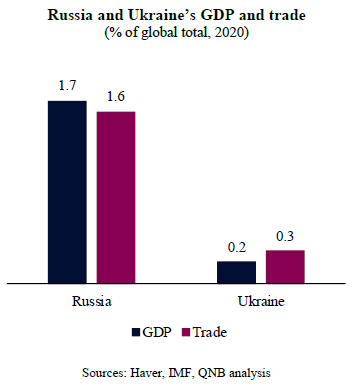

On the one hand, the direct impact of the conflict on global demand is rather limited, due to the sheer size of both the Russian and Ukrainian economies. In fact, with a nominal GDP of USD 1.5 trillion and trade flows of USD 600 billion (Bn), Russia represents less than 2% of either global activity or trade. Ukraine, a USD 155 Bn economy with trade flows of USD 100 Bn, represents significantly less. Therefore, irrespective of the magnitude of the downturn that the conflict may cause in either country, direct global demand destruction will likely be small on a global scale.

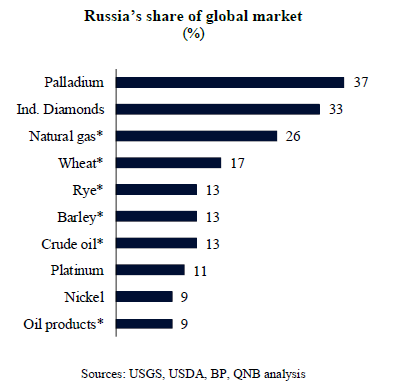

On the other hand, despite the modest nominal size of both economies, their natural resource base is large and disruptions can indirectly affect the global economy via supply shocks in commodity markets. Russia is the world’s largest transcontinental country with a territory that spans over eleven time zones and include massive deposits of natural resources, such as crude oil, natural gas, minerals precious metals and arable land. In fact, both Russia and Ukraine are important producers of fertilizers, wheat and other key products for the food industry. Hence, Russo-Ukrainian military action and sanctions are causing supply destruction at a large scale, severely stressing key commodity markets. This will produce higher global inflation and lower disposable income across countries, negatively affecting demand. This will further intensify “stagflationary pressures,” i.e., the trend of lower growth and higher prices. Vulnerable emerging markets will likely suffer from a deterioration of fiscal and current account positions. In the extreme cases, low-income countries can face mass food shortages and civil strife.

Moreover, while financial integration between Russia and the rest of the world is relatively small, the impact of commodity price spikes and asset destruction can be significant for commodity houses, brokerage firms and banks with direct exposure to Russia. Some signs of financial stress are already starting to emerge, as money market spreads are widening and Far East Asian commodity houses are experiencing multi-billion USD margin calls. If such issues continue, there could be a sudden de-leveraging in commodity markets, due to supply disruptions and collateral destruction. Cascading credit events in commodity markets could affect banks and other institutions that provide funding for such activities. In addition, Eastern European banks with exposure to Russia can also suffer significant losses, stressing the European financial system. Negative financial shocks could therefore add to the existing downward pressures on global growth.

All in all, Russo-Ukrainian military action and sanctions are largely spurring supply side shocks, rather than demand, for the global economy. This is taking place via commodity markets, amplifying inflation and creating scarcity of resources across the world. Financial risks are also increasing due to the direct and indirect effects of the shocks on financial institutions as well as on commodity traders.

Download the PDF version of this weekly commentary in English or عربي