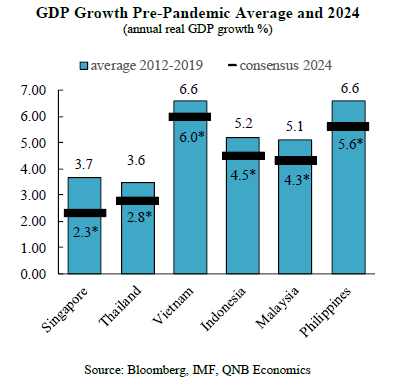

In recent decades, Southeast Asia has been the most dynamic region in the world, showcasing the brightest economic growth performance. The six largest countries of the Association of Southeast Asian Nations (ASEAN-6), which includes Indonesia, Thailand, Singapore, Malaysia, Vietnam, and the Philippines, have been among the fastest growing economies in recent times. With the end of the Covid-pandemic, it was expected that these countries would return to the strong growth rates of previous years. But 2023 turned out to provide a less supportive environment than had initially been projected, and in 2024 the ASEAN-6 economies will continue to underperform relative to their pre-pandemic growth rates.

In this article, we discuss two key factors that point to below-trend growth for the ASEAN-6 economies during 2024.

First, external demand will remain soft this year, which implies weaker support for economic growth of the highly globally-integrated ASEAN-6 countries. International trade is a key determinant of growth for the ASEAN-6 economies. In fact, exports represent 20-30% of GDP for Indonesia and Philippines, 65-95% for Thailand, Malaysia and Vietnam, and as much as 180% for Singapore. In 2023, world trade performance was disappointing, with the latest preliminary estimates suggesting that it contracted slightly. During the last 40 years, a contraction in global trade was only observed in 2009, as a result of the Global Financial Crisis (GFC), and in 2020 with the Covid-pandemic.

This year, we expect a mild recovery, with international commerce set to expand by around 2.8% on the back of an upturn in global manufacturing. Although this pace of growth is an improvement relative to last year, it implies a significant under-performance relative to the long-run average of 4.6% during 2000-2022. Given the importance of trade for the ASEAN-6 economies, this slowdown represents a major headwind for economic growth, making it more difficult for the region to return to pre-pandemic growth rates.

Second, higher interest rates in the major advanced economies (AE), as well as in the ASEAN-6 countries, have set a more challenging environment for economic growth. In advanced economies, interest rates are at the tightest levels in years. The U.S. Federal Reserve and the European Central Bank have increased their policy interest rates by 525 and 400 basis points (bps), respectively, since mid-2022. Although the two major AE central banks have reached the end of their tightening cycles, and are now debating the timing for rate cuts, the process will be gradual and policy rates are expected to stabilize at higher levels than in the previous economic cycle.

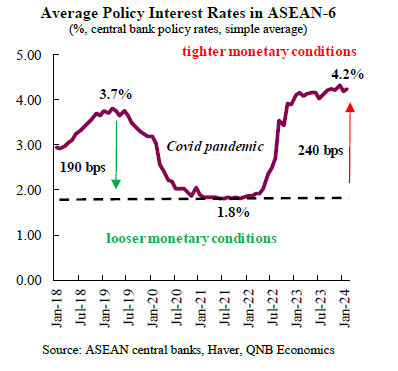

Similarly, central banks in the ASEAN-6 countries implemented their own monetary tightening cycles in order to contain spiralling prices. In these economies, the average increase in policy rates was 240 basis points (bps), to levels above those at the onset of the Covid-pandemic. The central banks in the region are expected to reach a turning point in monetary policy by mid-year, given softening economic growth and sustained downward trends in inflation. However, given the still relatively high levels of interest rates, and the lagged effects of monetary policy, they will continue to be a drag on activity over the next several quarters.

All in all, while growth in ASEAN-6 is still robust by international standards, it is below its pre-pandemic historical performance, given weaker external demand as well as tighter domestic and international financial conditions.

Download the PDF version of this weekly commentary in

English

or

عربي