The fallout from the global spread of Covid-19 has already produced an epic sudden change in risk sentiment from rampant optimism to fear since the beginning of 2020. Historically, this has tended to favour safe-haven assets, including high quality sovereign papers, precious metals and currencies of stable and wealthy countries. While the recent bout of risk aversion has mostly created textbook reactions in different asset classes, the recent depreciation of the USD constitutes an exception to what would normally be anticipated. As a classic safe-haven currency, the USD usually appreciates when investors face global emergencies. However, this time seems to be different. Our analysis delves into the forces that have been driving USD moves.

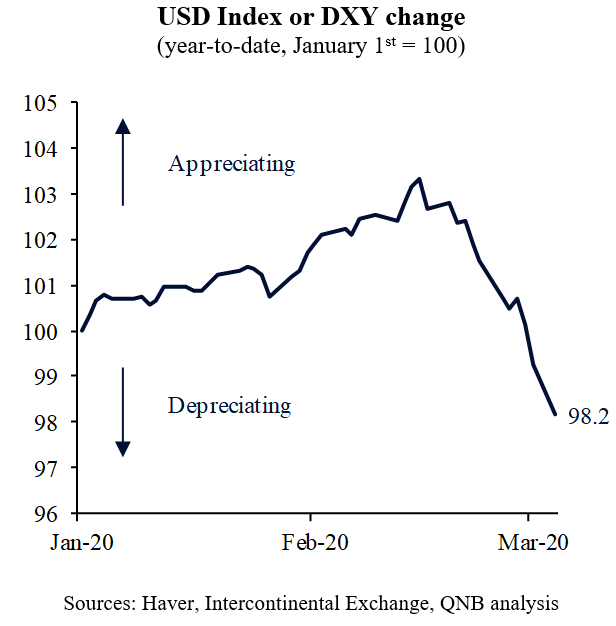

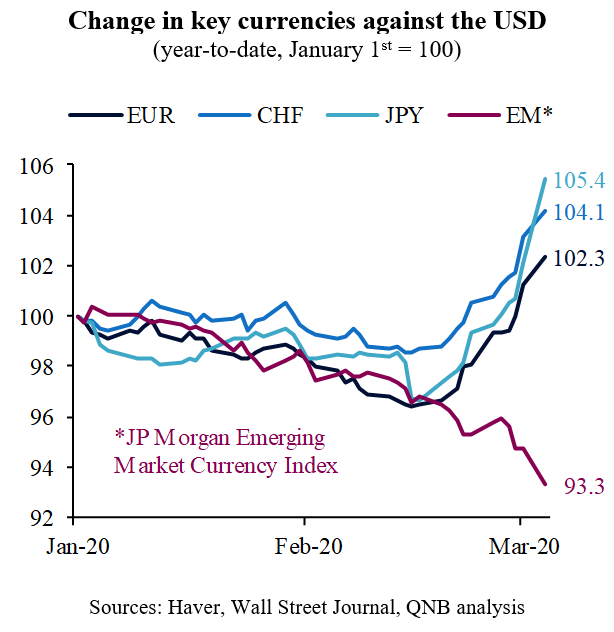

The USD index (DXY), a traditional benchmark that measures the value of the USD against a weighted basket of six currencies, has depreciated by almost 5% in recent weeks. This comes after a period of appreciation but was already more than sufficient to place the DXY performace for the year in negative territory. The movement is unusual given the generally positive correlation between volatility or fear and the DXY. A comprehensive explanation for such a move requires a dive into some key bilateral foreign exchange rates between the USD and other currencies. In fact, the USD has been underperforming key peers from other advanced economies while outperforming emerging market currencies.

The movements of the USD are determined by several cross-currents associated with risk sentiment, trade positioning and other macro related trends.

Three factors explain the recent depreciation of the USD against key currencies of other advanced economies. First, the USD is not the only safe-haven currency. Other currencies, particularly the Japanese Yen (JPY) and the Swiss Franc (CHF), have also historically served as a safe-haven or shock absorber in the portfolio of global investors. They also tend to appreciate in periods of global risk aversion, particularly due to the interest of investors from Asia and Europe.

Second, the magnitude of recent market dislocations triggered a broad sell-off that unwound long standing carry trades of leveraged investors against low-yielding EUR and JPY. Such sell-off includes not only short EUR/USD and long USD/JPY positions but also massive short EUR/EM trades. This produced a significant technical appreciation of the EUR and JPY against the USD.

Third, differences in monetary policy space create a fundamental asymmetry in terms of the potential direction of the spread between USD Treasury papers versus European and Japanese government bonds. While rates in Europe and Japan are already at the lower bound (close or below 0), there is still space for US rates to fall further. As the spread narrows, the USD becomes less attractive.

When it comes to EM currencies, two factors explain the recent USD appreciation. First, negative developments associated with the Covid-19 severely affected risk sentiment, increasing price volatility and the overall level of stress in money, bond and equity markets. Risk-off behaviour prompt investors to dump risky assets, including EM-related equities, bonds and FX.

Second, disruptions in global trade and supply chains as well as demand destruction in China are particularly threatening to Asian and commodity exporters. The massive deflationary shock is already prompting EM central banks to cut rates. In contrast to Europe and Japan, monetary authorities in most EM countries still have policy space. Lower yields in EM are encouraging further capital flight towards safer assets.

All in all, we expect the risk-off environment to continue throughout H1 2020, even if in a slightly more moderate fashion. However, the current trend of safe-haven currencies of advanced economies against the USD is expected to ease, especially as FX technical positioning changes and fixed income markets digest lower USD yields.

Download the PDF version of this weekly commentary in English or عربي