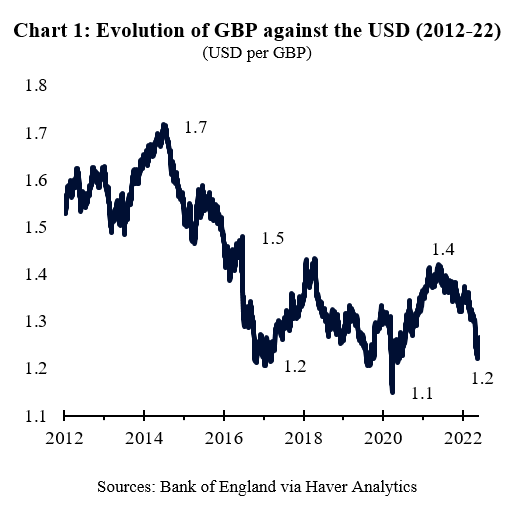

The Great British Pound (GBP) fell sharply at the outbreak of the Covid-19 pandemic, briefly to a level even below those seen after the Brexit referendum in 2016 (Chart 1). Since then, the GBP recovered to a peak of 1.4 per USD in early 2021, but has recently experienced another sharp depreciation. The main reason for the depreciation is the divergence in communication and approach between the Bank of England (BoE) and other major central banks, such as the US Federal Reserve (Fed). Essentially, the BoE is being more accommodative (“dovish”) by hiking interest rates less aggressively than the Fed. This incentivizes investors to shift their assets from the UK to the US seeking higher risk-adjusted returns, which puts downward pressure on the GBP.

Many central banks, including the Fed and BoE, are in a difficult position as they face stagflationary shocks, that both increase inflation and weaken economic growth. This means that interest rate hikes, necessary to control inflation, risk pushing the economy into a recession.

This week, we first compare inflation in the US and the UK, before delving into the outlook for GDP growth in both countries.

The disruption to energy supply from the war in Ukraine is the main difference between the US and the UK. For example, European gas prices have increased by much more than US gas prices. The result is that headline inflation is expected to peak at around 10% in the UK during Q4, significantly higher and later than in the US.

Secondly, although wage growth has risen to around 5% in both the UK and the US, labour markets in the UK will remain even tighter than in the US because Brexit is inhibiting the return of skilled workers form the European Union (EU) to the UK labour market.

Last but not least, the depreciation of GBP is putting upward pressure on the UK prices of imported goods and services. This is because the UK typically buys imports from larger markets in the US, EU and Asia, which are often priced in either USD or EUR. Imported goods and services becoming more expensive in GBP adds further pressure to inflation.

In summary, the outlook for inflation in the UK is worse than in the US, meaning that the BoE is under more pressure than the Fed to control inflation.

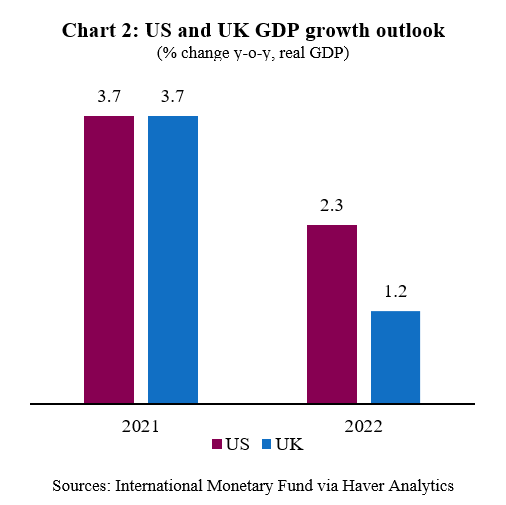

At the same time, the outlook for GDP growth in the UK is much weaker than in the US. The IMF expects US growth to slow from 3.7% in 2022 to 2.3% in 2023, whereas UK growth is expected to slow from 3.7% in 2022 to 1.2% in 2023. This leaves the BoE with a more severe recessionary headwind than the US. Indeed, the BoE has recently released its own forecast, which is even more bearish, with a contraction in GDP of 0.25% pencilled in for 2023.

In summary, the BoE is currently is facing an even more difficult situation than the Fed. On the one hand inflationary pressures are worse, with higher inflation expectations, wages, energy and import prices, in the UK than the US. This would suggest the BoE needs to be even more aggressively hawkish than the Fed to curb inflation. But, on the other hand, a lower growth outlook in the UK than in the US suggests that the BoE needs to be more accommodative than the Fed to support economic activity and growth.

Therefore, we do not expect the BoE to follow the Fed with a 50 basis point (bp) hike at either its next two meetings in June and August. Rather, we expect the BoE to stick to a steady pace of 25 bp hikes in each policy meeting, in an attempt to avoid a sharper slowdown that may turn into a recession towards the end of this year.

Download the PDF version of this weekly commentary in English or عربي