The year started with negative sentiment dominating the global macro-economic environment and outlook. On the monetary side, policy tightening from the US Federal Reserve and the European Central Bank is expected to continue until the middle of this year as inflation is still not fully abated. On the fiscal side, policy action is becoming less supportive in major advanced markets, and will consequently not be a key driver of economic activity. Furthermore, geo-political developments bring further uncertainty which also impact the economy, from intensifying competition and tensions between the US and China to the ongoing Russo-Ukrainian War. Last but not least, China’s Zero-Covid policy dragged economic activity domestically but also globally at the end of last year, due to renewed lockdowns amid multiple Covid-19 outbreaks.

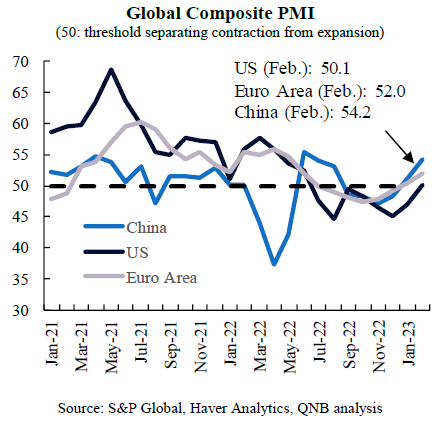

Despite these strong headwinds, economic data releases have shown positive surprises during the last few months. The latest Purchasing Managers Index (PMI) readings are providing support for this narrative. The PMI is a survey-based indicator that provides an assessment of improvement or deterioration in economic activity. An index level of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) business conditions. The PMI composite indicators reflect joint conditions in manufacturing and services.

In this article, we look at the latest PMI data for each of the major economies: the Euro area, the US and China.

In the Euro area, the Global Composite PMI had persisted below the 50-point threshold for six consecutive months in the second half of last year, but finally came into expansionary territory in January, with a further increase in February. The economy has proven more resilient than expected despite the adverse conditions caused by the conflict in Eastern Europe and its economic consequences. This included energy rationing, higher energy prices and lower disposable incomes. But negative factors were offset by fiscal support for firms and households hit by the energy crisis, the dynamism from reopening economies, a reversal of the spike in gas prices, and a relatively mild winter.

In the US, the economy at the end of 2022 was stronger than expected, with tight labour markets and an abundance of job opportunities, while consumers continued to spend from their large stock of savings. Although the PMI composite registered seven consecutive months in contractionary territory, it surpassed the 50 point mark in Februrary. This adds to the evidence that the US economy is still strong and more resilient to a sharp downturn than expected.

China is on its way to a significant economic recovery relative to last year. Economic activity had remained subdued given the lockdowns and restrictions after the resurgence of Covid-19, tighter regulation in several industries, and the withdrawal of stimulus policies. As a result, the PMI Composite prints were in contractionary terrain during the last four months of 2022. Authorities responded with monetary and fiscal easing, and support for unfinished real estate projects to offset the effects of the contraction in real estate investment. Together with the reopening of the economy, these measures pushed the PMI into expansionary territory and is expected to continue to pick-up in 2023.

All in all, despite the expected slowdown for the global economy for this year, advanced economies have shown more resilience, while economic activity in China should register a major economic rebound.

Download the PDF version of this weekly commentary in

English

or

عربي