Euro area real GDP growth has fallen to just 1.0% y/y in Q4 2019, the slowest pace of expansion since 2014 when the Euro area began to recover from the sovereign debt crisis. This forced the European Central Bank (ECB) to undertake significant monetary stimulus in September 2019, which was Mario Draghi’s parting gift to Christine Lagarde before he handed the ECB over to her leadership.

We follow the Euro area economy and like to compare and contrast the four largest economies in our analysis. We do so again here, reviewing their relative growth performance and how monetary and fiscal policy can influence them in different ways.

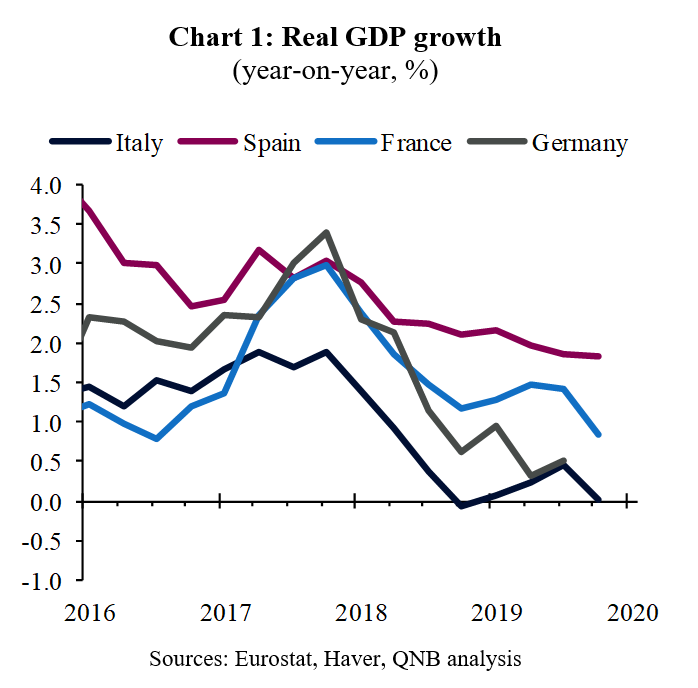

First we consider real GDP growth (Chart 1). Germany has historically been the strongest performing of the large Euro area economies, but it has suffered over the past two years due to its large export-orientated manufacturing sector. The recession in global manufacturing also noticeably weakened growth in both France and Italy. However, growth in Spain was supported by the benefits of past structural reforms.

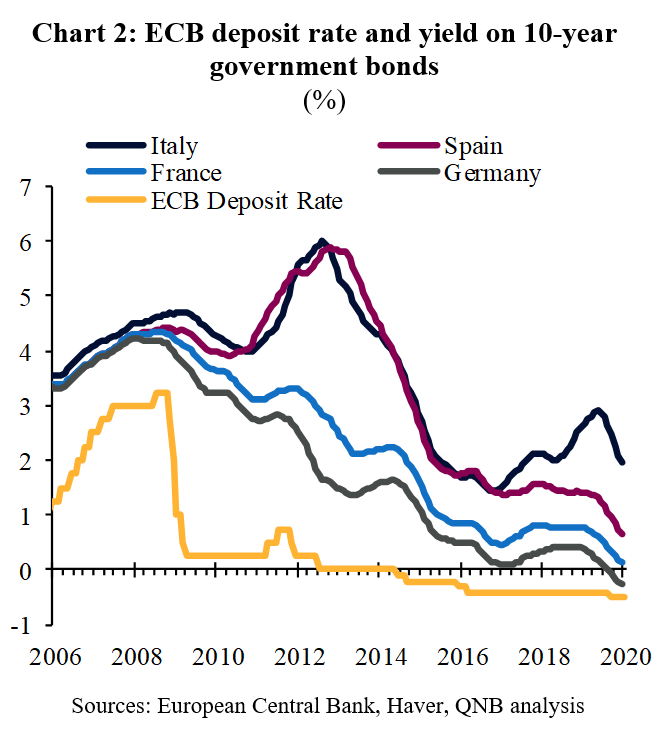

The ECB launched a stimulus package in September in response to the protracted growth slowdown, lower inflation and the persistence of significant risks to the outlook, notably global trade tension, Brexit and idiosyncratic political risks in Italy. The ECB’s stimulus will have supported credit growth in the Euro area, but the most obvious impact is on government borrowing costs. This is most clearly seen in the falling yields of 10 year government bonds (Chart 2). The country that has benefited most from this is Italy, especially as Italian yields were on an upward path in early 2019 due to arguments between the Italian government and European authorities over fiscal policy. The other obvious beneficiary is Germany, as financial markets will now actually pay the German government to take care of their money as the interest rate is negative.

