Last year started on a positive note for the global economy. Bullish sentiment was rampant while overall activity was setting the stage for another period of accelerating expansion. In January 2020, the International Monetary Fund (IMF) projected that the global economy was set to grow at a healthy pace of 3.4% for the year. However, global conditions took a dramatic turn with the spread of the Covid-19 pandemic.

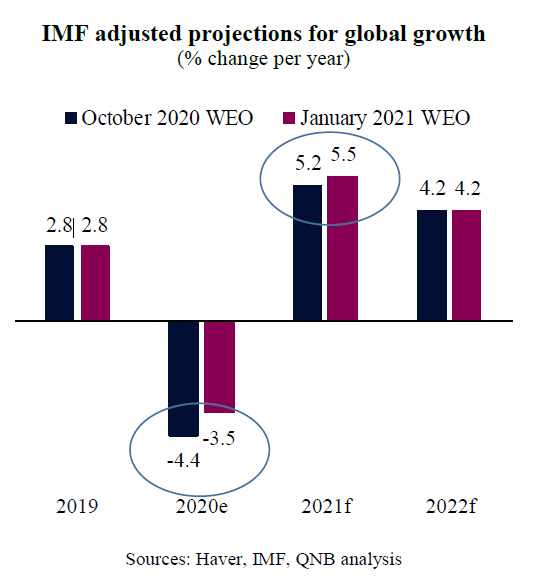

As the pandemic plagued the global economy with a collapse in demand and activity, the IMF downgraded its growth projections for 2020 to a 4.4% contraction in October, on a previous update to the World Economic Outlook (WEO). That was part of what the IMF labelled as “a crisis like no other.”

But conditions have improved since Q3 2020 and the IMF has started to take stock of the changes in its most recent WEO report, from late January 2021. Four points summarize the updated IMF take on the global economy.

First, the global economy is estimated to have performed better than previously anticipated last year. While in October the IMF projected a global GDP contraction of 4.4% for 2020, it now estimates a smaller contraction of 3.5% for the same period. The difference is attributed to a stronger-than-expected recovery in private consumption and fast adjustments to work-from-home, which boosted global demand and alleviated potential supply-side constraints. Importantly, all major economies (US, Euro area, Japan and China) outperformed previous expectations in the second half of 2020.

Second, global growth for the year is expected to be stronger than previously projected. According to the IMF, the global recovery is set to accelerate. In fact, the IMF has upgraded its projections for global growth this year to 5.5% from 5.2% in October. Key reasons for the upgrade include additional policy stimulus from large advanced economies and the development of several effective vaccines, therapies and Covid-19 containment efforts. Expectations of a vaccine-powered strengthening of activity later in the year outweigh the current drag on near-term momentum due to rising Covid-19 infections.

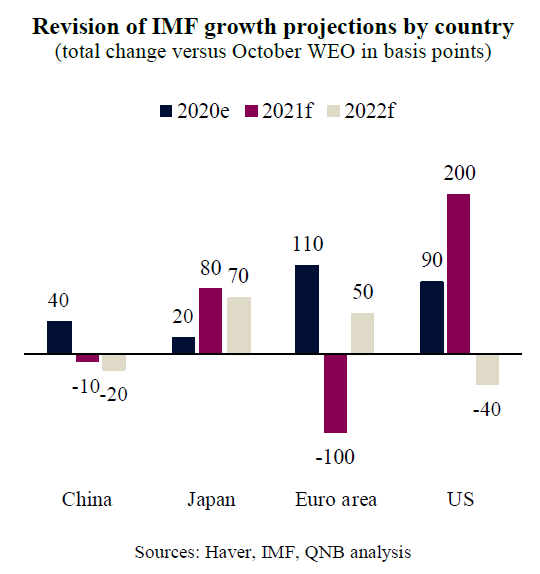

Third, recoveries will diverge across countries and regions, producing an uneven path to economic normalization. The strength of the projected recoveries varies depending on the severity of the health crisis, the extent of supply chain disruption (related to the structure of the economy and its reliance on contact-intensive sectors), the deployment of effective vaccines, and the effectiveness of policy support to limit persistent damage. Due to larger than expected fiscal stimulus programs and effective immunization and Covid-19 containment policies, the US and Japan had significant upgrades on their growth prospects. The Euro area, however, had a significant downgrade on their growth projections for 2021, as the region suffers with new waves of severe epidemics and struggles to secure prompt access to effective vaccines.

Fourth, despite the “exceptional uncertainty” surrounding the baseline projections, the balance of risks is well levelled. On the upside, further favourable vaccine news could increase expectations of a faster end to the pandemic, supporting the confidence of corporates and households. On the downside, activity could turn out weaker if the virus surge (including from new Covid-19 variants) proves difficult to contain before vaccines are widely available, and social distancing measures or lockdowns prove stronger and longer than anticipated. Moreover, the recovery is also vulnerable to policy mistakes, particularly an early withdrawal of policy support in key countries such as the US, China or the Euro area.

All in all, despite short-term challenges associated with new waves of Covid-19 and a softer recovery in Europe, the IMF has presented a positive outlook for the global economy. Recent economic performance has been stronger than anticipated, growth projections were upgraded and the balance of risks seems to be “neutral” rather than tilted to the downside for the first time in years.

Download the PDF version of this weekly commentary in English or عربي