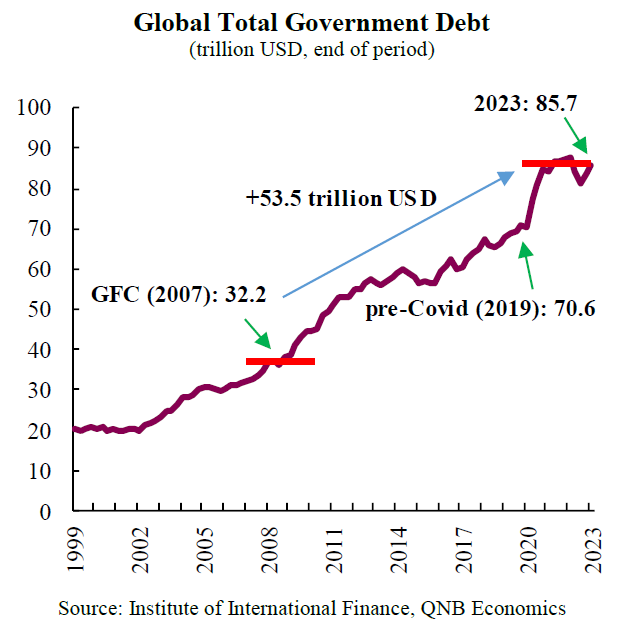

The Covid-19 pandemic represented a negative shock of unprecedented magnitude to the global economy, causing the sharpest contraction in activity ever recorded in quarterly national accounts. In response, extraordinary monetary and fiscal policies were put in place to provide support to households and firms, to preserve the economies from a deeper potential collapse. Low interest rates and quantitative easing from central banks, combined with expansionary fiscal policy, fuelled unprecedented credit growth. This resulted in skyrocketing public and private debt across the world, adding to the trend that had begun with the Global Financial Crisis (GFC). Since then, government debt has more than doubled to reach USD 85.7 trillion, while total global debt stands at USD 304.9 trillion.

Debt levels are not only high by historical standards, they are also expected to continue to rise broadly around the world. In the context of high and rising interest rates, debt becomes even more relevant as a potential drag to GDP growth. In our view, to understand the overall debt dynamics and the risks they pose for long-run growth, it is important to break down the origin of debt increases, as well as to differentiate between advanced economies (AE) and emerging markets (EM).

First, rising debt levels in AE are mostly accounted for by the deterioration of public sector accounts and the need to fund ever growing deficits. In 2023, total government debt in AE reached USD 59.7 trillion, an increase of 60% relative to the USD 37.4 trillion after the GFC, equivalent to 113.6% of global GDP.

High government debt levels in AE are set to harm growth by diverting resources away from investment. As governments increase their borrowing, the issues of new debt compete with the private sector for a given amount of savings available. As a result, real interest rates increase, which can “crowd out” private investment, and therefore limit economic growth.

Second, elevated corporate indebtness combined with higher interest rates can create a “debt overhang” problem that hinders investment by firms. The Covid-19 pandemic generated a massive disruption in economic activity that impacted sales and profits of firms around the world. In order to keep firms operational and contain the destruction of jobs, governments implemented injections of liquidity through loan guarantees as well as new lines of credit. Although, total debt in nonfinancial corporations as share of GDP has declined from its peaks during 2020 in both AE and EM, they are still above their pre-pandemic levels. Now, in a scenario with higher interest rates and tighter credit standards, this can result in a “debt overhang” in firms, where they will find it harder to obtain funding for new investments.

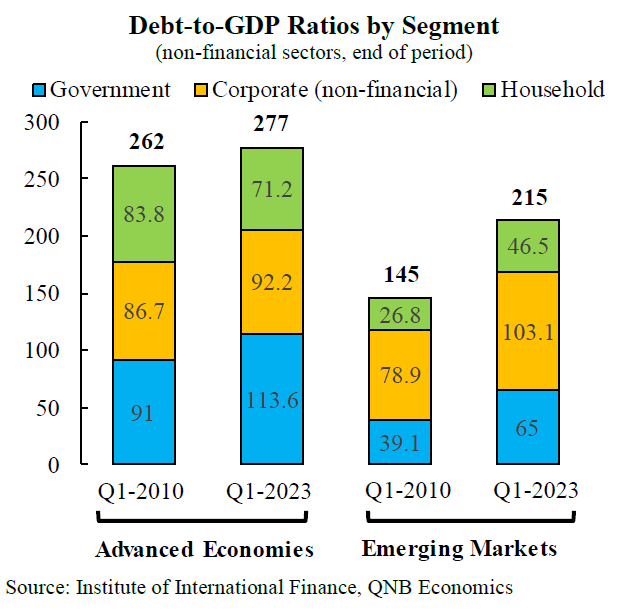

Third, an assessment of debt dynamics in EM requires a further differentiation between China and other EM. In the period from Q1-2010 to Q1-2023, China accounted for 65% of the growth in government debt, and 76% of growth in nonfinancial private debt in EM. In China, debt had a very particular form, as the country benefited from abundant domestic savings, the debt was mostly financed by residents in local currency. This prevents the country from suffering the standard balance of payment pressures that affect other EM during periods of economic stress. Hence, China is better positioned to engineer a deleveraging process in the future.

In contrast, debt in other EM tends to have a funding profile with more significant participation of external funding, or in hard currencies from advanced economies, making them vulnerable to external shocks and “sudden-stops” in capital inflows. Such vulnerability could be even more pronounced in the current scenario, where tighter monetary policy in major advanced economies pulls capital away from riskier EM. In the past, debt crisis in EM were triggered by sharp increases in international interest rates. High levels of debt now leave the more risky EM exposed to financial distress that can make refinancing difficult, and result in a crisis that resembles previous experiences.

All in all, unprecedented and rising debt levels pose significant risks to the global economy going forward, through the diversion of funds from productive investments, financial constraints in the corporate sector, and potential vulnerabilities in EM.

Download the PDF version of this weekly commentary in

English

or

عربي