The unprecedented strength of fiscal and monetary stimulus in advanced economies led to a rapid recovery in 2021. However, growth is slowing in 2022 and inflationary pressures are already high and rising. Higher inflation and lower GDP growth is called stagflation and is one of the most challenging situations for central banks to face.

Tighter monetary policy and financial conditions may still be necessary to prevent inflation expectations in the Euro area becoming de-anchored in response to the highest inflation since the creation of the Euro. Indeed, strong data at the beginning of the year drove a hawkish pivot from European Central Bank (ECB) at its February meeting, with follow up announcements expected at its March meeting.

However, the economic situation has now changed radically with the escalation of geopolitical tensions into conflict in Ukraine. As a result, we are facing a stagflationary shock that will impact the Euro area, mainly via a supply shock in commodity markets, particularly energy, fertilizers and grains. This week we explore the main factors influencing ECB policy, the outlook for inflation, growth and risks.

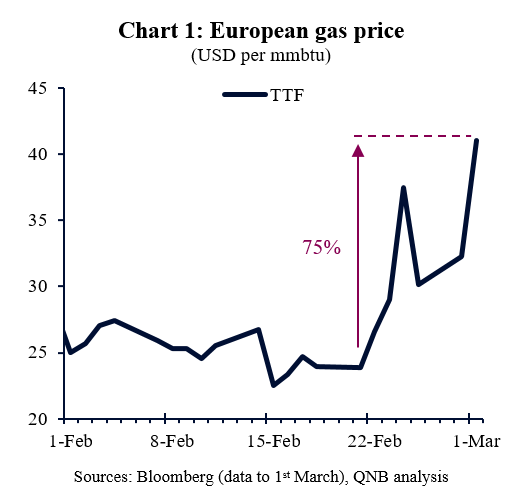

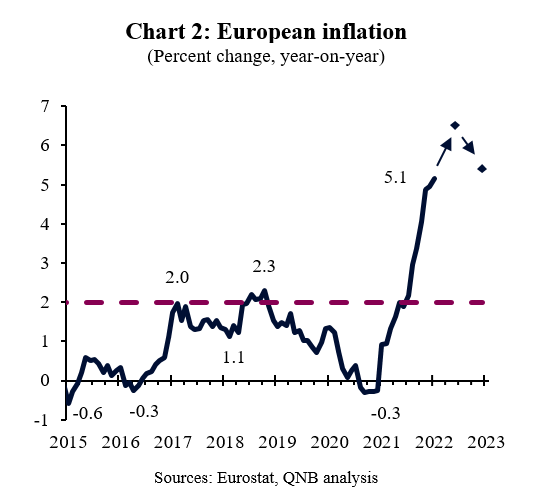

First, energy prices have surged as the conflict has escalated, with European gas prices up by over 75% from mid-February (Chart 1). Given low inventories and import constraints, we expect gas prices to remain elevated from here, resulting in continued near-term inflation pressures. However, the pass through into consumer prices is likely to be limited by a combination of regulation and government support through mechanisms including price caps and subsidies. While significant uncertainty remains, we now expect inflation to peak at over 6% this summer, before easing back towards 5% by the end of the year (Chart 2). That is well above the ECB’s inflation target of 2% and may force the ECB to tighten policy despite weaker GDP growth and heightened uncertainty.

Second, the main impact on GDP growth will be via the drag from higher energy prices on consumer spending, despite some cushioning by government support policies. The negative growth shock from reduced exports is likely to be small since the Euro area does not export much to either Russia and Ukraine. However, the impact from tightening financial conditions could be larger due to the disruption from sanctions and falling equity prices, resulting in lower spending and investment. One positive factor is that the Euro area began the year with strong positive momentum, recovering from the impact of the Omicron variant. We also expect more increased government spending to support GDP growth. Taken together, these factors mean that we now expect Euro area growth to be around 0.5 percentage points below the IMF’s January forecast of 3.9% growth in 2022.

Third, we are obviously facing a period of acute uncertainty and risk. From the perspective of Euro area inflation, GDP and monetary policy, the main risk is that gas supplies are disrupted for an extended period. Such disruptions could impact industrial production with Goldman Sachs estimating a potential hit to GDP of 1% in Germany and France, and as much as 3% in Italy. Hence, we judge that risks are clearly, and significantly, to the downside for the Euro area’s GDP outlook relative to the base case outlined in the previous paragraph.

To conclude, our view is that the ECB continuing with its hawkish pivot in March will further weaken the economic outlook, and exacerbates clear downside risks. Therefore, we expect a deterioration in the macroeconomic environment to force the ECB to pause for breath over the summer, perhaps even being unable to bring an end to asset purchases before September.

Should additional stimulus be necessary, due to the crystallisation of downside risks, then it is likely to come more from fiscal rather than monetary policy. However, the ECB will need to keep interest rates low enough and financial conditions loose enough to support debt sustainability and provide fiscal space to governments.

Download the PDF version of this weekly commentary in English or عربي