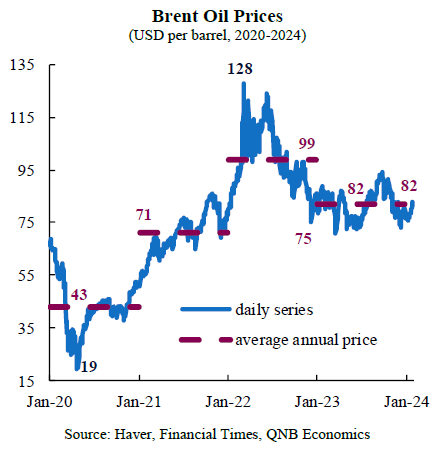

The beginning of the Covid-pandemic in early 2020 marked the beginning of a period of significant bouts of volatility in commodity markets. For crude oil, in particular, major global events represented substantial shocks to markets, leading to extreme upward and downward swings in relatively short periods of time. Initially, the Covid-pandemic represented a major negative shock to demand, given large-scale global lockdowns. This led to a temporary collapse in market conditions, as inventories were above full capacity whilst demand was at multi-decade lows. The price of Brent crude, the most relevant benchmark for global oil markets, bottomed at USD 19 per barrel mark in April 2020.

Thereafter, from the low in April 2020, crude oil prices experienced a remarkable turnaround. This was supported by a faster than expected post-pandemic global recovery, as well as active output management by OPEC+ member countries. The beginning of the Russo-Ukrainian war provided an additional boost, leading to a new spike that brought the Brent benchmark to USD 128 per barrel in March 2022.

After the peak, crude prices corrected significantly. On the demand side, given the slowdown in advanced economies, and the relatively moderate strength of the re-opening of economic activity in China from Zero-Covid policies. On the supply side, OPEC+ increased output to counterbalance the expected excess demand, while major economies (U.S., Europe, and China) managed emergency releases of strategic oil reserves. As a result, there was a correction in oil prices in 2023 to an average of USD 82 per barrel. Importantly, supply and demand balanced, stabilizing prices around the annual average, which fluctuated between a low of USD 71 and a maximum of USD 94 per barrel. These are milder variations relative to the large swings in 2022, when prices had moved between a low of USD 75 and the peak of USD 128 per barrel. Moving forward, Brent prices are expected to remain supported at current levels around USD 80 per barrel. We discuss key factors that support our view.

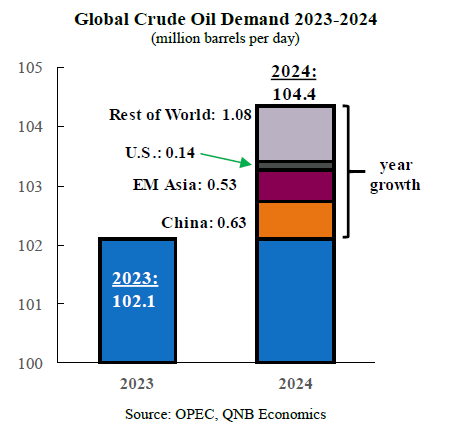

First, on the demand side, the macroeconomic outlook for China, the rest of Emerging Asia (including India), and the U.S. remains robust, which will boost growth in global oil consumption. In China, although the post Covid-pandemic recovery was not as impressive as initially expected, growth remains firm. In its last World Economic Outlook, the IMF increased the 2024 growth forecast for China to 4.6%, from the previous 4.2%, reflecting new fiscal support from the government. Additionally, sustained expansion in the petrochemical industry, as well as jet fuel demand from expanding air transportation, will provide further backing in this economy. Expected growth of 6.5% for India and 4.7% for the ASEAN-5 economies (Indonesia, Malaysia, Philippines, Singapore, and Thailand) will also be key contributors to demand this year.

The U.S. represents approximately 20% of world oil demand, and is therefore one of the key drivers of hydrocarbon markets that needs to be monitored. The recent data releases showed that real GDP continued to expand at a healthy pace in the U.S., beating consensus expectations by a significant margin in the last two quarters of 2023. Consumption remains strong in the world’s largest market due to firm labor demand and healthy household balance sheets. The likelihood of a recession, although not entirely discarded, has fallen considerably, and now the most likely scenario points to a “soft landing”. Taken together, these factors should be supportive for oil demand.

Second, on the supply side, the unexpected surge in volumes available at the market during 2023 is set to exhaust itself. The use of strategic reserves, as well as the record drawdown of commercial stocks, led to multi-decade lows in overall oil inventories, which is a concern for energy security. This calls for official net purchases for re-fulfilment of stocks, resulting in additional demand. On top of this, OPEC+ countries decided to enact output cuts in order to sustain prices at higher levels. Finally, investments were made during the energy crisis in 2022-2023, suggesting less room for additional investments and supply growth in 2024. Hence, supply volumes are unlikely to surprise to the upside.

To put current conditions into perspective, it is worth considering that, in relative terms, oil prices are not particularly expensive. The overall cost of oil demand amounts to approximately 2.8% of 2024 expected global nominal GDP. This is significantly below the historically critical threshold of 5% of GDP, when the “oil price burden” starts to weigh on consumption and investment in a significant way. If the cost of global oil consumption was at 5% of world GDP, Brent prices would average USD 145 per barrel. This implies that the global economy could absorb Brent prices at much higher levels before global demand is more seriously impacted. Furthermore, at the time of writing, Brent prices are up 24% from pre-pandemic levels, underperforming other major commodities, such as gold and copper, which have increased 33% and 38%, respectively.

All in all, crude oil prices are expected to stabilize near current levels, as physical markets will tighten on the back of decelerating supply growth and still robust global demand. We therefore expect oil prices to fluctuate in a range close to USD 80 per barrel over the next few quarters, barring any significant surprises on the geopolitical front.

Download the PDF version of this weekly commentary in English or عربي