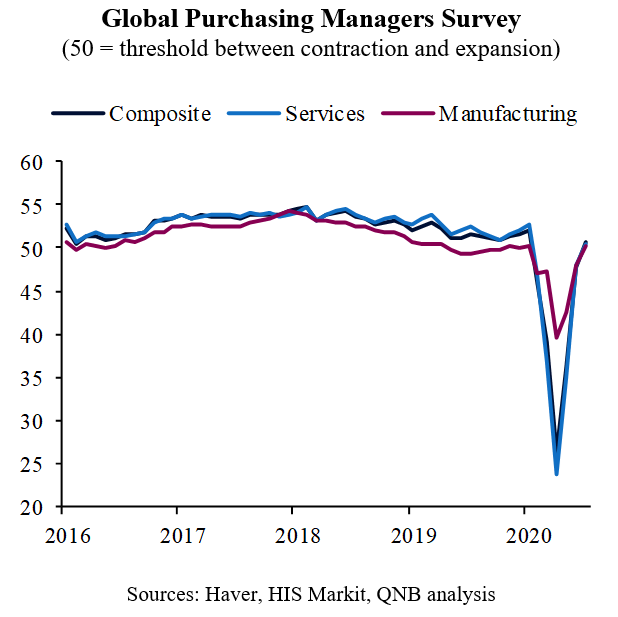

A cautious optimism has continuously marched ahead over the last few months, as several advanced economies gradually “re-opened” their activities, hopefully leaving the peak of the pandemic shock behind. The stabilization of the Covid-19 spread and aggressive policy stimulus produced a significant reversal of economic trends, from a rapid but deep depression to what so far appears to be a recovery to close to previous levels in the medium term. At the time of writing, a broad based stabilization is taking place globally, igniting not only the badly hit service sector but also manufacturing, as expressed by the bounce in surveys with purchasing managers (Purchasing Managers Indices or PMIs).

Several months into the tentative rebound, this analysis delves into the figures of one of the most reliable gauges of real activity, i.e., global trade.

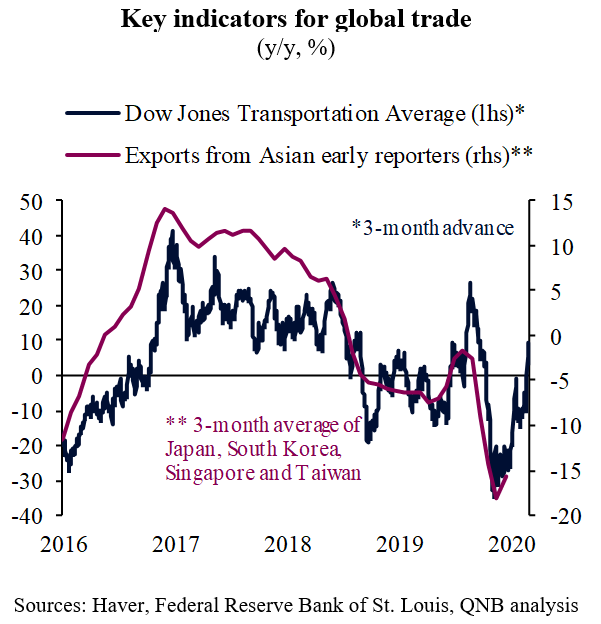

Exports of early-reporting and highly open economies of East Asia, which are a key coincident indicator of overall trade dynamics, are so far down 11% y/y in July 2020. While this represents a significant downturn, it is far off from the collapse experienced in April, when y/y exports crumbled by more than 19%. Moreover, a smoother trend-line of 3-month average y/y figures point to the beginning of a turning point for exports, with the trend gradually moving upwards after the sharp crash.

Most importantly, however, four reasons point to promising signs that the turning point in global trade will gain momentum.

First, last month (July), exports of early reporting East Asian economies expanded on a month-on-month basis for the first time since January 2020. After 5 months of decline, USD export values from key Asian economies increased by 6% from June to July. Exports for Asia and Europe, in particular, have picked up substantially, suggesting a quick “re-opening” rebound.

Second, transportation activity, a key leading indicator for incoming demand and exports, had also started to point to additional strength. The Dow Jones Transportation Average, an equity index comprised of airlines, trucking, marine transportation, railroad and delivery companies, whose performance traditionally leads exports by 3 months, are not only signalling for the beginning of a recovery but for a significant acceleration over the next few months.

Third, a backlog of new orders is set to reach producers globally, after several months of supply-side disruption and inventory drawdowns. The Covid-19 shock affected the export-intensive manufacturing sector after 19 months of steep industrial deceleration, when the manufacturing cycle was ripe to turn into expansive mode. The build-up of inventories related to preventive measures against disruption in US-China trade relations in 2018 were gradually drawn down over 2019, requiring new orders and an increase in trade flows. The pandemic did not completely wipe out the need for those new orders.

Fourth, the pandemic has accelerated secular or long-term consumption trends that are traditionally export-intensive, such as software, electronics and communication equipment. Working from home requirements are propping up the demand for hardware and electronics. The adoption of 5G technology and the required IT infrastructure for its proper functioning is boosting demand for the semiconductor industry.

All in all, trade is so far reinforcing other positive signs of an early recovery from the global recession. Should the pandemic stabilize further and extraordinary policy support continue, activity and trade will likely accelerate even more.

Download the PDF version of this weekly commentary in English or عربي