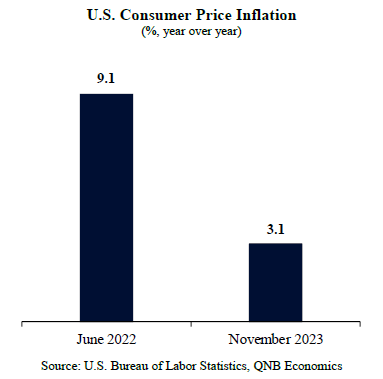

The outbreak of the Covid-pandemic in 2020 marked the beginning of a sequence of exceptional events that brought inflation rates to multidecade highs in the U.S. in 2022. At the initial stages of the pandemic, lockdowns imposed constraints in supply, followed by extraordinary monetary and fiscal stimulus that fuelled demand. Further pressure was put on prices by labor shortages and a major commodity shock triggered by the Russo-Ukrainian war, taking the rate of inflation to 9.1% at peak in June 2022.

Furthermore, as inflation was much above the target of monetary policy, the response from the Federal Reserve (the “Fed”) started, however only after some initial hesitation. The Fed embarked on a record policy rate tightening cycle to help bring down inflation. Since then inflation initiated a downward trend with a significant contribution from declining energy prices, as well as the normalization of supply-chain conditions.

Given the significant progress so far in reducing inflation, and the positive surprises in the latest CPI releases, some market analysts suggest interest rate cuts could come as soon as Q1-2024. In our view, however, while the ongoing slowdown in economic activity will further contribute to the fall in inflation rates, progress could be more gradual. Hence, we expect policy rate cuts to come later in Q2-2024. Moreover, even after a few rounds of rate cuts, we still expect to see policy rates at higher levels than before the pandemic for some time. In this article, we discuss the two main factors that support our view.

First, there is limited downside for energy costs to continue pushing headline (or total) inflation down. The Brent oil price peaked at an average of USD 124 per barrel (p/b) in June of last year, from USD 64 p/b in January 2020, before the start of the Covid-pandemic. As a result, at the height of the surge in prices, energy costs accounted for 3 percentage points (p.p.) of total inflation. These trends later reversed: as Brent oil prices fell to approximately USD 75 p/b in June 2022, energy costs helped bring down inflation.

However, since mid-2023 oil prices have remained relatively stable on the back of extended production cuts from OPEC+ on the supply side, and positive surprises on the demand side given improving growth expectations for the major world economies (U.S., Euro-Area, and China). Going forward, absent major negative shocks in the global economy, energy prices have little additional room to provide another sizable contribution to reduce inflation.

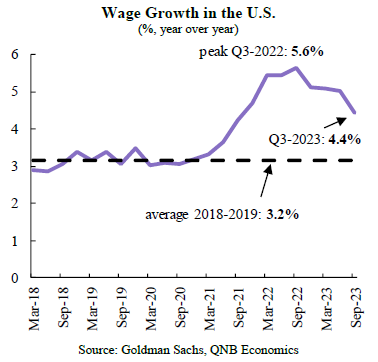

Second, tight labor markets continue to provide support to the demands of higher wages by workers, maintaining pressure on labor costs for firms. Unemployment rates in the U.S. have averaged 3.8% in the last 3 months, close to the historical minimums. Tight labor markets strengthen the position of workers in wage negotiations.

A useful gauge to measure the evolution of wages is given by the Wage Tracker Indicator. This meter shows that wages are growing at a 4.4% rate in the U.S., considerably above the 3.2% average of the two years before the pandemic. Although there are signs of easing in labor makets, it will take several quarters for wage growth, currently above inflation rates, to arrive to normal levels. The deceleration in wage growth is another signal of falling inflation, as there is less pressure on the costs of firms, although the pace and timing of the improvement is unclear.

All in all, inflation has come down significantly from its peak in the U.S. and should continue to moderate over the coming months. However, the Fed is likely to be cautious and prefer to wait to see clear progress in reducing non-energy inflation to avoid cutting policy rates too early.

Download the PDF version of this weekly commentary in English or عربي