The direction of the US economy is a topic that is discussed in controversy. To this day, there seems to be no clear consensus on whether the economy will enter a full-blown recession, if it will only experience a mild recession, or even if a recession can be avoided altogether. The picture is overall blurred, despite significant headwinds better-than-expected indicators since the beginning of the year have pointed to a resilient economy. Nevertheless, a recession is not out of the picture yet, and the questions of a much-anticipated downturn remain.

A recession is officially declared by the National Bureau of Economic Research (NBER) when there has been a significant decline in economic activity, which lasts more than a few months and, importantly in the current scenario, is spread across the economy. In a series of articles over the coming weeks, we will investigate and deep-dive further into different forward looking indicators from three categories (production, households, and market-based), to assess the current state of the US economy, and how the downturn is taking shape. In this issue, we discuss the outlook from the perspective of three production sectors (services, manufacturing, and construction).

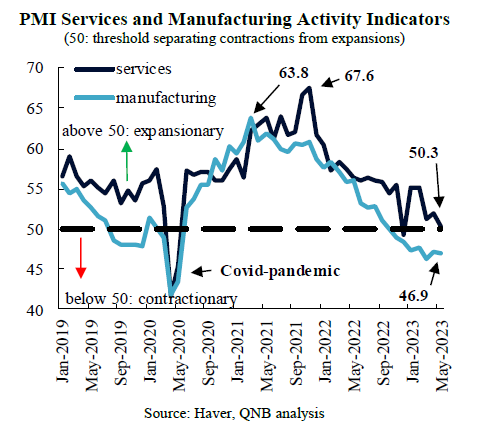

First, the service sector remains overall resilient, despite a gradual softening trend. The most recent Purchasing Managers Index (PMI) shows this evolution. The PMI is a survey-based indicator that provides an assessment of improvement or deterioration in economic activity. An index level of 50 serves as a threshold to separate contractionary (below 50) from expansionary (above 50) business conditions. During the strong recovery in 2021, the PMI for services reached a peak of 67.6, and then began a downward trend that continues to the latest readings. The releases this year until May have been above 50, still enduring in expansionary territory.

The service sector is acting as a stabilizer in the ongoing adjustment process of the economy. In general, compared to other sectors, services exhibit a smoother evolution over the business cycle, as well as more moderate reactions against changes in monetary policy. One reason for this is that consumption of services is less dependent on finance, making it less sensitive to interest rates. Additionally, households are less inclined to undertake sharp adjustments in the consumption of services, with some obvious examples being health and education. In contrast, households are more likely to postpone purchases of durable goods, such as cars and household appliances, when economic conditions deteriorate or financing costs become too expensive.

Furthemore, consumption in services has still not recovered to its pre-Covid pandemic trend, which implies that there is some additional room for growth going forward. The services sector is key for the performance of the US economy, as it accounts for over 75% of output, and employs over four out of five workers in the private sector. Therefore, a smooth adjustment in this sector is fundamental for a healthy economic dynamic. In other words, resilient services consumption implies that a sharp economic slowdown is less likely.

Second, the manufacturing sector is in contractionary mode, with a trend towards further weakening. The PMI for manufacturing began a downward trend after reaching its peak of 63.8 in March 2021, ahead of the service sector, and has been in contractionary territory since November 2022. This is partially explained by the transmission of higher interest rates to investments. Fixed investment growth has been negative for four consecutive quarters since Q2-2022. Additionally, and in sharp contrast to services, consumption of goods overshot markedly above its trend during the Covid-pandemic. This implies that there is still additional downside potential until consumption normalizes further.

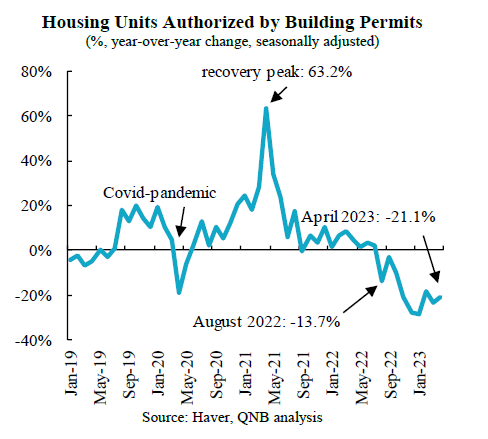

Third, the construction sector is contracting consistently and anticipates a recession. Higher interest rates and tighter lending standards have increased borrowing costs and reduced the availability of credit. Additionally, decreasing loan-to-value ratios imply borrowers have to post more equity to obtain a mortgage. As a result, property financing is becoming more expensive for prospective buyers as well as more difficult to obtain, having a negative impact on construction.

Building permits have displayed negative growth since August last year, and averaged -22.9% so far this year. Historically, consistently negative growth rates of this magnitude have anticipated recessions without exception, and are therefore a reliable signal of an upcoming recession.

All in all, data from key economic sectors show that the US economy is facing cross-currents. Taken together, we expect the economy to be heading to a soft-landing, or shallow recession, considering the resilience of the large services sector, against the more negative developments in manufacturing and construction. In upcoming issues, we will further analyse and complement our view on the US economy from alternative perspectives.

Download the PDF version of this weekly commentary in English or عربي