Governments around the world are having their finances savaged by the coronavirus pandemic. Last week, we highlighted that a sudden reversal of capital flows is a problem for vulnerable Emerging Markets (EM). Indeed, the International Monetary Fund (IMF) estimates that portfolio capital outflows from EM were about $100 billion in the past two months, more than three times larger than during the same period of the 2008 global financial crisis.

As we write, the IMF is conducting its annual spring meetings in a virtual format for the first time. Kristalina Georgieva, the IMF’s new Managing Director, opened the meetings by saying that the IMF had approved a doubling of emergency lending to USD 100 billion. The IMF estimates the gross external financing needs for EM to be in the trillions of dollars, of which EM can only cover a portion themselves, leaving residual gaps in the hundreds of billions of dollars. Georgieva also gave a preview of the April 2020 World Economic Outlook, noting that: “We are still faced with extraordinary uncertainty about the depth and duration of this crisis. It is already clear, however, that global growth will turn sharply negative in 2020”.

This week we look at the policy response to this challenge. First, we explain how the IMF lends to vulnerable countries by borrowing from countries in a stronger position. Second, we look at the demand for IMF’s emergency facilities, boosted by the fact that they come with much softer conditionality than standard IMF support. Third, we consider the size and sources of IMF’s funding and lending capacity. Finally, we look at other policy measures, which could boost the IMF’s capacity or provide additional liquidity support to EM without the IMF. In order to provide loans to vulnerable countries the IMF must fund itself by borrowing from member countries that have more robust external positions.

One of the IMF’s key roles is to provide loans to member countries experiencing actual or potential balance of payments problems to help them rebuild their international reserves, stabilise their currencies, and continue paying for imports, while correcting underlying problems. The IMF’s normal lending is to countries that are considered solvent, but experience balance of payments difficulties. These loans are extended via structured programmes with strong conditionality.

The IMF is currently facing an unprecedented number of calls for emergency financing, receiving 90 requests or expressions of interest from member countries. The IMF’s emergency financing facilities are distinct from its more traditional bailout programmes. Their purpose is to enable borrowing countries with implementing policies to address emergencies such as the coronavirus. Borrowing can be negotiated more rapidly and with fewer conditions. The IMF’s emergency lending capacity has recently been doubled to USD 100 billion.

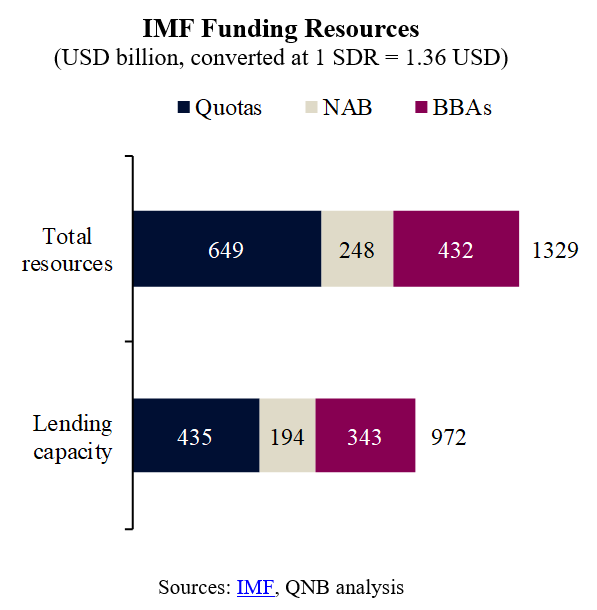

The funding for IMF’s lending is provided by member countries, primarily via quotas. Each member of the IMF is assigned a quota, based broadly on the relative size of its economy. Additional funding can be drawn from credit lines as a temporary supplement to funding provided by quotas. New Arrangements to Borrow (NAB) allow the IMF to borrow additional funding from the most credit worthy member countries and institutions. The IMF has also entered into several rounds of bilateral borrowing agreements (BBAs) to ensure that it can meet the financing needs of its members. The current BBAs, agreed in 2016, run through to the end‑2020.

The IMF’s total resources (around USD 1.3 trillion) is simply the sum of quotas, NAB and BBAs (see chart). However, the IMF cannot draw funding from all of its members at the same time as well as lending to some of them. Therefore IMF’s effective lending capacity (around USD 1 trillion) is less than its total resources, with around 20% of resources kept as a liquidity buffer and resources provided by vulnerable countries also excluded from the calculation.

So far, only around 20% of the IMF’s lending capacity has been committed. But what if that is not enough?

The IMF’s balance sheet is expressed in an archaic unit called the Special Drawing Right (SDR). The SDR is a basket of 5 major currencies (the Chinese RMB, USD, euro, Japanese Yen and British pound sterling), which is currently worth about 1.36 USD. Some economists have proposed a huge allocation of SDR, worth around USD 4 trillion, large relative to IMF’s total resources of USD 1.3 trillion. This would effectively give the IMF’s poorer members a claim on the currency reserves of its richer ones. Indeed, the IMF reports that several poorer countries have called for it, and that the idea is under discussion. However, the SDR was originally designed as a replacement for the USD in its role as the international reserve currency. The US wants to maintain the USD’s dominant role in international finance, and has a large enough share of votes at the IMF to effectively veto any new allocation of SDRs.

Fortunately, the US takes the USD’s role seriously, with the US Federal Reserve (the Fed) proactively providing USD liquidity to central banks around the world. Indeed, the Fed has permanent swap lines with the European Central Bank, the Bank of Japan and other issuers of major currencies. Going further, in response to the crisis the Fed opened swaps with nine other countries including Korea, Brazil and Mexico. Even more broadly, the Fed enhanced the ability of dozens of foreign central banks to access USD by allowing them to exchange their holdings of US Treasury securities for overnight USD loans.

In conclusion, we are becoming ever more aware of the magnitude of the economic shock caused by the coronavirus. The large amount of USD debt issued by EM is a clear vulnerability. Fortunately, the IMF has substantial resources upon which it can draw and the Fed has also taken significant steps to ensure USD liquidity in international as well as domestic financial markets.

Download the PDF version of this weekly commentary in English or عربي