Commodities are a cornerstone of the global economy, fueling the tangible processes that sustain the physical aspects of modern life. Within the broader commodity spectrum, copper stands out as the world’s most actively traded base metal. Valued for its unmatched electrical conductivity and versatility, copper is indispensable to industries spanning construction, infrastructure, transport, and durable goods.

Beyond its industrial utility, copper prices have long been recognized as a forward-looking indicator of economic momentum. Because shifts in copper demand often precede broader changes in economic activity, the metal is widely regarded by market participants as a bellwether for investment trends and cyclical turning points. This predictive quality has earned copper the nickname “Dr. Copper” – a nod to its perceived expertise in diagnosing economic trends, as if it held a PhD in economics.

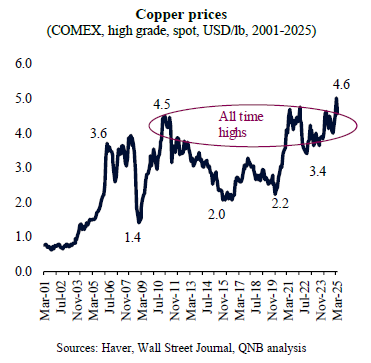

Copper prices have decisively broken out of their historical trading range, now standing at around USD 4.6 per pound (lb) – a clear move beyond previous peaks seen both after the Global Financial Crisis and during the post-Covid investment boom. This breakout is particularly noteworthy given the recent deterioration in global growth sentiment, after the “Liberation Day” tariffs imposed by the Trump administration, which might have been expected to dampen demand. Instead, copper’s resilience underscores a deeper structural strength.

Naturally, these recent movements prompt the question: are copper prices overstretched and due for a significant correction, following the expected slowdown in global growth, or are we entering a new era of sustained higher prices for copper? While acknowledging that copper remains subject to bouts of volatility and faces meaningful pressures – notably from slower urbanization and a less benign real estate market evolution in China – we posit that powerful secular or long-term forces are now the dominant driver for prices. In this piece, we outline three key secular drivers that, in our view, will underpin robust copper demand and support elevated prices over the coming years.

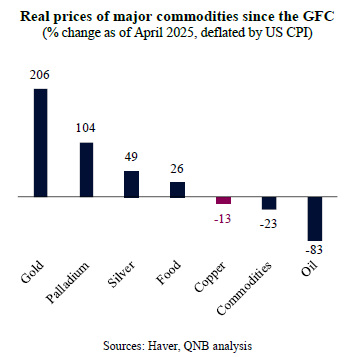

First, various indicators of relative value point to considerable upside potential for copper. Despite recent nominal gains, copper prices remain around 13% lower in real terms (adjusted for US CPI inflation) compared to their 2008 peak during the GFC. This contrasts sharply with the strong real appreciation seen in other metals such as gold, palladium, and silver. Copper’s trajectory has instead been more similar to the broader commodity complex, which has also suffered from the significant drag of real energy prices. This suggests that copper is “cheap” and could appreciate significantly before any demand destruction materializes.

Second, FX dynamics are poised to lend additional support to copper prices. Historically, copper has shown a strong inverse correlation with the USD – typically rising when the USD weakens and falling when it strengthens. The USD has already depreciated by more than 7.8% against a basket of major currencies so far this year. Moreover, despite this sharp depreciation, currency valuations still suggest that the USD remains overvalued by roughly 18%, indicating further room for depreciation ahead. A softer USD would enhance global purchasing power for USD-denominated commodities like copper, stimulating demand and providing an additional tailwind for prices.

Third, underlying market fundamentals point to sustained copper shortages in the medium- and long-term, setting the stage for structurally higher prices. On the demand side, copper consumption is set to accelerate sharply, driven not only by established trends in electrification and infrastructure but increasingly by the explosive growth of AI-related technologies. The rapid buildout of data centers, high-performance computing clusters, and power-intensive digital infrastructure is fueling a surge in electricity demand, which in turn amplifies the need for copper across grids and transmission networks. On the supply side, the picture remains constrained. Inventories are hovering near historic lows, and capital expenditure by major copper miners continues to lag, limited by complex permitting processes, rising geopolitical risks, and pressure from investors to maintain capital discipline. This supply-demand imbalance is likely to require higher prices to incentivize the next wave of production. Copper’s unique role in enabling the backbone of both the energy transition and the AI revolution cements its importance – and underscores the case for sustained strength in the years ahead.

All in all, copper prices are likely to de-couple from cyclical macro pressures, due to powerful tailwinds such as “cheap” relative prices, support from FX markets and a favourable supply-demand balance dominated by long-term industrial trends.

Download the PDF version of this weekly commentary in

English

or

عربي