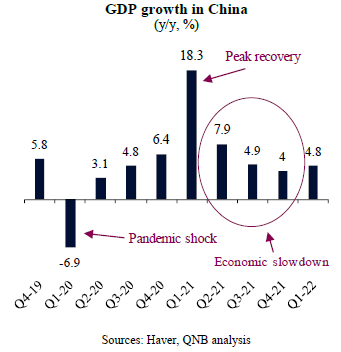

China is a major source of uncertainty for the global growth outlook in 2022 and 2023. After a sudden collapse in demand and activity in Q1 2020, following the outbreak of Covid-19, China performed an impressive recovery from the pandemic. The positive momentum lasted from mid-2020 to mid-2021. China at that time was the first and only large economy to present positive GDP growth in 2020, being ahead of other countries in the economic cycle by several quarters. While the strong performance led to an early withdrawal of both fiscal and monetary stimulus, the government also started a comprehensive campaign to tighten regulation on the real estate and corporate sectors, dampening business sentiment and containing a more significant rebound in private investments.

As a result, the recovery in China slowed down significantly since Q2 2021. In light of this, Chinese policymakers started to gradually revert from policy tightening to policy easing in late 2021 and early 2022, aiming to create more breathing room to the private sector. This provided some support to the economy, as a significant pick up in investments boosted GDP growth to 4.8% in Q1 2022, the first quarter of accelerating activity after the period of peak recovery from the first phase of the pandemic.

However, despite this positive performance, there are clear signs that a sudden stop in momentum already started. In March 2022, a new wave of Covid-19 outbreaks led to a strong government response within the “Covid-zero” framework, i.e., strict lockdowns and social distancing measures that persist until new cases in affected areas are flat lined. This has so far included short lockdowns in the Southern Province of Guangdong, the main manufacturing hub of the country, and a longer, very significant lockdown in Shanghai, the largest and wealthiest city in China.

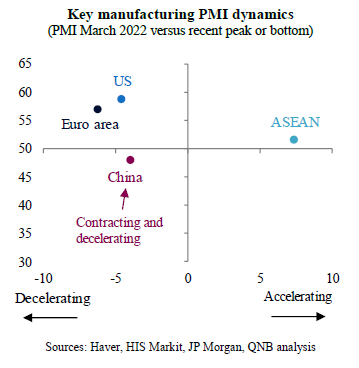

Lockdowns are affecting hundreds of millions of people in China, with the economic effects already starting to emerge. The manufacturing Purchasing Managers’ Index (PMI) of China, a survey-based indicator that measures whether several components of activity improved or deteriorated versus the previous month, slid back to sub-50 levels in March. Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions. In other words, higher frequency data is indicating that activity in China is not only decelerating but is also contracting or running below normal levels. In contrast, activity is still comfortably in expansionary territory in all major peers, including the US, the Euro area or the emerging economies of Southeast Asia (ASEAN).

In our view, two factors maintain the uncertain outlook for growth in China moving forward.

First, China is still vulnerable to new Covid-19 outbreaks. In fact, local Covid-19 outbreaks are becoming more frequent as variants that are more contagious emerge amid a population that is less immunized. We expect the government to continue with its “Covid-zero” policy, deploying robust social distancing measures against local outbreaks. This will weigh on growth as activity will be halted around the locations where new Covid-19 cases concentrate.

Second, supply-chain constraints are likely to continue, on the back of Covid-19 disruptions, low inventories and still strong pent-up demand. Supply constraints include low inventory levels as well as bottlenecks and other disruptions in manufacturing output and transportation infrastructure, such as ports, containers, and logistic networks. We expect to see supply constraints ease only by mid- to late-2023, when Covid-19 should become less of a threat to Asia. Supply-chain constraints put a cap on China’s manufacturing growth for this year and next, creating negative spillovers to the global economy.

Despite the above mentioned challenges, the Chinese economy should be partially buffered by fresh new measures of monetary and fiscal support. In fact, in mid- to late-April, authorities announced different economic packages, signalling to the public that policymakers will not tolerate a “hard landing” of the Chinese economy. The packages include liquidity injections, credit support to key sectors, subsidized loans, infrastructure investments and other targeted measures.

All in all, more simulative policies are justified by China’s significant slowdown as well as the challenges posed by Covid-19 outbreaks and supply constraints. On balance, we expect to see a further deceleration in GDP growth in Q2 2022, before some stabilization takes place over the second half of the year. We project China’s GDP to grow by 4.5% in 2022 and 5% in 2023. Such subdued performance, vis-à-vis historical norms, will be less supportive to the global economy, making it more vulnerable to other negative shocks, such as the US policy tightening and the Russo-Ukrainian conflict.

Download the PDF version of this weekly commentary in English or عربي