Late last year, the Euro Area was facing significant headwinds from a battery of deep and broad negative shocks. In addition to the legacy of Covid-pandemic related disruptions, the region faced the geopolitical spillovers from the Russo-Ukrainian conflict, high and rising inflation rates, and the prospects of an imminent energy crisis during the winter. However, against this pessimistic backdrop, the Euro Area economy was proving unexpectedly resilient.

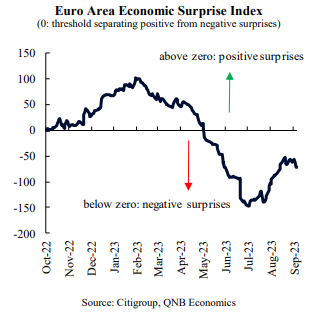

The Economic Surprise Index, which provides a measure of how data releases stand relative to expectations, remained well inside the positive range during the beginning of the year. This signalled that the economy was outperforming forecasts, as it managed to avoid a widely anticipated contraction in GDP.

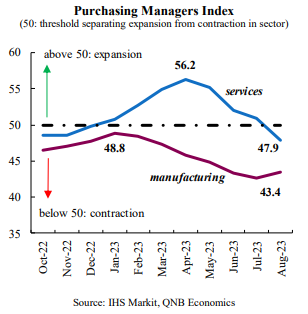

However, the series of negative shocks gradually started to take a toll on the economy after the first quarter. The deterioration in manufacturing became evident first. The Purchasing Managers Index (PMI), which is a survey-based indicator that reflects the direction of economic activity, showed that manufacturing was already contracting in the second half of 2022, and the negative trend deepened severely throughout this year as the Chinese recovery decelerated and global inventories became full. The service sector, which accounts for approximately 70% of the economy, had been supporting the economy, but finally entered the negative range in August on the back of continuous headwinds associated with tighter financial conditions and lower real incomes. At that time, weakness was evident across the board, with PMIs pointing to contractions in both services and manufacturing in the four largest Euro area economies (Germany, France, Italy, and Spain). In this article, we discuss three factors that contribute to a continuously weak performance for the Euro area economy over the next several quarters.

First, financial conditions are set to remain tight on the back of higher monetary policy rates and central bank balance sheet normalisation. To fight inflation, the European Central Bank (ECB) has increased its policy rates by 425 bps since June of last year. Additionally, the monetary institution continues to revert the balance sheet expansion that was put in place during the pandemic, which will further restrain the availability of credit. In addition to higher credit costs for households and firms, credit availability has become more constrained given the stricter lending standards set by banks. As a result, adjusted for inflation, credit is already contracting at a rate of 4% in year-over-year terms.

Tight labour markets, recovering energy and commodity prices as well as high inflation rates for services continue to fuel inflation pressures. This calls for the ECB to maintain stricter monetary conditions for a longer period of time, which will weigh on economic growth.

Second, global trade became a headwind for the Euro area as the global economy continues to slow down. Global trade volumes are expected to grow by 1.7% in 2023, a weak mark compared to the 2.5% average of the 5-year pre-Covid pandemic period of 2015-2019. This is already having an impact on the Euro area, and in particular in the more manufacturing-oriented countries. During the first half of the year, the evolution of exports implied a negative contribution to growth of 0.3% in the Euro area, and trade will continue to represent a limiting factor to growth for the remainder of the year. The sharp deceleration of growth in China is likely to amplify these problems, particularly for countries with strongest linkages to this Asian economy, such as Germany, the Netherlands, and France.

Third, the Euro area faces significant challenges associated with energy vulnerability and a high dependency of oil and gas imports. This vulnerability is even more pronounced in the industrial sector, with Germany's manufacturing base being particularly susceptible to potential gas shortages. There are currently limited short-term alternatives to Euro area imports of Russian energy. These negatively affects gross fixed capital formation in Europe. In the foreseeable future, energy vulnerability will continue to weigh on investment decisions.

All in all, going forward we expect weak economic growth in the Euro area given tight financial conditions, weak external demand, and lasting energy vulnerability. We expect the economy to grow 0.6% this year, and to remain stagnant in 2024.

Download the PDF version of this weekly commentary in English or عربي