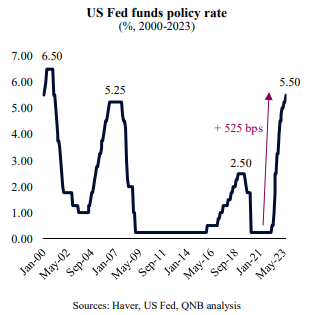

The US Federal Reserve (Fed) has been on the move to revert a decade-long approach of ultra-easy monetary policy since March last year, when untamed inflation forced it to increase policy rates for the first time in more than three years. This marked the beginning of one of the most dramatic and unexpected monetary tightening cycles in US history.

After a short-lived “pause” in interest rate hikes at the Federal Open Market Committee (FOMC) in June, the Fed decided to hike again at their last meeting late last month. The most recent action, another 25 basis points (bps) increase in interest rates, accounts for the 11th hike so far this cycle, including the aggressive “jumbo” 75 bps hikes of the second half of 2022. Taken together, 525 bps of hikes now places the Fed funds policy rate at 5.25-5.5%, the highest level in more than 20 years.

While the Fed has been moderating the pace of its tightening cycle since December 2022, with milder rate hikes and even the “pause” in June, uncertainty remains. There is still an unfinished debate about whether the Fed is ready to wind down, “pause for longer” or even pivot the policy rate changes sooner rather than later in early 2024.

The debate has gained further momentum as recent inflation prints have surprised to the downside, pointing to a rapid conversion of price changes towards the Fed’s 2% official target. In fact, the headline consumer price index (CPI) peaked at 9.1% in June 2022, before moderating to the 3% figure from the latest print.

Market participants are overwhelmingly expecting that the Fed has finished its hiking cycle and that rate cuts should start in Q1 2024 and continue throughout the year. The Fed’s Chairman, Jerome Powell, has been more cautious, suggesting that future decisions should be rather data dependent.

In our view, despite the rapid progress in cooling down inflation over the last few months, we believe that the Fed would lean “hawkish” amid uncertainty, potentially even hiking rates further this year. Three main factors support our position.

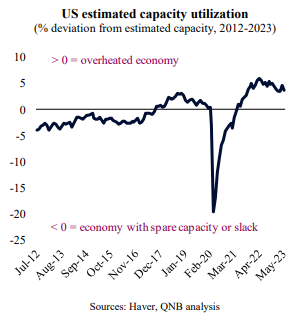

First, the US economy is still significantly overheated which leaves little room for complacency. US capacity utilization, measured taking into account the state of the labour market as well as industrial slack, suggests that capacity constraints still exists. In other words, there is currently higher demand for labour than employees available, whereas industrial activity is running above its long-term trend. These conditions may lead to rapid price increases should commodity prices recover or domestic consumption re-accelerates. The Fed is unlikely to cut rates or even pause for too long until the labour market eases further and industrial spare capacity increases, providing a buffer for the economy to absorb shocks without the risk of rapid inflation outbursts.

Second, tailwinds from commodity prices for inflation control are likely to reverse over the coming months. After declining by 22% from their peak in May 2022, commodity prices are stabilizing and are set to recover further, particularly as inventories drawdown and the global manufacturing cycle bottoms. Moreover, a potential escalation of the Russo-Ukrainian conflict can create further upside risks for commodity prices, including energy and grains. This would add to other capacity constraints, fuelling a re-acceleration of inflation.

Third, the US economy is proving more resilient than previously expected and further positive surprises on growth would place a floor in inflation. Real GDP increased by 2.4% in Q2, well above most estimates of trend growth. The Fed’s high-frequency activity index has increased significantly in recent weeks, suggesting that growth momentum remained strong going into Q3. This is reflected in the Atlanta Fed’s GDPNow “nowcast,” which is currently pointing to a robust 3.5% growth this quarter. This underlying strength is likely to add more pressure for the Fed to lean “hawkish,” given its need to maintain a 2% inflation target.

All in all, despite the aggressive rounds of rate hikes so far, and substantial gains in terms of inflation moderation, we believe it is too early to proclaim a “victory” over high inflation and an end to the tightening cycle. Capacity constraints, commodity headwinds and a re-accelerating US economy may contribute to reverse the inflation direction over the short- or medium-term.

Download the PDF version of this weekly commentary in

English

or

عربي