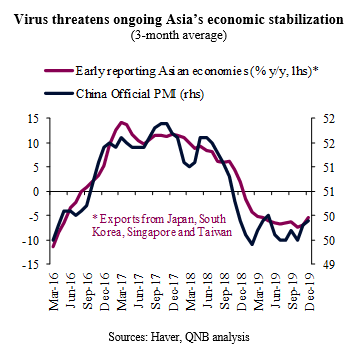

This year has started on a positive note in emerging Asia. Bullish sentiment was rampant and the global economy was set to benefit from a favourable combination of moderate growth, high employment and low inflation. China, in particular, was expected to be a key driver of an upcoming economic acceleration, with policy support spilling over to commodities, emerging markets and other open economies. In fact, leading indicators from Asia were already flashing positive signs of stabilization in recent months. But a major risk has emerged in the fallout from the worsening Wuhan pneumonia outbreak. Our analysis delves into the main economic consequences of the virus spread, discussing potential impacts, risks, policy responses and the overall effect on the outlook for emerging Asia.

Over the coming weeks, the most important channel through which Asia will be affected by the new virus is tourism. Visitor arrivals are set to plummet throughout the region, likely weighing negatively on growth in Q1 2020. At the time of writing, flights are being cancelled and administrative decisions taken to further restrict the flow of tourists from China. The Chinese government has gone as far as to cancel all group tours leaving the country, which immediately affects around 50-60% of all Chinese tourists. In addition, Hong Kong will close some border checkpoints and restrict flight and train services from the Mainland, while Malaysia, Mongolia and the Philippines have announced border or visa restrictions for Chinese nationals.

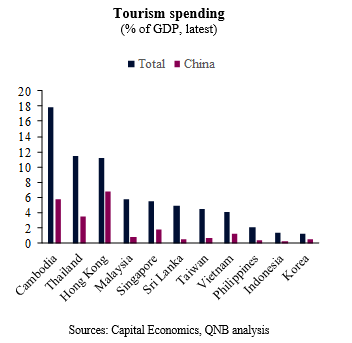

Make no mistake, tourism is a major source of income for emerging markets in Asia. Importantly, tourism spending from Chinese nationals represents a significant share of some economies, especially Hong Kong, Cambodia, Thailand, Singapore and Malaysia.

Should the virus spread more quickly beyond China and into other Asian countries, tourists from different nationalities are likely to avoid visiting the region altogether. Moreover, if the experience from the SARS outbreak in the early 2000s is any guide, the retail and services sectors should also be hit by a severe slowdown in domestic consumption. This is because people fear infection and naturally avoid going out for leisure or work in areas where the virus is present.

In the absence of a major breakthrough in treatment or a slowdown in contagion, there is a significant risk of disruption in manufacturing activity. China is the central node of Asia’s supply chains, and further extensions of the Lunar New Year holidays can impair businesses everywhere. This would likely prevent or delay the upcoming positive turn of the global manufacturing cycle towards another expansion.

The sudden reversal in market sentiment is triggering deflationary forces (e.g., severe downward pressure in key commodity prices). Therefore, we expect to see a further strengthening of the case for more policy stimulus in both Asia and the rest of the world, at least over the coming months. China, not least, is likely to deploy monetary and fiscal levers in favour of short-term expansion, even to the point of relaxing existing restrictions on unconventional credit growth.

Before the virus outbreak, we had a constructive view for emerging Asia in 2020, expecting growth to accelerate moderately to around 4.2% y/y from 3.8% in 2019. It is still too early for a more comprehensive assessment of the situation with the spread of the virus, but now we expect to see a significant slowdown in growth in Q1 2020. However, should the spread of the virus be contained over the coming weeks, we expect to see a strong rebound in activity in Q2-Q3.

Download the PDF version of this weekly commentary in English or عربي