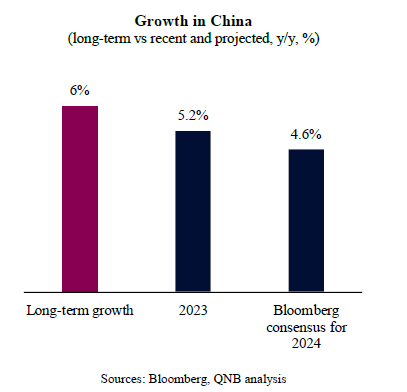

Pessimism about China’s economic performance seems to be pervasive amongst investors, economists and analysts. This is well captured by the Bloomberg consensus, a tool that tracks forecasts from economists, think tanks and research houses, presenting a range of projections as well as the median point of market expectations for growth in a given country. The Bloomberg consensus forecasts point to a tepid 4.6% Chinese growth in 2024, 60 basis points (bps) below last year’s growth and 140 bps below the country’s long-term growth average.

Weaker growth expectations are following a period of sequential negative headwinds for China. These included a sudden stop in momentum following the final wave of the pandemic in China in 2022, a real estate crisis, lacklustre policy support, a deep global manufacturing recession, and private sector uncertainty associated with aggressive regulatory clampdowns on innovative companies.

However, despite all of the headwinds and negative expectations, there is some room for moderate optimism when it comes to growth in China. In our view, three factors sustain an above-consensus 5% growth for the country in 2024.

First, the government has just announced 5% GDP growth as a significant economic KPI for the year, suggesting that more aggressive policy measures are on the way. This comes on the back of Chinese policymakers becoming more concerned about the domestic economic slowdown. We anticipate that Chinese authorities are now keen on pivoting their macroeconomic policy stance from neutral to supportive or accommodative. Policy actions so far had included only a few rounds of interest rate reduction, liquidity injections and limited spending in infrastructure projects. However, recent declarations from both fiscal and monetary authorities seem to justify the more aggressive growth target of the government. On the fiscal front, the government set the broad fiscal budget deficit at 6.6% of GDP, much higher than market expectations. Moreover, the central and local governments still have untapped resources from last year to deploy in 2024, which could increase the “effective” fiscal deficit to 7.7% of GDP. This would amount to a large fiscal impulse. On the monetary front, officials from the People’s Bank of China (PBoC), the country’s central bank, have been indicating additional easing measures over the next several months.

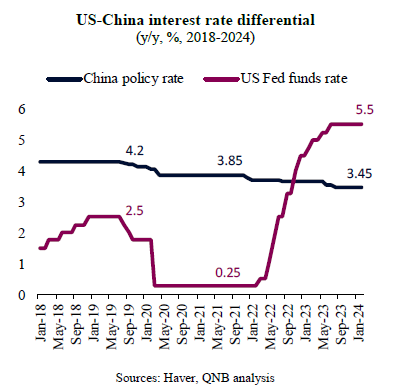

Second, the start of the easing cycle in the US later this year is also set to support a more aggressive round of stimulus by the PBoC. Once the Fed starts cutting rates for the first time in more than four years, the PBoC will have more policy room to ease further without creating additional incentives for capital outflows from China. In recent years, the US-China interest rate differential changed dramatically in favour of the US, with higher US yields attracting capital inflows from the rest of the world, including China. This created pressure in the renminbi, which depreciated by 14.3% since its recent peak in February 2022. As foreign exchange stability is one of the monetary policy targets of the PBoC, monetary authorities could not provide more significant support to the weakening Chinese economy. Hence, a Fed easing cycle should unlock more monetary stimulus from the PBoC, providing a tailwind for the Chinese economy.

Third, manufacturing is expected to be more supportive for Chinese growth over the coming months. After an unusually deep and long “global manufacturing recession,” which has been in place since 2022, a positive turn towards an expansion cycle is expected. The Global Manufacturing Purchasing Manager’s Index (PMI), a timely indicator of whether activity is improving or deteriorating, has bottomed in July last year and improved thereafter. The latest print, from February 2024, already points to expansionary activity. An expansionary manufacturing cycle often gains momentum rapidly and lasts for about 1.5 years. This is expected to be supportive for China, as manufacturing represents 26% of the country’s GDP.

All in all, while we do not expect strong growth for China this year, we believe general market expectations are too negative. A stronger commitment from the Chinese government for stronger growth, more monetary policy room for rate cuts and a more supportive global manufacturing cycle should support economic expansion around the official 5% target.

Download the PDF version of this weekly commentary in English or عربي