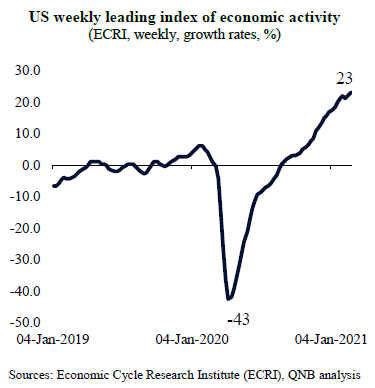

The US post-pandemic economic recovery is proving to be durable, lasting for several quarters and not showing any signs of receding. In fact, the US weekly leading index of economic activity, which is a composite of high-frequency data that tends to predict the business cycle by 3 to 10 months, still points to a rapid acceleration in activity at least for the next quarters.

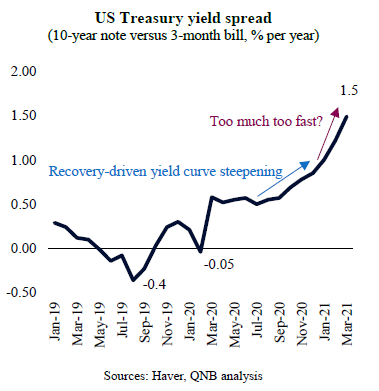

Macro-sensitive US Treasuries confirmed the positive backdrop. After recession fears and the Covid-19 shock that pushed the benchmark spread between 10-year and 3-month Treasuries to negative territory, the economic recovery produced a healthy steepening of the yield curve. This tends to be a positive leading indicator of economic expansions as lower short yields imply monetary stimulus and higher long yields imply higher growth or inflation expectations.

But in macroeconomics, one can have too much of a good thing. The strong US recovery is starting to suggest a build-up of new economic imbalances. Aggressive fiscal stimulus is driving investors to “price in” an overheating economy where inflation runs too fast. This is starting to lead to an abrupt spike of long-dated US yields.

Should this trend of a disorderly rise in long-dated US yields continue, financial conditions will likely tighten, potentially leading to a “hard landing” of equity prices and slower economic growth in the future. Higher yields could be detrimental to the highly leveraged US corporate and government sectors, increasing rollover risks and the overall debt burden. Importantly, access to cheap credit is a sine qua non condition to the survival of large swaths of the US corporate sector.

Within this context, the US Federal Reserve (Fed) is under increasing pressure to address the issue of rising yields sooner rather than later. Some analysts expect monetary policy actions to contain spikes in long-dated yields already in the upcoming Federal Open Market Committee (FOMC) meeting of March 16-17.

There are three monetary policy tools that the Fed can use to cap or contain long-dated yields. First, the Fed can deploy Japanese-style Yield Curve Control (YCC), a policy whereby the monetary authority would target some long-dated yield and pledge to buy enough long-term bonds to keep yields from rising above the target. This policy measure is perceived as aggressive as there is no notional limit of resources to be deployed in achieving the target rate.

Second, the Fed can enact a “twist” operation, by which it would sell part of its stock of short-term Treasury bills to reinvest in long-dated Treasury notes and bonds. The net effect would be a flatter yield curve with slightly higher bill yields and lower yields for notes and bonds. The objective of “twist”-type operations is to contain or lower long-dated yields without increasing the balance sheet of the Fed with new purchases of assets.

Third, the Fed can introduce a “duration extension” to its existing USD 120 billion monthly asset purchase program, whereby it changes the composition of purchases towards more long-dated securities and away from short-dated bills.

In our view, the Fed will likely resort to a combination of “twist” operation and “duration extension” to the existing asset purchase program. This would be a smoother transition from the current Fed policies and would give all economic agents time to evaluate the path of the current recovery and the inflation trajectory. All in all, the Fed is likely to tweak its monetary policy over the coming months, but a Japanese-style YCC policy seems too aggressive for the current circumstances.

Download the PDF version of this weekly commentary in English or عربي