China is often referred to as a massive growth engine. In fact, from the Great Financial Crisis of 2008-09 to last year, China was responsible for 42% of the total global economic expansion. In 2019 alone, China’s growth added to the world an amount equal to Switzerland’s total GDP or more than USD 700 Bn. Importantly, expanding Chinese aggregate demand had a high multiplying effect, spilling over to commodity prices, emerging markets and other open economies.

The size and impact of a robust post-Covid-19 global economic recovery will rely to a great extent on China’s performance. Hence, investors and policymakers are constantly looking for emerging signs of strength or weakness from the Asian giant. This begs the questions: as China moves further away from the epidemic’s peak and lifts comprehensive social distancing measures, how is its economy performing? What can we expect next?

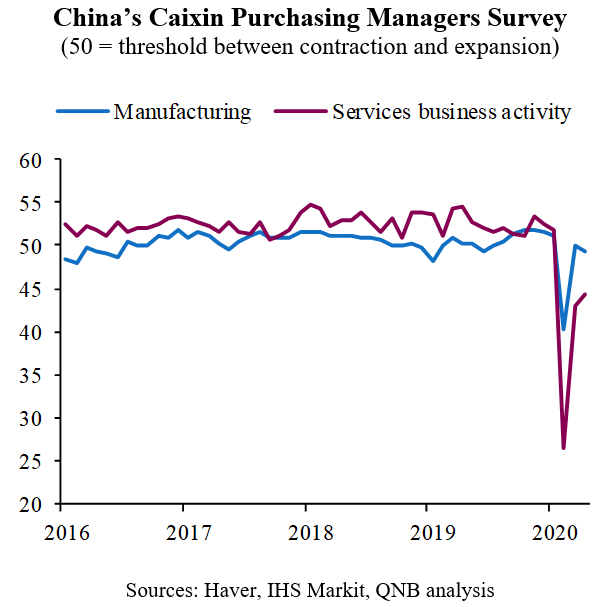

At the time of writing, a tentative economic rebound seems to be taking place in China, after a sharp contraction in Q1 2020, when GDP fell by 6.8% year-on-year (y/y). Key coincident indicators point to a significant stabilization of both output and demand. The headline Caixin Purchasing Managers Survey (PMI) recovered to 47.6 in April from a record low of 27.5 in February. While still in contraction territory, the composite PMI level is getting close to the 50 mark, which traditionally separates a contraction from an expansion. Similarly, industrial production staged a 3.9% y/y growth in April from a 13.6% y/y decline in February. Retail sales, a gauge for China’s consumer economy, stabilized in April, contracting only 5.3% y/y versus a dismal 38.9% depression in February. Moreover, credit growth picked up and high frequency highway traffic volume during working and rush hours snapped back to normal levels.

While such signs of economic recovery in China are encouraging and positive for the global macro backdrop, three factors point to a more paced gradual recovery rather than a rapid V-shaped rebound.

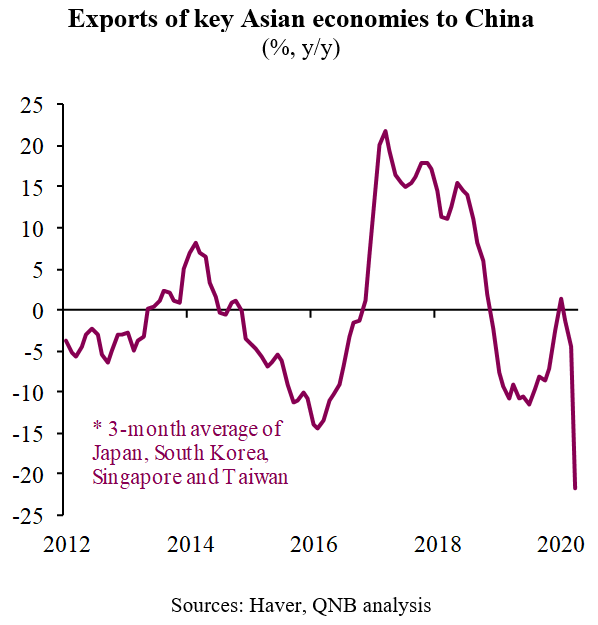

First, on the supply side, activity data suggests that a large stock of inventory has been building up rapidly over the course of the last few months. Industrial inventory of finished products soared by 15% y/y in Q1 2020 from 2% y/y in the previous quarter. As a result, a drawdown of existing inventory will be needed before a more sustained phase in business expansion occurs. Remaining weakness in the industrial sector can also be attested by the low overall value of exports from key Asian manufacturers to China. Given the nature of regional supply chains, a material manufacturing rebound will be led by a pick up in Chinese regional imports.

Second, on the demand side, lower disposable income of households and more persistent behavorial changes of individuals are set to maintain a cap on consumption growth. Income losses from Q1 as well as higher levels of unemployment are expected to increase the marginal propensity of Chinese households to save. Moreover, individual tendency to maintain social distance for longer will prevent consumers to undertake leisure activities. This will continue to weigh on consumer-facing service sectors such as accommodation, catering, tourism and offline retailers. Highway traffic volumes during non-working hours are still significantly down from normal levels all across China. Not surprisingly, PMI service data still points to depressed levels of activity in consumption-related businesses.

Third, on the external side, weak global demand due to the Covid-19 pandemic and continuous uncertainty about the bilateral relationship with the US produce additional headwinds. The export channel growth driver will likely be temporarily closed to China until all major economies start to recover and open up. Moreover, global uncertainties and the conflicts with the US invoke caution in Beijing. Hence, the Chinese government wants to be prudent and save policy space/stimulus ammunition in case bilateral negotiations turn sour or exogenous shocks hit.

All in all, the Chinese recovery should continue but lingering headwinds will likely prevent a more desirable V-shaped recovery. However, despite the magnitude of the shock and all its consequences, the dynamism of the Chinese economy is already starting to show signs of a recovery. A gradual expansion of domestic demand is still expected to generate positive growth of around 1.5% y/y in 2020.

Download the PDF version of this weekly commentary in English or عربي