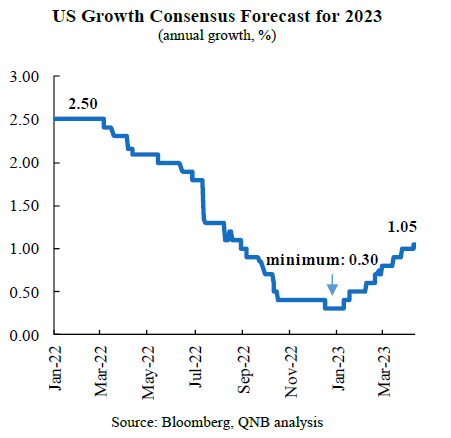

During the second half of last year a recession in 2023 for the US seemed inevitable. The economic headwinds were strong and coming from numerous flanks: high inflation eroding wages and the purchasing power of households, disrupted commodity markets with high oil prices, the beginning of a monetary policy tightening cycle by the Federal Reserve, and the removal of fiscal support for the economy. The discussions on the outlook then centered on the prospects of a “hard” or a “soft” economic landing, as the consensus growth forecast reached a minimum of 0.30% in December 2022.

But since late last year the growth outlook has improved. After the minimum of 0.30%, growth expectations gradually climbed up to 1.05% in April 2023. The improvement was not driven by any specific event that changed future expectations but by the release of stronger than anticipated activity data, evidence that the underlying economy is still robust.

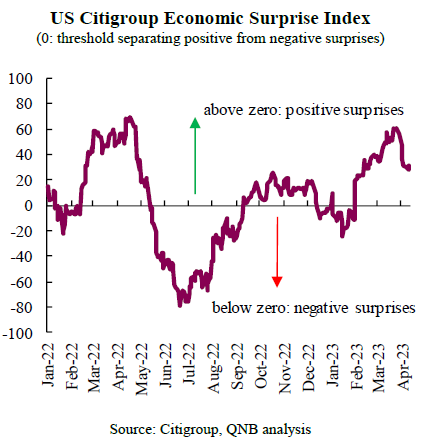

This process has been well captured by the Citigroup Economic Surprise Index (CESI), which is an appealing and useful tool to understand and summarize how economic data releases have beaten or missed expectations over a period of time. The index for the US incorporates 38 statistical indicators from a variety of key economic areas, including the labour market, real estate, industrial output, the consumer sector, and business surveys. The index is a weighted index, where each weight depends on how much the respective indicator can affect financial markets. Indicators with a higher weight impact financial market more than indicators with lower weights. The index also considers the timeliness of the information. Indicators from the last 90 days have a lower weight than more recent news and information. Values above zero indicate positive accumulated surprises, while negative values imply that data releases have been worse than expected.

The index shows that positive surprises have not been isolated events. It began an upward trajectory in January this year, entered positive territory at the beginning of February, and climbed to a new peak in March. The service sector, which accounts for 77% of the economy, has been a key source of positive surprises. Business surveys have beaten expectations in the last few months, pointing towards an economy that remains resilient.

In our view, there are three factors that explain the relative US economic resilience shown by stronger than expected data.

First, household balance sheet data show that consumers still have a significant buffer of savings, and are able to tap into these resources to support consumption. In aggregate, households have US$ 18.2 trillion available in deposits. Interestingly, even households at the bottom 60% of the income distribution benefit from high cash levels, as they hold between US$ 3,000 and 12,000 in excess savings.

Second, energy prices have come down significantly from the average levels registered last year, providing additional room in terms of disposable income. Consumer energy expenditures are roughly 5% of disposable income for the average household, and reach 7% for lower income households. WTI oil peaked at a monthly average of US$ 114.6 per barrel (p/b) in June of last year, before stabilizing around US$ 80 p/b during the winter months, the time of the year when energy consumption is the highest. The fall in oil prices has brought down gasoline costs by 25% over the same period, leaving more resources for additional consumption.

Third, labor markets remain strong, despite anedoctal cases of high profile layoffs in large US technological companies. Job creation continues to outpace population growth. Importantly, nonfarm payrolls, a key measure of total employment, added 504 and 311 thousand jobs in January and February, compared to the pre-pandemic monthly average of 177 thousand during 2018-2019. The unemployment rate stands at historically low levels of 3.5%. Stable labor markets and abundance of job opportunities decrease uncertainty for households, and provide another pillar to sustain higher levels of consumption.

All in all, economic data releases have on average been consistent in giving positive surprises this year, which have resulted in an improvement of the US growth outlook. We expect the US economy to grow by 1.1% this year. While this is not a strong showing, it is still far from indicating a recession. This substantiates the resilience of the US economy, leaving it on a better standing to withstand any new potential shocks. This is particularly important in a context where stress in the banking sector could influence the outlook over the next few quarters.

Download the PDF version of this weekly commentary in English or عربي