The Euro area is struggling with a resurgence of Covid-19 now that the weather is colder and people are spending more time together indoors, which increases the rate of infection of the virus. This increase in Covid-19 infections is coinciding with the flu season that lasts from October until May in the Northern Hemisphere, which raises concerns over the capacity of the health care infrastructure such has hospital beds and particularly intensive care beds.

So far, the sharp rise in new cases has translated into relatively fewer severe cases needing hospital treatment and also a lower death rate. This is likely to be due to a number of factors including medical professionals having a better understanding of the virus and treatment options.

However, this is no time for complacency, especially as people will have a strong desire to gather and mix socially during the festive season. The resurgence of Covid-19 has prompted governments to reprise some of the containment measures used during the first wave earlier this year, including a national lockdown imposed by France starting on the 30th of October, and increasingly intense local lockdowns in other countries.

Our analysis considers the outlook for economic growth and inflation before delving into the monetary policy tools available to the policymakers sitting on the European Central Bank’s Council.

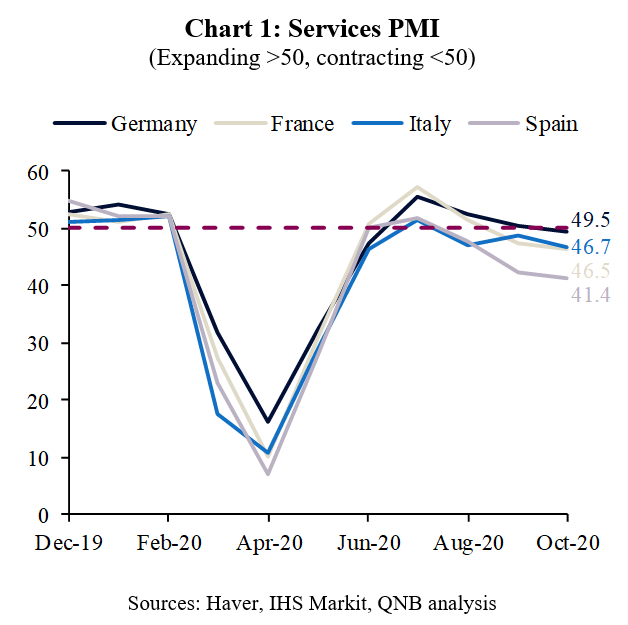

The sharp rebound in economic growth of the Euro area during the summer ran out of steam by August. While the manufacturing sector shows continuing recovery, the services sector has been hit by the partial return of containment measures. For instance, the service sector PMI in the four largest Euro area economies has drifted lower and now indicates contraction (Chart 1). The outlook is likely to remain bleak until next spring despite some good news about the efficacy of the vaccine from Pfizer and BioNTech. The main challenge now is how rapidly the vaccine can be mass-produced, and at what cost, to enable sufficient vaccinations to reach herd immunity.

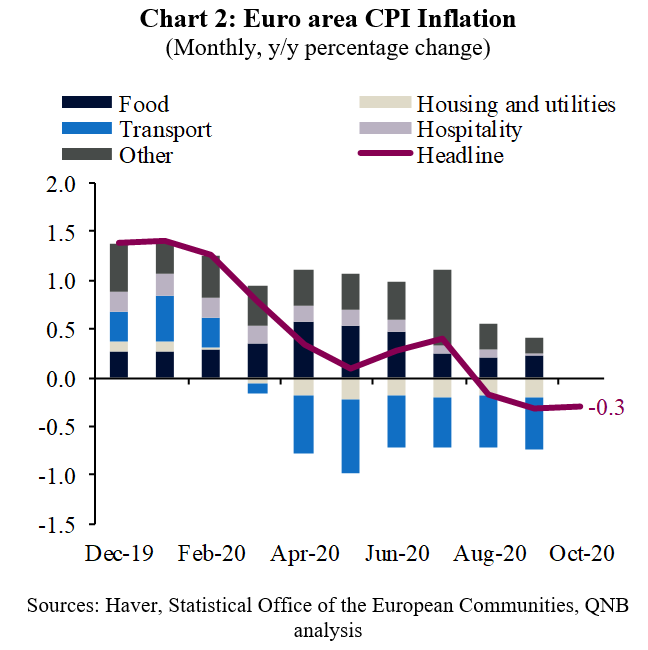

Headline CPI inflation spent its third month in negative territory in October on the back of muted price pressures (Chart 2). By far the largest drag on inflation comes from the transport component of inflation, held down by low oil prices since March 2020. Likewise, housing and utilities are marking a negative contribution due to low energy prices. More concerning is the broad-based weakness across other components since July as demand for goods and services have been more severely impacted by the pandemic than the supply side of the economy.

With such weak outlook for economic growth and inflation so far below its target, the ECB is honour-bound to do more at the December meeting of its Governing Council. However, with its main policy interest rate already in negative territory, the ECB is dependent on unconventional policy tools.

The ECB’s main tool is asset purchases, often referred to as quantitate easing (QE). To side-step constraints on pre-existing programs, the ECB launched its Pandemic Emergency Purchase Program (PEPP) in March 2020 with EUR 750 Bn, before increasing it by EUR 600 Bn in June. Going forward, we expect the Governing Council to increase the programme by additional EUR 400 Bn at its December meeting.

Furthermore, the ECB is currently supporting banks through Targeted Long-Term Refinancing Operations-III (TLTRO-III). This facility offers Euro area banks subsidised funding in return for increasing lending to the real economy. We expect the ECB to extend the availability of the facility from June to end-2021.

Finally, the ECB could further cut the deposit rate from -0.5% currently. However, we consider this move unlikely because it would further reduce the profitability of Euro area banks, which find it difficult to pass-on negative interest rates to depositors and other sources of funding.

Despite concerns that ECB has run out of gunpowder, President Lagarde affirmed that “the options in our toolbox have not been exhausted. If more has to be done, we will do more”.

We should also bear in mind the interaction between monetary and fiscal policy. In particular, the PEPP provides fiscal space for governments to increase their debt issuance substantially. This has helped lower the risk spread between countries in northern Europe with low bond yields, and countries in southern Europe with higher bond yields.

The evolution of the pandemic and the responses to contain it will continue to dominate the outlook for both economic growth and inflation, with the countries hit hardest expected to see slower recoveries. We do not expect Euro area GDP to return to its pre-crisis levels until 2022.

Download the PDF version of this weekly commentary in English or عربي