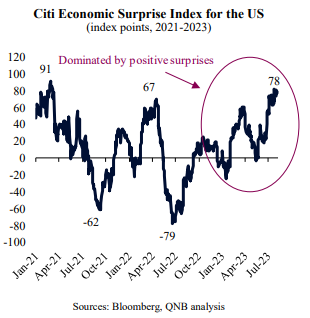

US economic growth has surprised to the upside in recent quarters, supporting global demand through a period of weakness associated with a “manufacturing recession,” policy tightening and increased geopolitical uncertainty. This can be observed by the US Citi Economic Surprise Index, which summarizes how relevant economic data releases have beaten or missed analyst expectations over a period of time. Positive surprises have been dominating negative surprises since late 2022.

In fact, it is not a daunting task to find macroeconomic and financial indicators supporting a bullish US growth story at this moment. Equity prices rebounded strongly and are close to all-time highs, GDP is currently growing above potential, and unemployment is hovering around multi-decade lows. However, one should take a more nuanced approach when looking into the data, as certain indicators tend to trigger warning signs much in advance of any material problem.

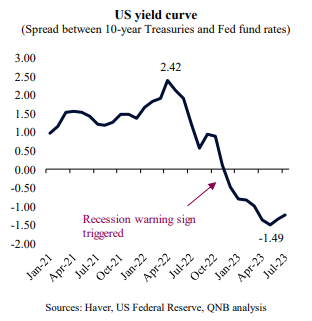

Importantly, macro-sensitive US Treasuries are pointing to a more complex backdrop. Different metrics from the US government yield curve, which is the yield differential between similar instruments with different maturities, have inverted. For example, the benchmark spread between 10-year Treasury notes and Fed fund rates turned negative in December 2022, before diving further into deep negative territory in recent months. This benchmark spread is a leading indicator of recessions as lower long yields imply lower growth expectations and higher short yields imply monetary tightening. This sign has flashed in advance of the last seven US recessions since the early 1960s, usually giving a year or two of warning before a recession starts.

Is this time different when it comes to the accuracy of the yield curve signal? Can the US indeed avoid a deeper recession over the next 18 months?

As US growth steadies and inflation moderates, investors and market analysts seem to be converging towards an optimistic position, implying that the US can indeed avoid a recession. This is due to the belief that US authorities are operating a “beautiful tightening,” where the Federal Reserve (Fed) calibrates policy to deliver an optimal “soft landing,” i.e., a policy mix that moderates growth just enough to push inflation back to the 2% target without causing any major stress in demand.

In our view, however, this position is too optimistic. Historically, the Fed was never able to contain runaway inflation with a “soft landing.” During previous tightening cycles, either policy action was not strong enough, leading to a disruptive pickup in inflation, or policy quickly became too tight, forcing a more pronounced economic downturn.

Uncertain long lags between policy measures and their impact in activity tend to make the prospect of policy calibration rather illusory. “Policy mistakes,” interpreted either as an over- or under- reaction to inflation, are the historical norm.

Currently, given the underlying strength of the US economy and the financial health of US households, we expect to see the US economy accelerating over the next few months.

According to the Atlanta Fed’s GDPNow model, which estimates real time growth with high frequency data, US growth is running at 5.6% in Q3 2023, almost three times most estimates of trend growth. Building permits increased, capital expenditure intentions are rising and the forward-looking Purchasing Managers’ Index (PMI) new orders-to-inventory ratio are implying a turning point to the manufacturing cycle back into expansion mode over the next few months.

Importantly, labor force participation among prime-age workers surpassed pre-pandemic levels. Hence, unless labour demand slows, real wages will rise, as there is very little room for a further increase in labour supply. Currently, wages are growing at 5.3% per year, significantly above the running 3.2% inflation rate. This supports real income growth directly and strong consumption activity indirectly. Similarly, capacity utilization is running hot, more than 2.5% above its long-term average, suggesting very limited supply side space to accommodate higher demand.

While these factors point to a robust US economy, it is not necessarily good news. Strong US activity, combined with tight labour markets and low spare capacity, is likely to lead to another wave of high inflation. At 5.3% growth, wages are running still twice as fast as the 2.5% growth that is necessary to support a further moderation of inflation towards the 2% Fed target. The half percentage difference is determined by the long-term average productivity growth. As long as wage and inflation growth are not in balance, the Fed is likely to enact more rate hikes. This risks a sharper downturn later in 2024.

All in all, the sign provided by the yield curve inversion should not be ignored. There are currently enough imbalances in the US economy to prevent a “soft landing” and eventually bring a recession in H2 2024.

Download the PDF version of this weekly commentary in

English

or

عربي