The spread of the novel coronavirus (Covid-19) has resulted in changes in behaviour and containment measures bringing the world to an entire halt. The resulting shocks to both supply and demand have triggered one of the fastest and deepest economic downturns ever experienced in modern times. However, recent data suggests that the decline in growth of the global economy has reached the bottom, with activity now being set for a significant rebound over the coming months. Our analysis delves into the global Purchasing Managers’ Index (PMI) for the manufacturing sector in order to assess the conditions for an economic recovery.

The global manufacturing PMI is a survey-based indicator that measures whether several sub-components of business activity have improved or deteriorated versus the previous month. As such, the manufacturing PMI is an index that serves as an important coincident indicator of global activity and demand. Traditionally, an index reading of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) changes in business conditions.

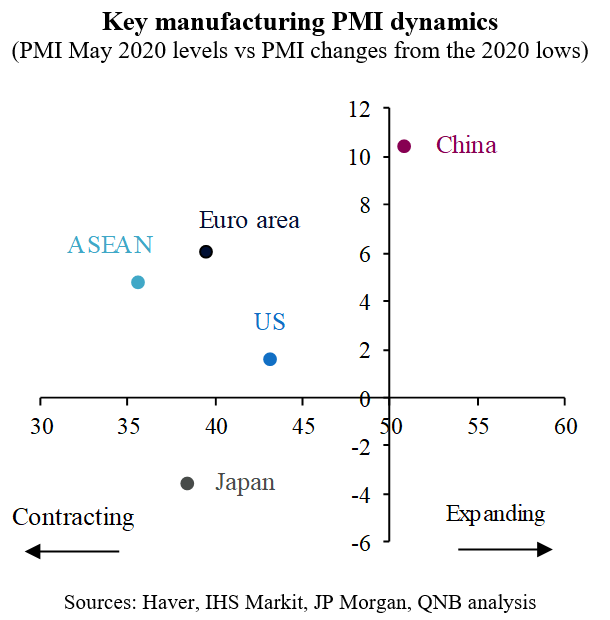

The headline global manufacturing PMI worsened for three consecutive months from 50.3 in January to 39.6 in April 2020, narrowly undercutting the contraction during the 2008-09 financial crisis. However, the latest data for May imply that the deterioration of global economic conditions is slowing down, with the headline manufacturing PMI figure recovering to 42.4. While the absolute levels are still within contractionary territory, the rate of change is moving in the right direction, suggesting a potential turning point. Importantly, positive developments are taking place in almost all major economies, including the US, China and the Euro area, with Japan being the only major laggard.

Looking into the details, the PMI sub-components are also indicative of a positive turning point. We highlight three main areas.

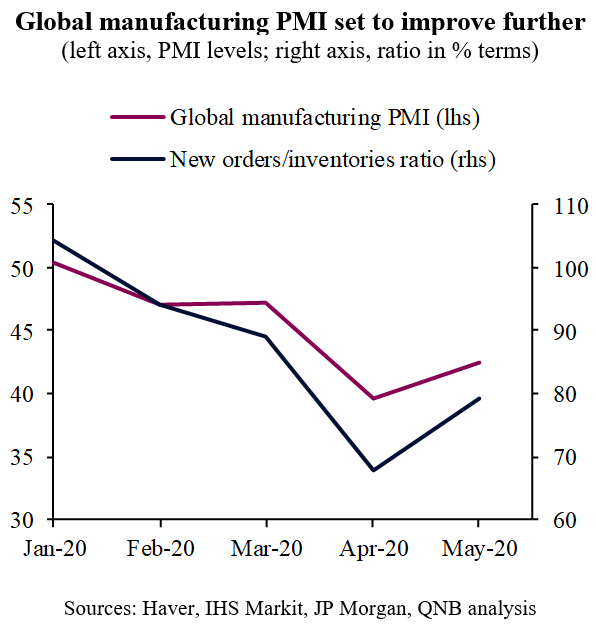

First, forward looking PMI sub-components are pointing to additional improvements in the next couple of months, as the ratio of new orders to inventories suggest investment in working capital is set to increase. When inventories are drawn-down and new orders increase, manufacturers need to expand activity. The new orders to inventories ratio tends to lead the headline manufacturing PMI by 2 months, i.e., manufacturing PMI tend to respond to changes in the new orders to inventories ratio and follow its direction and pace.

Second, output improved to 39.2 in May compared to 32.5 in April. Despite the low absolute level, the sharp increases point to a fast stabilisation. As major economies open up, pent up demand will filter through the economy. This is likely to be amplified by the strong support from both fiscal and monetary authorities, which could push output quite suddenly into expansionary territory.

Third, employment eased slightly to 43.2 in May from 41.5 in April. Likewise, this is suggesting that the layoffs have reached their peak and we should start seeing improvements across different labour markets. For this particular sub-component, the US is at the forefront, given the flexibility of its labour market. After a sharp deterioration in the employment sub-component for the US from 46.9 in February to 27.5 in April, the contraction started to ease to read 32.1 in May. In addition, and arguably even more importantly, US non-farm payrolls experienced the first improvement in months, with a robust gain of 2.5 million jobs in May against a consensus expectation of 8 million job losses.

Overall, while global manufacturing activity is still struggling as a result of the shock from Covid-19, all key sub-components of major manufacturing PMI surveys point towards economic stabilisation. Should this trend continue, global manufacturing will likely be transitioning from deteriorating at a slower rate to improving gradually in the coming months.

Download the PDF version of this weekly commentary in English or عربي