The dominant global macro theme for the last year and a half has been the economic recovery from the depths of the Covid-19 pandemic shock. In fact, with a GDP growth of 5.9% in 2021, the global economy witnessed the fastest expansion in activity in almost 50 years. The Global Manufacturing Purchasing Managers Index (PMI), which is a coincident indicator for global economic activity, has been in expansion territory for 21 consecutive months, and it remains strong as per the latest print of March 2022, demonstrating the resiliency of the global economic recovery.

However, despite the strength of the global recovery, new macro drivers are emerging, placing downside risks to the economic outlook. In this piece, we highlight two major macro drivers that are expected to weigh on the global economy over the next several quarters.

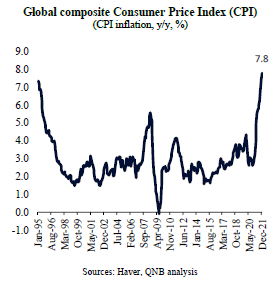

First, global inflation accelerated rapidly to multi-decade highs, threatening the prospects for price stability. This is the result of Covid-19 related supply chain constraints, strong stimulus-driven demand, low labour participation rates and ultra-tight commodity markets.

During the pandemic, as the consumption for services was limited by lockdowns and social distancing measures, direct fiscal transfers to households created a demand boom for manufacturing products. The secondary effect of this was a strong demand for commodities, particularly metals and, subsequently, as mobility started to recover, also energy. On top of that, the negative supply-side shock from the Russo-Ukrainian conflict added to the problem by disrupting commodity markets, including not only metals and energy but also food products and fertilizers. This took place when the Bloomberg Commodity Index was already advancing to new highs and stockpiles of certain key commodities were at historically low levels. Russia is a major exporter of key commodities across all segments (i.e., energy, metals and grains) and the introduction of embargos, sanctions and trade bans affect the availability of these goods, creating price pressures.

High and rising prices will lower disposable incomes globally, placing downward pressure on consumption growth. In low- and middle-income countries, the potential for chronic food inflation or food shortages can even trigger a wave of civil strife and political risk events. In the lower range of the income per capita spectrum, this may even potentially lead to a fresh wave of famine and hunger.

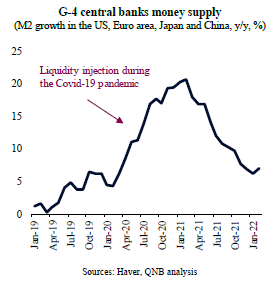

Second, liquidity conditions are tightening and this will create additional downward pressures on global growth. After a period of plentiful liquidity in all major markets, following pandemic policy support programs, the tide is starting to turn, resulting in tighter financial conditions. Money supply growth has been slowing down significantly over the last several months.

In addition, major central banks have started to “normalize” their monetary policy, aiming to strengthen more comprehensive campaigns against inflation. Many central banks are believed to be “behind the curve” when it comes to securing their inflation mandate. In the US, for example, the last time inflation reached current levels was in January 1984, when policy rates were at 9.56% per year, versus the current rate of 0.25%.

We expect the US Federal Reserve (Fed) to conduct two rounds of 50 basis points (bps) hikes and at least six more rounds of 25bps hikes in 2022 and 2023. Moreover, the Fed is set to start a process of “quantitative tightening” (QT) or letting the balance sheet shrink by around USD 95 billion per month. Other major central banks are in a similar situation and either already started their own normalization process or will start it sooner rather than later.

As liquidity is withdrawn from the global economy, credit events are likely to increase sharply. More credit events and tighter liquidity conditions will spillover into risk appetite, leading to a sharp slowdown or even a contraction of global credit. Less credit will weigh on consumption and investment, containing GDP growth.

All in all, the headwinds from these two major macro drivers will cause more damage to the global outlook, despite still high consumption in the US. Hence, we expect to see a significant slowdown of growth across several markets, including the US, the Euro area and China.

Those trends led the World Bank and the International Monetary Fund (IMF) to revise their growth forecast from 4.1% and 4.9%, respectively, to 3.2% and 3.6% for 2022.

Download the PDF version of this weekly commentary in English or عربي