Europe’s dependence on Russian gas has been increasing for the past few decades despite massive investment in renewable energy. Indeed, the proportion of Europe’s gas coming from Russia rose from 26% in 2001 to 37% in 2019. Now, with the war in Ukraine, Russia is using this dependency to try and undermine Europe’s support for Ukraine and push for an easing of sanctions.

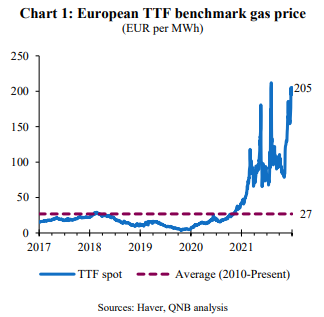

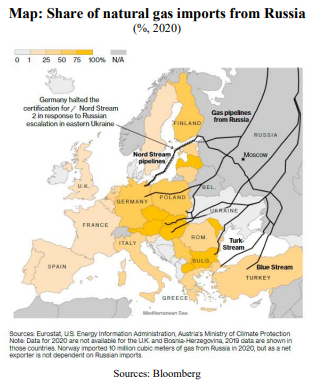

The dependence on Russian gas has means that prices have risen to record highs across the whole continent. Indeed, the Title Transfer Facility (TTF) benchmark gas price in Europe has risen to almost 8 times its average since 2010 (Chart 1). However, the pain is not being felt equally across the continent, with the countries in Northern, Central and Eastern Europe typically most dependent on Russian gas (Map).

Gas plays an important role in the European economy for heating homes, for heavy industry and as the marginal fuel in electricity production. Hence, these record high prices are already acting as a headwind for the European economy. But, with no end in sight for the war in Ukraine, financial markets have moved to price in persistently high gas prices into 2023 and 2024. This week, we consider the implications of this for Europe’s economic outlook, focusing on four main channels: the impact on consumer demand, industrial production, monetary policy and fiscal policy.

First, consumer demand is already being hit by high energy prices, capacity constraints and tight labour markets. Consumer confidence has deteriorated sharply, falling further since May as utility bills are now expected to double in many countries. Similarly, prices for holidays, restaurants and other services have risen sharply due to capacity constraints at airports and hotels, which have been unable to recruit sufficient staff, despite significant wage increases. In addition, goods prices remain elevated as global supply chain bottlenecks are easing only slowly. All-in-all, high prices for energy, services and goods are a major headwind for consumer demand across Europe despite the high levels of savings held by some wealthier households.

Second, record high gas prices have already caused large corporate gas users to reduce their consumption by a little more than 10%. Going further, in response to Russia reducing gas flows, the European Union has negotiated a target of a 15% reduction in gas use overall for 2022. But, if Russia cuts off gas completely, this may not be enough. Goldman Sachs estimate that a halt of Russian gas flows through the Nord Stream pipeline would reduce GDP by 3.5% in the Euro area, 3.7% in Germany, 5.6% in Italy, and 1.5% in France. Given, that flows have already been reduced to only 20% of capacity, then we can conclude that there will already be a sizable hit to GDP via lower industrial production in Europe.

Third, we consider the impact on monetary policy. Both the European Central Bank (ECB) and Bank of England (BoE) are lagging behind the aggressive series of interest rate hikes being implemented by the US Federal Reserve (Fed). This is already putting downward pressure on the EUR and GBP, which have depreciated relative to the USD. Weaker currencies are adding to inflationary pressures, on top of the fact that European inflation is more sensitive to energy prices, which are also higher in Europe than the US. It is therefore going to be very difficult for either the ECB or BoE to avoid hiking interest rates substantially despite the very real prospect of a sharp slowdown in GDP growth.

Finally, fiscal policy cannot come to the rescue for two reasons. First, compared to pre-pandemic governments are running with higher deficits and debt levels, which limits fiscal space. Second, governments cannot provide widespread support to all firms and households without driving both energy demand and inflation higher. Therefore, fiscal support must be limited and targeted, with direct payments to the most vulnerable firms and households.

In conclusion, weakening consumer demand, constrained industrial production, tighter monetary policy and limited fiscal support mean that European economies face several severe headwinds. These headwinds are all caused, or exacerbated, by high energy prices and/or limited gas imports from Russia due to the war in Ukraine. It seems increasingly likely that the war will drag on into 2023, which means that a recession in Europe is now looking more likely than not and that inflation is likely to remain persistently high into next year.

Download the PDF version of this weekly commentary in English or عربي