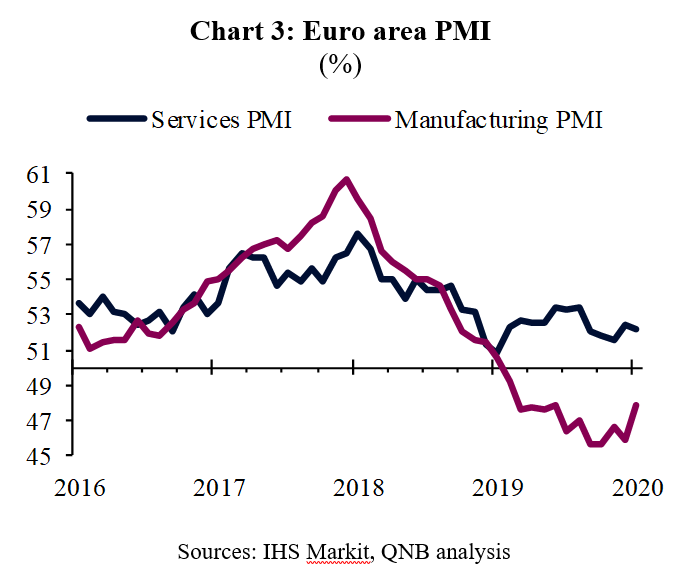

This stimulus from the ECB, together with the easing of global trade tensions with the Phase 1 deal to de-escalate the US-China trade war, have resulted in an improvement in leading indicators such as the Purchasing Managers Index (PMI).

The Euro area composite PMI for the Euro area has been rising since a low of 50.1 in September, reaching 51.3 in January. This masks a clear divergence between the weak performance of the manufacturing sector, which depends on external demand, and the more stable performance of the services sector, which depends more on domestic demand within the Euro area (Chart 3).

Unfortunately, this nascent recovery of the Euro area economy faces a new headwind in the form of the coronavirus that broke out it China at the end of 2019. Fortunately, there are only around 30 confirmed cases of the virus in Europe. However, China represents a significant source of demand for high-end manufacturing in Europe, so European exports will take a hit in Q1 for sure.

Europe’s manufacturers may also be exposed to some supply chain disruption caused by the virus. Estimates suggest the hit to Euro area growth may be as much as 0.2 percentage points (ppt), lowering our growth projection to 1.1% in 2020. The German economy is more sensitive and may see growth fall to as low as 0.8% in 2020.

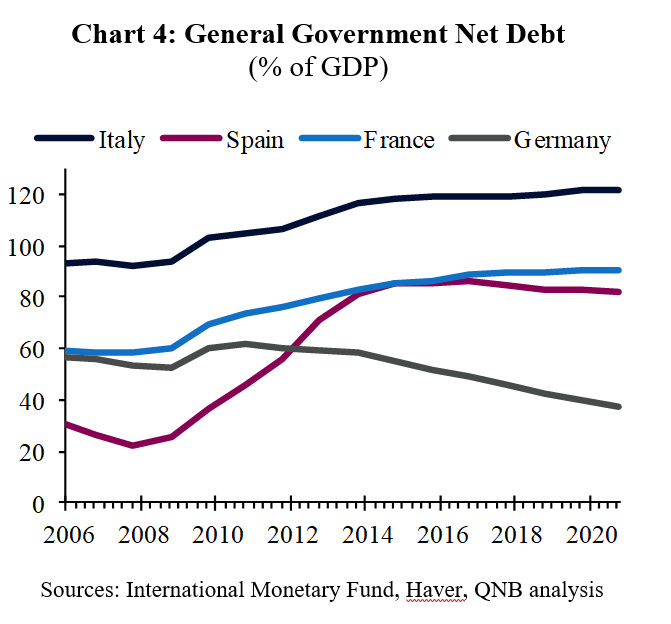

Fortunately, ultra-low interest rates have helped make Government debt levels much more sustainable across the Euro area (Chart 4). Indeed, Germany now has a lower level of Net Government Debt than before the 2008 global financial crisis.

Therefore, we expect that the persistently weak economic growth in the Euro area will allow the ECB to maintain monetary stimulus for longer and encourage governments to engage in fiscal stimulus.

Moreover, we hope the following four facts will provide political support for Germany to lead the way with fiscal stimulus. First, that the slowdown in GDP growth is most pronounced in Germany. Second, that the German government can borrow at negative interest rates.Third, the likelihood that Germany is most exposed to the shock from the virus. And finally, that German government Net Debt is low and has been falling consistently.

Download the PDF version of this weekly commentary in English or عربي