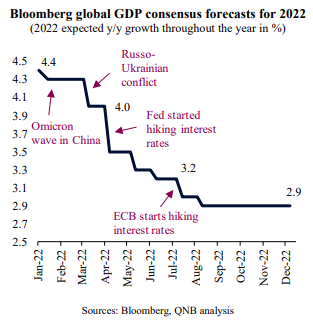

This closing year started on a positive note for the global economy. Market sentiment was exuberant as the recovery from the depth of the pandemic continued, signalling another bout of strong performance in major advanced economies and selected emerging markets (EM). In fact, at the beginning of the year, Bloomberg consensus forecasts pointed to a robust global growth of 4.4% in 2022.

However, global conditions took a dramatic turn for the worse early in the year as China’s Zero Covid policy led to significant lockdowns in the country. The Russo-Ukrainian conflict added another layer of complexity to the macro picture with supply chain bottlenecks for energy and food. This further accelerated already elevated inflation across most advanced economies. To tackle high-rising inflation, ultra-easy policy measures taken during the pandemic started to be aggressively reversed globally. As a result, growth expectations were repeatedly revised downwards while inflation expectations were revised upwards, creating a rare macroeconomic shock that was last experienced in the 1970s.

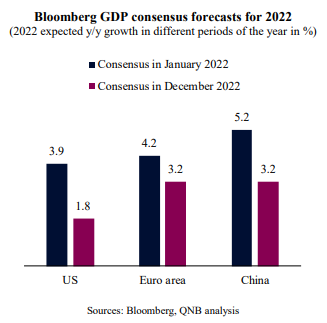

The estimated global growth of 2.9% for 2022 is a significant setback, particularly given both the initial growth expectation of 4.4% and the long-term growth average of 3.4%. Importantly, this year’s weakness interrupted the strong recovery witnessed in the second half of 2020 and in 2021, placing the global economy 5% below the pre-pandemic economic trend. The deterioration was broad-based, affecting all major economies, including the US, the Euro area and China.

In this article, we dive into the key events of 2022 that caused such downward revisions in global growth expectations.

Starting with China at the beginning of the year, the Omicron wave of Covid-19 cases required hard lockdowns and extensive social distancing measures to supress the virus under their Zero Covis policy. This included the unprecedented lockdown of millions of people in Chinese tier-1 cities for almost two months and tight restrictions on movement in other regions. Lockdowns covered areas that generate 40% of China’s GDP and represent 80% of its exports. Restrictive bank lending despite higher money supply, a clampdown of an overleveraged real estate sector as well as aggressive regulation across the tech industry led to the sharpest economic slowdown by the country in more than 30 years.

Lockdowns in China amplified the magnitude of supply chain shortages that emerged during the pandemic across the globe. New consumer behaviours amid the pandemic and direct fiscal transfers to households created a temporary demand boom for manufacturing products that spilled-over into an excess demand for commodities when supply was constrained.

The Russo-Ukrainian conflict added to the commodity market’s disruption by putting additional pricing pressure when stockpiles were at historically low levels. Consequently, energy and food prices spiked. Brent crude oil prices averaged USD 100 per barrel for the year, the highest level in a decade and close to the record levels seen in 2011 and 2012. Embargos, sanctions and boycotts disrupted Russian gas flows to Europe, igniting an energy crisis that started to cause a recessionary environment in parts of the continent. At the same time, inflation unexpectedly reached multi-decade highs in the US and the Euro area.

Higher prices lowered disposable incomes and pressured central banks to act more aggressively, making up for the lax approach adopted since the pandemic, when ultra-easy policies were maintained even as the first signs of price acceleration emerged. The US Federal Reserve (Fed) engaged in an aggressive hawkish policy stance and hiked interest rates seven times, taking the Fed Funds Rate from 0-0.25% to 4.25-4.5%. Similarly, the European Central Bank (ECB) raised rates four times, taking the Discount Rate out of negative territory for the first time in seven years to 2%. Moreover, after a decade-long period of liquidity injection and quantitative easing, both the Fed and the ECB tightened or even reverted the approach to manage their balance sheets.

Tighter financial conditions in the context of high global debt levels led to lower credit expansion, which constrained access to capital and dragged both consumption and investment, negatively affecting economic activity.

All in all, despite a promising start, the year 2022 was dominated by macro challenges that led to sub-optimal global growth. Hopefully, however, for 2023, most of the causes of the global slowdown – lockdowns in China, continued supply chain constraints, high commodity prices, accelerating inflation and aggressive central banks – are set to moderate or revert.

Download the PDF version of this weekly commentary in English or عربي