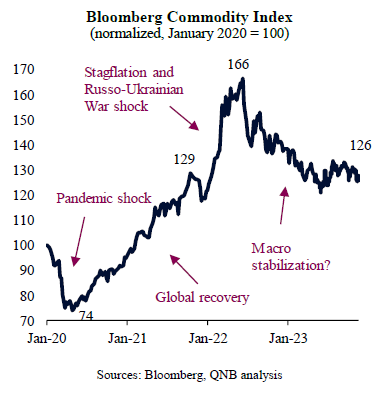

Commodity markets have been experiencing unprecedented bouts of volatility and dislocation since the pandemic started in early 2020. In fact, shocks to commodity markets have been so significant that prices followed boom and bust swings in relatively short order over the last few years.

The negative demand shock from the Covid-19 pandemic initially triggered deflationary pressures that rapidly pushed commodity prices to multi-decade lows. The Bloomberg Commodity Index, a leading benchmark for general commodity price movements, plummeted from January to late April 2020. However, it did not take long for unprecedented policy stimulus to spur a significant global economic recovery, which supported commodity prices. After a healthy period of economic recovery, excess global demand, combined with supply constraints and the Russo-Ukrainian conflict shock, led to a spiral of high prices in late 2021 and early 2022. High commodity prices seemed to have reached a zenith mid- last year, before a significant correction. This was mainly driven by the Chinese slow down, high inflation squeezing real incomes, and the unexpected increase of oil supply on the back of strategic inventory releases.

A closer look at commodity price movements can shed light on important aspects of the global economic outlook. The price development of selected commodities conveys relevant macroeconomic information, including trends on sentiment and inflation, often leading or confirming cyclical turning points. Our analysis focuses on three trends within the latest evolution of commodity markets that could be an indicator for the global macro outlook in the coming months.

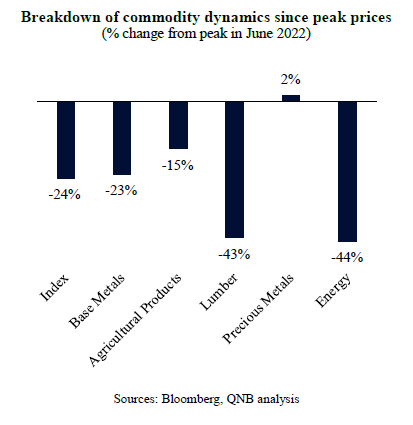

First, commodity prices seem to challenge the “soft landing” narrative, i.e., the idea that inflation can be brought back to the target of major central banks without causing a recession. In fact, commodity prices are pointing to at least a shallow recession across major advanced economies. This is expressed in the more pronounced correction of highly cyclical commodities, such as energy and base metals. Within energy, Brent crude oil prices, while still slightly above pre-pandemic levels, are down 37% from their recent peak. Within base metals and forest products, copper and lumber prices, important proxies for activity in China and the US, have also collapsed from their recent peaks. Such price performance suggests that the global growth outlook is still dominated by headwinds, despite the recent re-acceleration of the US economy.

Second, precious metals are also pointing to a weak global economy. Gold prices are close to all-time highs. However, silver prices, key as an input for the new economy (technology and clean energy industries), are significantly below its recent highs and have fallen significantly in recent months. This suggests that some pressures were released from the real economy as demand for silver tends to be cyclical. A rising gold-to-silver ratio amid a strong gold performance is a sign that deflationary pressures are taking hold with a slow down in overall demand and economic activity.

Third, the combination of robust gold prices with falling 10-year US Treasury yields in recent months suggests that investors are now more inclined to think that uncertainty is heightened and the global economy should slow down further. While gold seems to have de-coupled from inflation trends since the pandemic, it is still a traditional safe-haven asset to hold in times of uncertainty and negative macro developments. Higher safe-haven demand in highly macro-driven asset classes tend to be correlated to a cyclical downturn rather than periods of economic re-acceleration.

All in all, recent developments in commodity markets are not conveying a message of global macro strength, despite robust US consumers and the re-acceleration of the world’s largest economy over the previous quarter. The sharp correction in cyclical commodities point to more growth headwinds whereas precious metals suggest high safe-haven demand. Uncertainty is paramount in the global outlook and commodity prices point that the worst may not be over when it comes to economic activity.

Download the PDF version of this weekly commentary in English or عربي