Early in the year, negative narratives from investors and analysts dominated the global macro agenda. This followed a particularly arduous 2022, when market participants had to face the hard realities of subdued activity, high inflation, and geopolitical polarization.

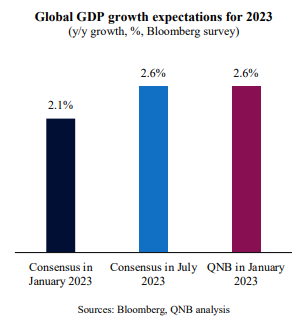

The gloomy environment in January 2023 translated into poor economic and market expectations for the year. In fact, the Bloomberg consensus forecasts pointed to a tepid global economic expansion of 2.1% in 2023, significantly below the long-term average of 3.4% and below the 2.5% mark that commonly define a global recession. The Bloomberg consensus is a tool that tracks global forecasts from analysts, think tanks and research houses, presenting a range of projections as well as the median point of market expectations.

But this proved to be too pessimistic, as we highlighted in our Economic Commentary from January 1st 2023: “… as we enter the new year in 2023, it is safe to say that a large amount of negative events is already discounted and understood. In our view, the previous series of downward revisions led to overdone pessimism about lower growth prospects. We therefore expect to see the global economy growing by 2.6% in 2023, with all major economies expanding at a faster pace than most analysts predict.”

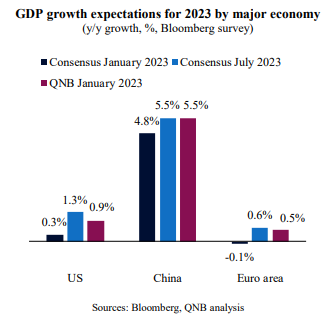

Halfway through 2023, our scepticism about the idea of an imminent global recession was justified, despite continuous monetary tightening, the US banking woes and industrial weakness across continents. Indeed, over time, consensus converged to a more positive outlook, as the US consumption and labour markets proved more resilient, the Chinese recovery surprised to the upside, and the Euro area downturn was mitigated by both a mild winter and more supportive fiscal policies.

Moving forward, however, we would caution against a full U-turn from too much pessimism to too much optimism. While we believe global growth will continue to be resilient in the face of multiple headwinds (monetary, fiscal, and geopolitical), we do not see scope for a further sequence of upward revisions. We rather maintain our growth projections from earlier this year. Three main factors support this cautious view of weak but supported growth for the rest of the year.

First, global consumers are unlikely to benefit from the same type of tailwinds that supported real disposable incomes in H1 2023. The sharp correction in commodity prices, down more than 30% in about a year, favoured a significant deceleration of inflation and inflation expectations. As a result, real wage growth and disposable incomes received a boost, which further supported consumption globally. But there is limited room for commodity prices to decline further. Global inventories are at record lows and supply growth should be limited, as further output increases require new investments that are not currently on the pipeline.

Second, higher monetary policy rates are affecting consumer spending and corporate investments. As time goes by, more homeowners will be affected by costlier mortgages. A similar logic is also valid for corporate debt. As credit becomes more costly through higher interest rates, overall investment spending will dampen private sector growth contribution. Hence, monetary policy is set to slowly permeate the real economy.

Third, following a period of expansion after its late post-pandemic “reopening,” China’s economy is losing steam again. Fiscal and monetary stimulus are so far limited, calibrated to sustain a normal level of activity but not to produce the type of investment booms that were part of the Chinese easing cycles in the past. While additional stimulus are expected for the rest of the year, we see no “policy bazooka” this time around. Hence, significant positive growth surprises from China are unlikely.

All in all, global growth has been more resilient than analysts and markets expected earlier this year. However, the room for positive surprises is now much more limited than it was six months ago, when excessive pessimism took over investors and economists.

Download the PDF version of this weekly commentary in

English

or

عربي