As member countries of the European Union (EU) reckon with the economic consequences of the coronavirus (Covid-19) spread, a new challenge emerges. The depressive and deflationary forces of the Covid-19 shock require once again additional policy innovation and, ultimately, further EU integration. This time, however, policy responses will have to go beyond the technocratic solutions presented by the European Central Bank (ECB).

After several rounds of monetary policy easing in Europe since 2008, policy rates are already in negative territory and quantitative easing is becoming less and less effective. The ECB alone cannot provide enough stimulus to support a prompt recovery from the Covid-19 shock. Hence, massive fiscal expansion is the new frontier for European policymaking. But innovation in this realm requires at least a partial solution to one of the most fundamental problems of the EU, i.e., how to balance a common market that is dominated by a currency union without a fiscal union.

It is no surprise that the “fiscal issue” is one of the most controversial points when it comes to economic integration. In Europe, for example, leaders of the highly productive, saving-prone economies of the North have always tried to avoid additional fiscal commitments vis-à-vis the EU. Understandably, they wanted to avoid a dynamic in which the taxpayer of low debt countries running fiscal surpluses subsidizes unsustainable spending elsewhere. On the other hand, however, European leaders of less competitive economies have often argued for the necessity of either fiscal transfers or more fiscal flexibility within the common currency area. They claimed such transfers or flexibility would be key to compensate for the lack of foreign exchange adjustments or to avoid deep economic downturns as well as “austerity traps.”

With the economic and humanitarian consequences of the Covid-19 shock and limited monetary ammunition, the great European engine seems to be moving towards looser fiscal policy across the board. On May 18th 2020, German Chancellor Angela Merkel and French President Emmanuel Macron proposed an aggressive plan of EUR 500 billion in additional fiscal spending, which should be incorporated into the EU budget and the European Recovery Fund. The Franco-German proposal served as a base for the European Commission document that is currently being submitted for discussion and approval by the EU member countries within the European Council. The final proposal included not only EUR 500 billion in grants but also an additional EUR 250 billion in loans.

The Franco-German position for additional fiscal stimulus is ground breaking for four reasons. First, it is sponsored by German authorities, which in the recent past were staunch supporters of fiscal prudence, then leading what was considered the “European austerity camp.” Second, the proposed amount of EUR 500 billion of additional stimulus was significantly higher than expectations, which were hovering around EUR 200 billion. Third, it supports an allocation of resources based on sectoral and country needs rather than a priori rules based on country size or EU contribution, implying demand-driven fiscal transfers. Fourth, allocations are meant to be budgetary grants rather than loans.

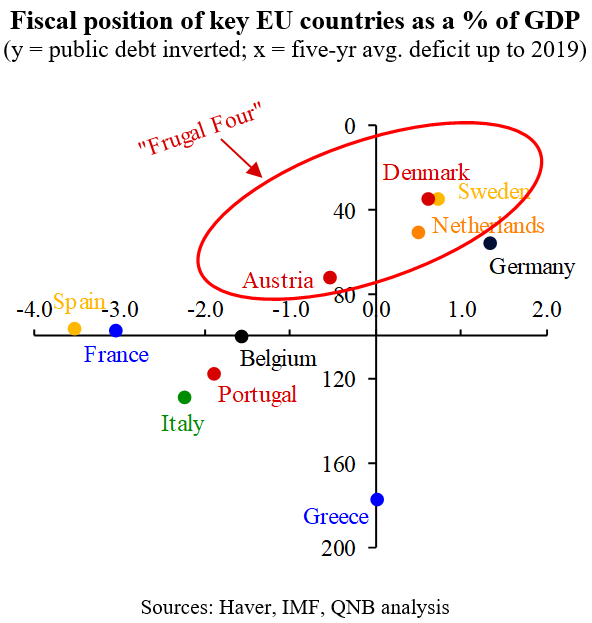

While a new round of stimulus is necessary to stabilize the EU and provide a strong base for a recovery, the proposal is already facing opposition from certain low debt countries that run fiscal surpluses or small deficits. Austria, the Netherlands, Denmark and Sweden, collectively known as the “frugal four,” are particularly opposed to the size of the package, the grant format of the support and the unclear criteria for potential disbursements. Ahead of the European Council Summit on June 19th, the group has publicly supported a smaller package, the distribution of resources as loans rather than grants and more systematic prioritization criteria for decisions about allocations.

Despite the partial opposition of the “frugal four,” we believe that the Franco-German/European Commission proposal is likely to be approved more or less in its current form sooner rather than later. The input from the “frugal four” may lead to some significant improvements, particularly in terms of checks and balances for resource allocation. But changes on magnitudes and grant/loan formats are unlikely.

All in all, the approval would be an important signal of cohesion and would likely strengthen the European economic and financial position, supporting a recovery of the EUR from its multiyear lows versus the USD, Swiss franc and Japanese yen. It would also further contribute to the narrowing of peripheral spreads. Most importantly, it would enhance the solidarity needed for the further advancement of the still incomplete European integration project.

Download the PDF version of this weekly commentary in English or عربي