Covid-19 has led to substantial downward revisions to global GDP growth forecasts. For example, the IMF lowered its forecast for 2020 to -4.9% in the July, down from +3.3% in January. The impact of Covid-19 on global GDP is therefore markedly worse than the global financial crisis in 2009, when global GDP fell by -2.1%.

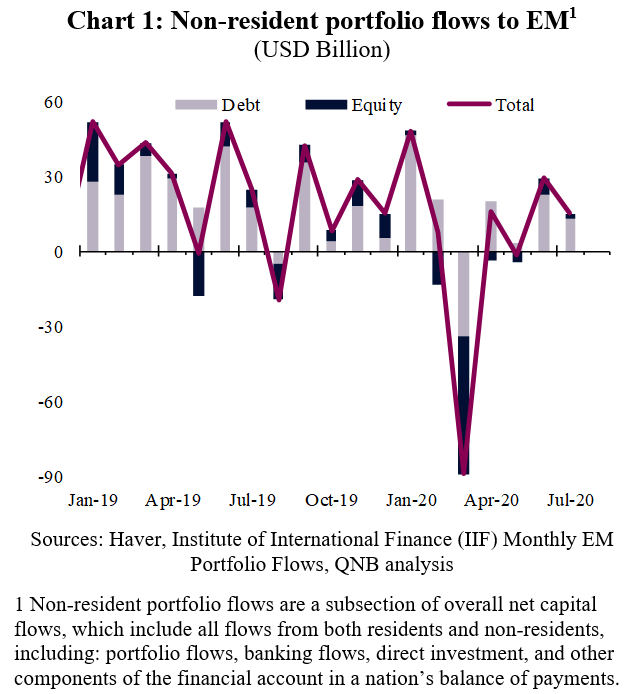

We started the year with a view that robust capital flows to Emerging Markets (EM) were likely to continue in 2020. But then Covid-19 hit the global economy leading to a sudden reversal of capital flows. Fortunately, massive policy support from major central banks, e.g., US Federal Reserve (Fed) and the Bank of Japan, has enabled flows to EM to rebound, with both EM equity and debt posting a second month of positive inflows in July (Chart 1).

1 Non-resident portfolio flows are a subsection of overall net capital flows, which include all flows from both residents and non-residents, including: portfolio flows, banking flows, direct investment, and other components of the financial account in a nation’s balance of payments.

With this in mind, we highlight three factors buffeting capital flows.

First, interest rate cuts and massive liquidity injection by major central banks are a tail-wind for capital flows to EM. Loosening of monetary policy in major advanced economies is often referred to as a “push factor” for capital flows to EM. The logic for this is simple. For example, when the Fed lowers interest rates in the US, it flows through to lower returns for depositors holding money in US banks, which “pushes” them to investment in other more risky assets and currencies, such as EM debt and equity.

Second, an improvement in market sentiment, with an easing of risk aversion and flight-to-safety dynamics, are a tail-wind for capital flows to EM. The Fed lowering interest rates and injecting liquidity into financial markets, alongside other policy support from governments, has supported and improved market sentiment. Market participants have gained confidence that markets will continue to function reasonably smoothly, which encourages or “pushes” them to invest more in riskier EM assets.

Third, concerns about still-high levels of infections in some EM, and resurgence of the virus in others, are a head-wind for capital flows to EM. Many countries in Latin America and South Asia are experiencing still-high levels of virus infections. High levels of virus infection either directly slow the economy, by taking workers away from their jobs, or indirectly via tighter social distancing measures and localised lockdowns that are required to control the virus. We expect this to recover once the virus eases.

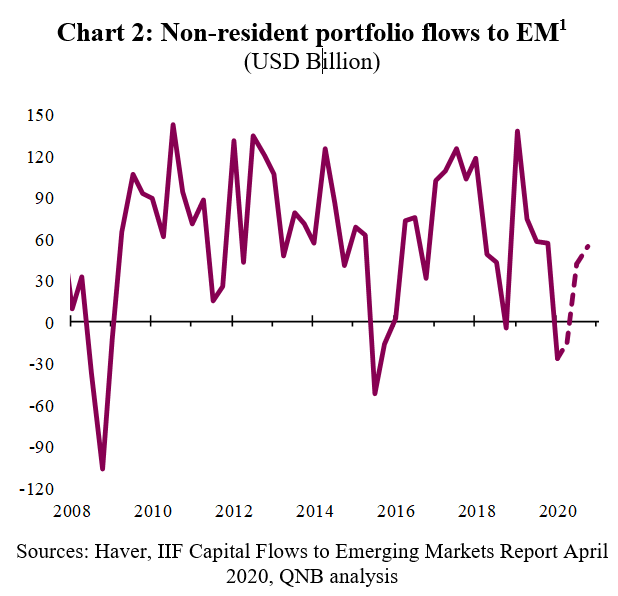

Our base case outlook assumes that significant policy support is maintained and that the virus is gradually brought under control in most countries. That should lead to a continued recovery of the global economy during the second half of the year. Considering the three factors mentioned above, we expect the tail-winds to be marginally stronger than the head-winds: (1) continued low interest rates are a persistent tail-wind; (2) adequate market sentiment is also a persistent tail-wind; and (3) moderating rates of infection are an easing head-wind. Together, we expect these three factors to support continued, but moderate, capital flows to EM over the second half of the year. Therefore, despite the fall in GDP in 2020 being larger than in 2009, the impact on portfolio flows to EM is likely to be smaller (Chart 2). Nevertheless, flows will still be much weaker in 2020 than they were in 2019.

Download the PDF version of this weekly commentary in English or عربي