The globalisation of supply chains for manufactured goods has been one of the key drivers of increasing prosperity over the past few decades. Indeed, it underpins a concept called “Factory Asia”, whereby factories in low labour cost Asian economies assemble high-tech components manufactured in more advanced Asian economies. Historically China has played a huge role, with it and its neighbours producing almost half of the world’s goods. However, as China seeks to move up the value-chain, and also driven by ongoing trade tensions with the US, supply chains have been shifting to include more factories in other lower-cost Asian economies, such as Vietnam and Cambodia.

These shifts were causing some degree of stress in the global supply chain, even before the Covid-19 pandemic hit last year. Now, exacerbated by the pandemic there is a risk that supply chain constraints will get worse before they eventually get better.

Three main factors are constraining global supply chains: unprecedented demand for manufactured goods; constrained production capacity; and bottlenecks in global logistics. This week we take stock of these factors, before noting the implications for inflation and the global economic recovery.

First, unprecedented demand for manufactured goods was caused by both fiscal stimulus in wealthy countries and by people being forced to live and work from home for much of the past year. Fiscal stimulus boosted incomes and spending more time at home increased demand for electronics and durable consumer goods such as domestic appliances. Going forward, we anticipate demand for manufactured goods to remain at a high level for the rest of this year due to low levels of inventory, shipping delays and a substantial backlog of unfulfilled orders.

Second, production capacity in Factory Asia has been constrained and may continue to be constrained.

The Delta wave of the pandemic has hit Asian economies particularly hard because of relatively low levels of vaccination and the fact that the Delta variant is more infectious. Therefore, ongoing, albeit still localised, lockdowns were necessary to control the pandemic over the past few months. This directly limited production capacity in some factories, but also cascaded further down the supply chain due to shortages of key components. Fortunately, the number of new infections has started to fall in most Asian countries and reduced the need for further lockdowns. Even so, it is expected to take months for component shortages to abate.

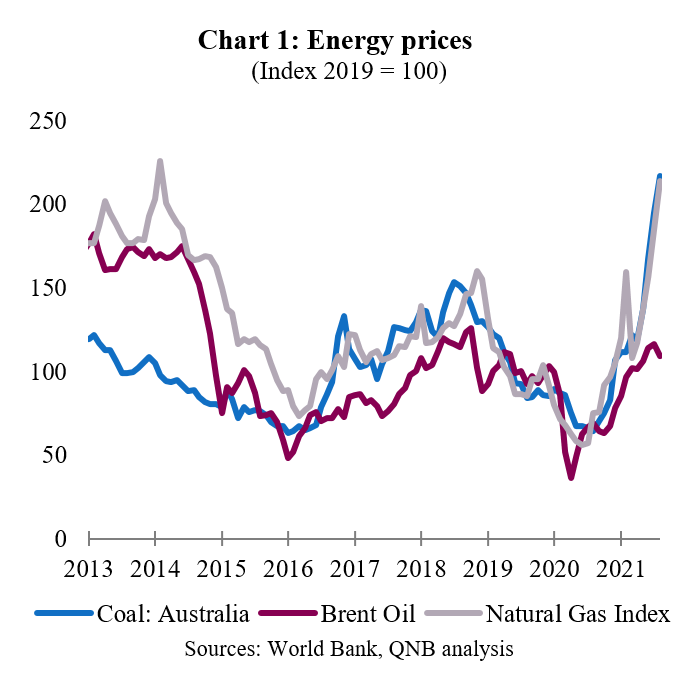

Going forward, the persistent rise in energy costs risks introducing a new constraint to production capacity in energy intensive manufacturing sectors. Energy prices have recovered strongly from low levels at the peak of the pandemic last year (Chart 1) and there is a risk they could rise further, especially if there is a particularly cold winter in the Northern Hemisphere. This raises the prospect of energy rationing, where production levels are reduced in energy-intensive industries to ensure heat and power are available for residential use.

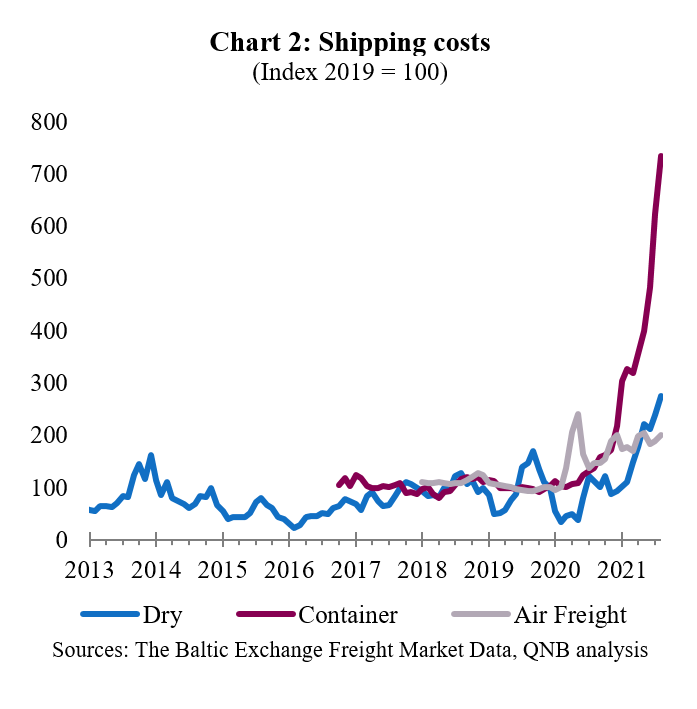

Third, a number of factors have contributed to ongoing delays and bottlenecks in global shipping and logistics. The result can be seen across three key metrics, air freight (for perishable and urgent deliveries), dry shipping rates (e.g., for coal or iron ore), and container shipping rates (Chart 2).

Ocean shipping cost increases and bottlenecks have been driven mainly by the impact of the pandemic on crew. Restrictions on entering countries and quarantine requirements have made it much more difficult and expensive to relieve and replace crew on ships. This has caused delays and increased costs for all types of maritime shipping.

At the same time, restrictions on international travel massively reduced the number of passenger flights (which also carry a considerable amount of air freight). Airlines have shifted resources (pilots, landing slots and even refitted some planes) towards their cargo operations, but demand still out-weighs supply resulting in high and rising prices.

Although the precise factors and details are constantly evolving, problems persist in global supply chains and they may get worse before they get much better. This has important implications for our views on both inflation and the economic recovery. Supply chain constrains act as a speed-limit for the global recovery in economic activity. Some output maybe lost forever. Production in some sectors may be unable to catch up before demand for goods and services return to more normal patterns. Whereas, the underemployment of workers, particularly in countries with limited fiscal space to support them, can lead to lost income and lower consumption. Persistent constraints in global supply chains will also cause inflation to remain elevated for longer. This in-turn limits the policy space available to central banks to maintain the current level of monetary stimulus. Expectations of tighter monetary policy could act as a further headwind to the recovery of global economic activity.

Download the PDF version of this weekly commentary in English or عربي