The US Federal Reserve (Fed) continues to dominate macroeconomic discussions. After supporting the “Great Pandemic Reflation” (2020-21), a stimulus-induced recovery that brought the US economy back to life from the depths of a sharp downturn, the Fed seems to be on the edge of a significant policy change to a more “hawkish” stance.

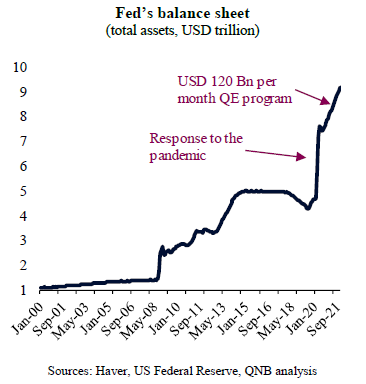

With the ultra-easy policy following the pandemic shock, the Fed cut interest rates to close to zero and injected massive amounts of liquidity into the financial system. The liquidity injection took place either through emergency measures or through a large-scale asset purchase programme (quantitative easing or QE) of USD 120 Bn a month. As a result, the Fed’s balance sheet ballooned to more than USD 8.6 trillion in total assets. This helped to stabilize markets, boost sentiment and support credit and demand.

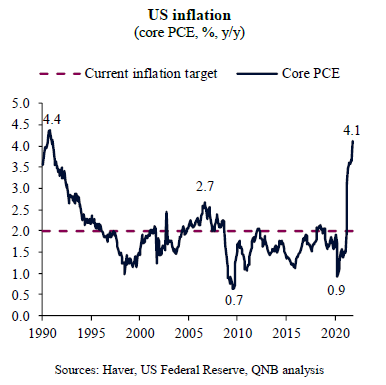

However, the Fed is now starting to enact its monetary policy “normalization” process. The change was officially announced in September 2021, when Jerome Powell, the Fed’s Chairman, indicated the expected timeframe of the “tapering” process, i.e., the process of scaling down the QE programme. Back then, Powell announced a gradual reduction of long-term asset purchases. QE already started to be reduced from USD 120 Bn per month to USD 105 Bn last month. According to the Fed September guidance, QE is set to be continually reduced by USD 15 Bn all the way to mid-2022, when net asset purchases from the Fed would reach zero. More recently, in his Congressional testimony on November 30th, Powell doubled down on the normalization narrative, suggesting that elevated inflation (core personal consumer expenditure price index – PCE – spiked to 4.1% y/y in October) could justify ending asset purchases sooner than planned, which would imply a faster than USD 15 Bn per month QE reduction. This communication, interpreted as a “hawkish” pivot by several analysts, led to significant risk-off moves in markets, with equity prices declining, short-term interest rates rising and volatility increasing.

In our view, three factors explain Powell’s recent hawkish pivot towards a faster normalization of monetary policy.

First, the Fed leadership was recently empowered by a fresh new four-year term, which strengthens the legitimacy of any significant policy changes. In fact, US President Joseph Biden announced the re-nomination of Jerome Powell for Chair of the Fed in mid-November. The re-nomination took place against a backdrop in which “progressives” were advocating the nomination of more “dovish” names that would support “easier” policies for longer, in order to fund higher social spending from the government. The confirmation of Powell was understood by many as an additional backing from the administration to a more hawkish monetary policy agenda on the back of a strong economic recovery and above target inflation.

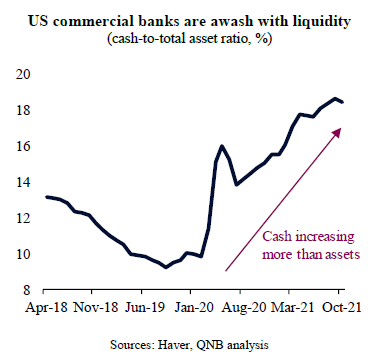

Second, to the extent that the US real economy still needs support to achieve pre-pandemic levels of employment, there is little evidence that more liquidity would be the right instrument to promote real growth and new jobs. Currently, money supply growth is not feeding credit growth. Excess reserves are abundant in US commercial banks as they are holding much more cash than they need for their commercial operations. The cash-to-total asset ratio of lending institutions, which captures liquidity conditions in the banking sector, has surge to close to all time highs. Therefore, QE is currently not supporting the economy while it is still contributing to asset price inflation which, indirectly, also feeds into consumer price inflation.

Third, as the Fed playbook requires the end of QE before any policy rate increases, the Fed is creating the conditions for a rapid response to potential price pressures on the inflation front. In other words, the Fed wants to be done with the QE tapering process as soon as possible so that it can quickly raise rates in case inflation accelerates further from here, requiring stronger action from policymakers.

All in all, the hawkish pivot is real. In our view, the pace of Fed tapering or QE reduction will likely increase to USD 30 Bn per month from the current USD 15 Bn per month. This implies that the QE is set to end in Q1 2022. In principle, this can pave the way for rate hikes already in H1 next year. However, we expect it to be much more difficult to implement rate hikes than QE tapering. This leaves us to place a question mark on the expected pace of rate hikes in H1 2021, given that the macro environment remains uncertain, in light of re-newed Covid-19 concerns with the Omicron variant.

Download the PDF version of this weekly commentary in English or عربي