The fallout of the Covid-19 pandemic has already produced the largest global economic shock since World War II. As governments across different continents responded to the health crisis with tight social distancing measures and lockdowns, economic activity globally plummeted at record speed in the first half of 2020.

In order to avoid a more persistent impairment on the balance sheet of corporates and households, economic authorities around the globe were quick to offer support. And there was no shortage of policy action to respond to the economic consequences of the pandemic. Major central banks cut policy rates aggressively or supported the financial system with massive injections of liquidity, preventing a disorderly dislocation of credit and equity markets. Moreover, fiscal policy became paramount as demands for financial relief surged, with governments around the world extending grants, subsidies and direct transfers to strained entities.

According to the IMF, stimulus measures as a response to the Covid-19 pandemic amounted to USD 12 trillion globally, or close to 12% of global GDP. Half of these measures consisted of liquidity support (loans, guarantees, and equity injections by the public sector) with the other half including additional spending or forgone revenue.

Importantly, however, the size and composition of stimulus measures have varied significantly across countries and geographies within the G-20. This analysis delves into the most important factors to explain such differences.

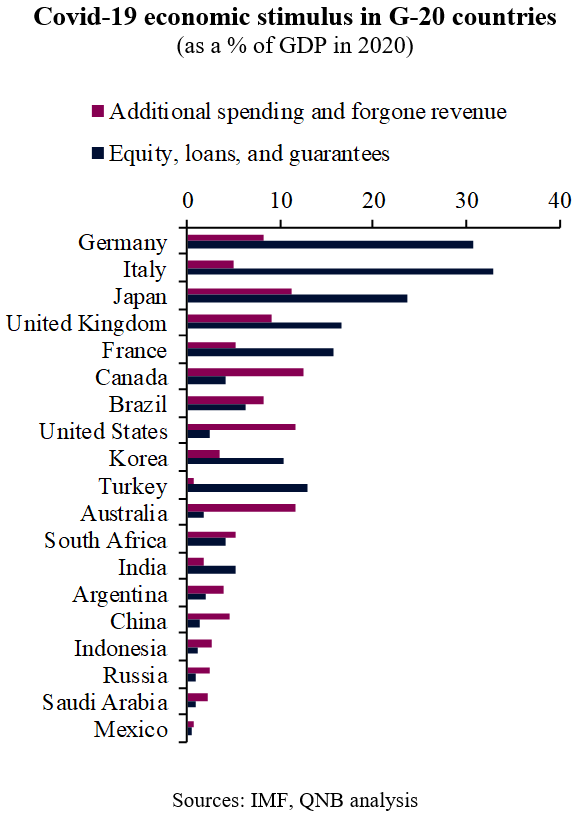

When it comes to stimulus size vis-à-vis GDP, monetary and fiscal measures varied markedly, with countries such as Germany, Italy, Japan, the UK, France, Canada, Brazil, the US, Korea, Turkey and Australia presenting much bigger stimulus packages than other G-20 countries. Two factors explain this difference.

First, stimulus demand was not the same across all countries, given that neither the severity of the epidemics nor the economic spillovers from the global shock hit all G-20 countries equally. Countries with larger stimulus tended to have had more severe waves of Covid-19 cases, longer lockdowns or more pronounced external shocks.

Second, monetary and fiscal policy space matters, as higher-income countries had more capacity to mobilize resources to support their economies. Countries with stronger institutions, more credible central banks and larger pools of domestic investors were able to launch more aggressive stimulus without the risk of causing a spike in inflation or in long-dated interest rates.

In terms of the composition of stimulus measures, discretionary economic policy actions in response to the pandemic followed country-specific institutional and political preferences. Certain countries relied heavily on off budget liquidity support and guarantees to firms as well as central bank quantitative measures (Germany, Italy, Japan, the UK, France, Korea, Turkey and India). Other countries, such as Canada, the US, Australia and China, relied more heavily on on-budget fiscal measures, including direct transfers to citizens, paid sick leave for the vulnerable, coverage of health costs for the uninsured, and tax holidays. A third group of countries, including Brazil and South Africa, relied almost equally on both liquidity measures and more traditional fiscal policies, using a plethora of government institutions to cushion the economic shock.

All in all, despite their differences in magnitude and form, G-20 stimulus policies have been so far key to stabilize the global economy, particularly after the collapse in activity in Q2 2020. Additional measures are likely to be rolled out over the coming quarters, which, along with vaccine progress against the Covid-19 virus, would be key for a full-fledged global recovery.

Download the PDF version of this weekly commentary in English or عربي