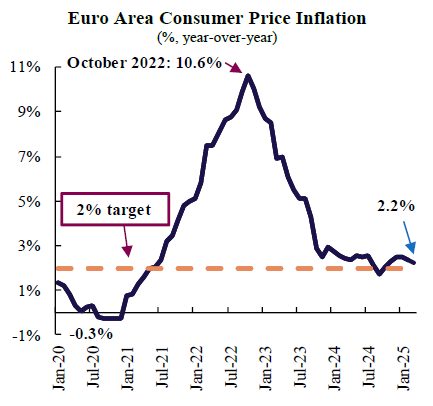

Spiralling inflation in the Euro-Zone was finally stabilized last year after an unprecedented cycle of policy rate increases by the European Central Bank (ECB). The ECB began the record tightening sequence of 10 consecutive rate hikes in mid-2022, taking the benchmark deposit rate from -0.5% to 4%. After a period of highly-restrictive monetary policy, inflation steadily descended from its peak of 10.6% towards the 2% target of monetary policy.

In June last year, with inflation half a percentage point above the target, the ECB finally felt confident that price pressures had been sufficiently subdued, and began the new phase of interest rate cuts. This gradual re-calibration took the benchmark deposit rate to 2.25% in April this year. However, further interest rate decisions will become increasingly difficult, as incoming data is weighted on a “meeting-by-meeting” basis, and policy makers balance stubborn underlying price pressures with a still pessimistic short-term growth outlook for the Euro Area.

In our view, the ECB has ample room to continue lowering its policy rate this year. In this article we discuss the key factors behind our analysis.

First, after lingering on the verge of a recession during the last two years, there is increasing pessimism signalling another year of underwhelming performance for the Euro Area as a whole in 2025. Despite encouraging growth in countries such as Portugal, Spain, Greece, and the Netherlands, overall Euro Area growth has been weighted down by the lacklustre expansions of the three largest economies: Germany, France and Italy. For the last ten months, the prints of the Purchasing Managers Index (PMI) have pointed to a stagnant bloc. The PMI is a benchmark survey-based indicator that provides a measurement of improvement or deterioration in economic conditions. The composite PMI, which tracks the joint evolution of the services and manufacturing sectors, has remained below or close to the 50-point threshold that separates contraction and expansion in overall activity, consistent with a stagnating economy.

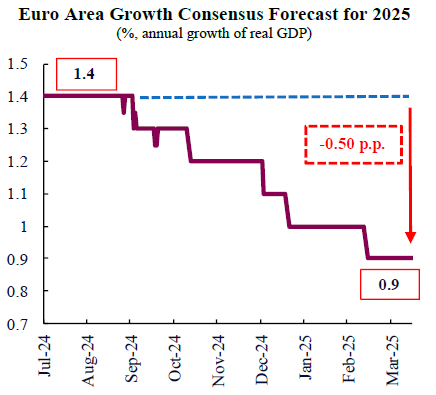

Furthermore, real GDP growth forecasts for 2025 have been on a downward trajectory since mid-2024. At the beginning of last year, the Bloombergy Survey showed an expected pace of economic expansion of 1.4%. This was encouragingly above the 1.1% annual growth average for the Euro Area in the previous two decades. However, this relative initial optimism gradually faded on the back of an industrial downturn, the enduring energy crisis and escalating global trade conflicts, reducing growth expectations to a below-average 0.9%. The weak economic outlook for the Euro Area, specially in a context of increasing protectionism and tariffs, and geopolitical ruptures, increases the likelihood of additional interest rate cuts by the ECB.

Second, price growth has been brought under control, and there is now an increasing risk that inflation drops markedly below the objective of the ECB. Inflation in services is becoming a focal point in the ECB’s policy discussions. Services are relatively less influenced by global commodity prices and other traded goods, and are therefore informative of domestic, underlying price dynamics. The latest prints of consumer prices show that monthly “core” inflation, in annual terms, continues to fall steadily towards the 2% target of monetary policy. Additionally, uncertainty surrounding the escalating trade wars is set to drag on investment and consumer demand, subduing price increases.

Diminishing wage increases will further reduce price pressures on the labour-intensive services sector. The ECB’s novel Wage Tracker Index is a measurement that gathers and aggregates data from thousands of collective bargaining agreements, providing valuable forward-looking information regarding the evolution of wages. After reaching a peak in Q4-2024, the wage tracker shows a rapid deceleration for its available horizon at the end of this year, reflecting a sharp easing of wage pressures. Some measures of inflation expectations computed by the ECB have remained below target. The Survey of Professional Forecasters by the ECB recently showed inflation expectations of 1.9% for 2026, and expectations implied by financial market instruments are already significantly lower. The marked disinflation trend justifies the ECB in further deepening its interest rate cutting cycle.

All in all, we believe the ECB will take the benchmark rate to a below-consensus 1.50% by end-2025, on the back of a balance of risks that should lean more heavily on the downside risks to economic growth over remaining inflation concerns.

Download the PDF version of this weekly commentary in

English

or

عربي