The post-pandemic combination of robust demand growth with persistent supply constraints led to a significant spike in global consumer and producer prices. As a result, major central banks have enacted “hawkish” moves, hiking interest rates aggressively and halting or even reversing balance sheet expansion. The Bank of Japan (BoJ), however, is a notable exception to this trend.

Historically at the forefront of radical monetary policy experimentation, the BoJ has so far continued its journey on tacking entrenched deflation. While the US Federal Reserve and the European Central Bank are tightening rapidly to tame inflation, the BoJ is maintaining its mix of ultra-easy policies. This includes negative interest rates, broad-based asset purchases and yield curve control measures that cap long-term rates at low levels.

But for how long will the BoJ be the “dovish” central bank outlier in a sea of “hawkish” peers? This question is gaining even more ground recently on the back of three important facts.

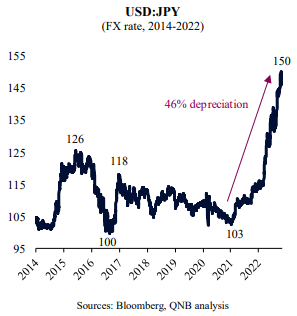

First, the Japanese Yen (JPY) has been depreciating at record speed against the USD, stoking fears of imported inflation and financial instability. USD:JPY movements have been sharp, with the Japanese currency depreciating by 43% since its recent peak in early 2021. The cause of the strong depreciation of the JPY is mainly to be found between a clear difference in the policy stance of the BoJ and other major central banks. Such policy divergence is leading to significant capital outflows from Japan to other advanced economies, particularly the US, pressuring the JPY. This takes place as Japanese investors look for higher risk-adjusted returns overseas. While 10-year Japanese government bond yields are barely positive, just above 25 basis points (bps), 10-year US Treasury yields are above 400 bps.

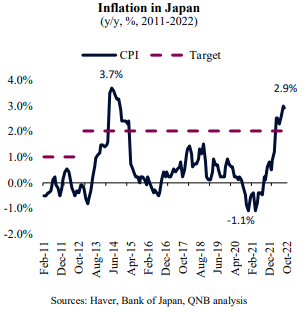

Second, inflation in Japan continues to march higher, printing in October 2022 an 8-year high figure that surpassed the BoJ target for the seventh straight month. Inflation may accelerate further on the back of high imported costs due to the sharp JPY depreciation, high inflation overseas and elevated commodity prices. Hence, analysts are now questioning whether Japan may be breaking away from its long-lasting deflationary trap of low growth, low inflation and high levels of indebtedness. This is justifying an open debate about a BoJ exit from years of radical, ultra-easy monetary policy.

Third, scheduled changes within the BoJ’s senior leadership team are coming and may accelerate the debate about fresh new policies. The term of the governor and the Board of the BoJ is set to expire in six months, potentially triggering a “change of the guard.” Haruhiko Kuroda, the highly respected current BoJ governor, is one of the main architects of the so-called “Abenomics,” the economic policy signature approach of the former Prime Minister Shinzo Abe, which aims to reflate the Japanese economy with ultra-aggressive measures. Kuroda is therefore often associated with a post-Abe continuation of “Abenomics,” championing “dovish” policies and positions. While Kuroda could still be re-appointed for a third five-year term as BoJ governor, most Japanese analysts expect a change in leadership. This could further stir the debate about policy pivots, even if modest, orderly and controlled.

All in all, a major JPY depreciation, above target inflation and scheduled changes in leadership may encourage the BoJ to move away from ultra-loose policies.

In our view, however, there is limited scope for major changes in BoJ policies. The Japanese Prime Minister, Fumio Kishida, has so far indicated his willingness to support the continuation of “Abenomics.” Moreover, below the surface of headline figures, the recent pick up in prices in Japan looks less persistent than in other advanced economies. Several components of the Japanese consumer price inflation basket still indicate muted price pressures. Before any meaningful policy change, the BoJ would need to be convinced that inflation would stabilize around 2% over the next quarters to understand if this trends persist. This would require a much stronger economy with significant wage growth, a rather unlikely scenario within the current macro-economic backdrop of slowing global activity.

Download the PDF version of this weekly commentary in English or عربي