The US Federal Reserve (Fed) continues to drive the economic agenda, setting the tone for monetary developments globally. In September 2021, after more than a year of extraordinary measures to support the economy following the pandemic shock, the Fed officially announced the start of its monetary policy “normalization” plan. Back then, the Fed announced a gradual reduction or “taper” of its USD 120 Bn per month long-term of asset purchases (otherwise known as quantitative easing or QE). The expectation was that net asset purchases from the Fed would reach zero by mid-2022, completing the so-called taper process.

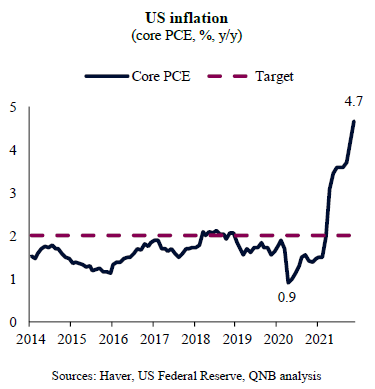

In December 2021, however, as inflation accelerated further, the Fed started a “hawkish pivot,” communicating that elevated price pressures could justify ending QE sooner than planned. In fact, the US core personal consumption expenditures price index (PCE), the Fed favourite gauge for inflation, spiked 4.7% y/y in December 2021; again well above the 2% policy target.

Inflationary developments started to indicate that ultra-easy monetary policy is no longer consistent with the magnitude, breadth and pace of the US economic recovery. US GDP is estimated to have expanded by 6% in 2021. Importantly, momentum is expected to continue strong this year, with a healthy pace of expansion in both consumption and investment propelling a GDP growth of over 5% in the US. Federal stimulus payments and social support programmes have helped to strengthen the finances of the private sector, providing a cushion of savings that are typically non-existent in the wake of a recovery. This supports high levels of consumption and activity for longer, which could lead to a multi-year period of above-trend growth.

While the US economy is still not running at full employment, given some “slack” or spare capacity in industrial production and labour markets, the growth outlook suggests that additional capacity will be filled sooner rather than later. This will increase the risks from economic overheating, eventually creating more persistent inflationary pressures.

Such risks are currently being amplified by negative developments on the supply side of key US trade partners. The spread of the Covid-19 Omicron variant in Asia, and particularly China, is starting to become a major threat to global supply chains. The current combination of a highly infectious Omicron variant with China’s “Zero Covid-19” policy could potentially lead to large-scale lockdowns and a cascade of severe shocks in supply chains and global trade. This would contribute to stress producers, create shortages and maintain prices elevated, both globally and in the US.

In light of such inflationary backdrop, Fed officials doubled down on their hawkish pivot, hinting at both an early end to QE and a much faster cycle of interest rate hikes. In recent weeks, monetary authorities even started the discussion about quantitative tightening (QT), i.e., the process of unloading some of the assets that were purchased during QE into the market. Differently than a QE taper, that only stabilizes the Fed’s balance sheet by reducing extraordinary net asset purchases down to zero; QT shrinks the Fed balance sheet with net sales of assets to the private sector. QT aims to mop up excess liquidity in the banking system, providing some much needed tightening in financial conditions.

Currently, the Fed balance sheet stands at USD 8.8 trillion, having more than doubled since the pandemic started in early 2020. During this period, excess reserves became abundant in US commercial banks, as growth in their cash holdings (132%) far outpaced their total asset growth (28%). Therefore, as banks are awash with liquidity, Fed assets can be more easily absorbed without causing undue market disruptions. Less abundant liquidity will contribute to tame asset price inflation which, indirectly, via financial and commodity markets, feeds into consumer price inflation.

All in all, the hawkish pivot is gaining momentum. In our view, QE taper will be completed in Q1 2022 and rate hikes will start as early as March. We expect four 0.25% rate hikes in 2022, one per quarter. QT should slowly start shortly after the first rate hike, potentially accelerating over Q2 and Q3.

Download the PDF version of this weekly commentary in English or عربي