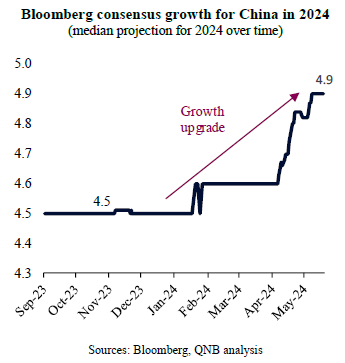

Early in the year, China was one of the main reasons for relatively tepid global growth projections for 2024. After almost three years of volatile growth and unexpected headwinds coming from China, negative narratives from investors and analysts started to intensify, dominating the country agenda. In fact, the Bloomberg consensus forecasts pointed to a slow 4.5% Chinese growth for 2024, significantly below last year’s 5.2% growth and the long-term 10-year average of 6.2%.

However, in recent months, the China “doom and gloom” story has been challenged by a combination of positive data surprises and firm government stimulus measures. This has so far produced a significant upward revision in growth expectations for the country this year.

After the latest rounds of GDP growth revisions and upgrades, is there still scope for further upside for Chinese growth this year? Are all the good news already discounted? Can the country sustain the momentum for much longer?

In our view, there is still room for further upside in growth projections for China this year, as the build-up in momentum and the improvement in overall sentiment can produce above target (5%) growth. Three main factors sustain our view.

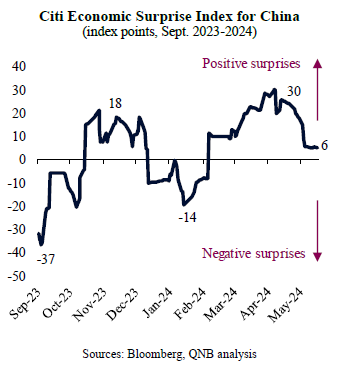

First, data is already surprising to the upside and there are indications that the positive momentum could continue for a while, leading to new growth projection upgrades. The Chinese economy expanded at a year-on-year pace of 5.3% in Q1 2024, beating analysts’ forecasts of about 4.8% by a significant margin. Moreover, the flurry of negative economic data surprises in China seems to have exhausted itself in September 2023 and January 2024, pointing to some pessimism that is already producing positive surprises.

This is reflected by the recent moves in the Citi Economic Surprise Index for China, a timely figure that measures the pace at which economic indicators are coming in above or below consensus forecasts. For the first time in more than nine months, data has been mostly producing positive surprises since for a period longer than two full months. These types of turns tend to imply that projections are currently still too conservative and should start to be revised upwards over the coming months.

Second, the Chinese government decided to step up policy stimulus and take more aggressive measures to support the economy. In recent quarters, policy actions included a few rounds of interest rate reductions, liquidity injections and fiscal spending in infrastructure projects. There was also a host of more than 100 new initiatives targeting support to the private economy, consumer spending, and foreign direct investments. On top of all that, and perhaps most importantly, the government has also addressed the real estate woes in recent weeks, amid high profile bankruptcies of developers and the pile up of built-but-unsold properties. Under a plethora of different measures, the real estate sector will be supported by financial aid to developers, a relaxation of mortgage rules and at least USD 42 Bn in central bank funding to help government-backed firms buy excess inventory. Regional developers are also incentivized to allocate part of their USD 539 Bn in bond borrowing quota to purchase unsold homes and distribute them to low income residents.

Both equity and bond markets have reacted very positively to such measures, in a movement that indicate a step change in investors’ confidence. This was one of the missing ingredients for a stronger economic response to policy stimulus, and should be more supportive of growth moving forward.

Third, manufacturing is expected to be more supportive for growth in China over the coming months. After an unusually deep and long “global manufacturing recession,” which has been in place since 2022, a positive turn towards an expansion cycle is expected. The Global Manufacturing Purchasing Manager’s Index (PMI), a timely indicator of whether activity is improving or deteriorating, has bottomed in July last year and improved thereafter. The latest print, from April 2024, point to continued expansion for three months in sequence. An expansion manufacturing cycle often gains momentum rapidly and lasts for about 1.5 years. This is expected to be supportive for China, as manufacturing represents 25-30% of the country’s GDP.

All in all, we believe that there is still room for further positive surprises and revisions in China GDP growth, and that authorities may comfortably deliver above target (5% GDP growth) performance in 2024. This is predicated in continuous positive data surprises, more aggressive policy stimulus and the beginning of the global manufacturing recovery.

Download the PDF version of this weekly commentary in English or عربي