Since the beginning of the Covid-pandemic, the global economy experienced a series of extraordinary shocks that propelled inflation rates to levels that had not been seen in decades. By mid-2022, inflation reached 9.1% in the U.S., and a double-digit record of 10.7% in the Euro-Area. These levels were far from the 2% targets of monetary policy. Initially, central banks were hesitant to respond to spiralling prices, given the exceptional circumstances set by a worldwide pandemic, and the risk of a deeper economic collapse. However, it became apparent that high inflation was not a short-lived phenomenon, and policy makers reacted strongly to bring inflation rates down to their targets.

In the U.S., the Federal Reserve Board (FRB or “Fed”) increased its policy rates by 525 bps to 5.5%. The European Central Bank (ECB) embarked on a record tightening cycle, increasing its main refinancing rate by 450 basis points to 4.5%. Additionally, the central banks began to revert the large purchases of assets that had been implemented during the Covid-pandemic to inject liquidity into the financial system.

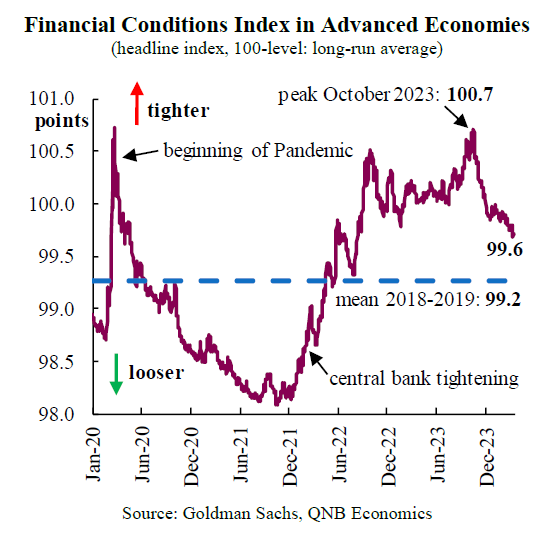

These monetary policies led to a tightening of financial markets in advanced economies. A useful measure is the Financial Conditions Index (FCI) for advanced economies, which provides a useful indicator by combining information of short- and long-term interest rates, as well as credit spreads and equity prices. The FCI indicated that markets were at their tightest in October 2023. However, as inflation rates consolidated their downward trends and positive inflation prints reassured analysts, markets began to assimilate the end of the monetary tightening cycles and financial conditions improved. In our view, although financial conditions will continue to improve this year on the back of policy rate cuts by the Fed and the ECB, they will remain in restrictive territory over the next several quarters. We discuss the two main factors that support our analysis.

First, although we expect major central banks to start cutting policy rates in 2024, they will be cautious in the pace of rate cuts. The latest readings of headline inflation have come down from their peaks of 9.1% and 10.7% respectively, in the U.S. and the Euro-Area, to 3.5% and 2.4%. Furthermore, inflation rates are expected to continue to converge towards the 2% targets amid weaker economic growth. In our view, this will allow the Fed to cut its policy rate by 50 bps to 5.0%, and the ECB by 100 bps to 3.5% by the end of the year. However, this pace of interest rate cuts implies that relatively high interest rates will remain in place over the next several quarters.

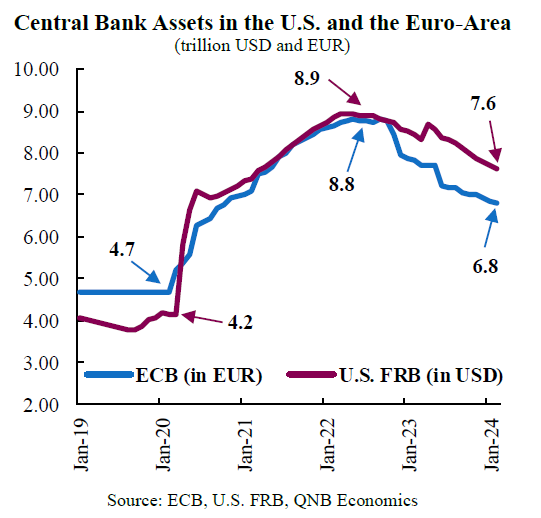

Second, the ECB and the Fed will continue to drain liquidity in the banking systems by reverting the balance sheet expansions that were put in place during the Covid-pandemic. To mitigate the consequences of the pandemic, central banks in advanced economies purchased large amounts of financial assets from the markets. This strategy, which is termed “quantitative easing” (QE), was implemented to inject liquidity in the financial system, as well as to contribute to lower long-dated interest rates.

In order to normalise the unprecedented size of its balance sheet that resulted from QE, the Fed began its reduction in June 2022, and has to date decreased its size by USD 1.3 trillion from the peak of USD 8.9 trillion. Similarly, the assets of the Eurosystem (the ECB plus the national central banks of the Euro-Area) have fallen by EUR 2 trillion from their peak of EUR 8.8 trillion. This process of normalisation will continue through 2024, reducing the excess liquidity in the financial system.

High interest rates and lower liquidity levels in the financial system restrain the availability of credit for the private sector. The latest bank lending surveys in the U.S. and the Euro-Zone show that commercial banks continue to tighten their lending standards. Furthermore, private sector credit volumes are contracting in the two largest advanced economies.

All in all, we expect that decreasing liquidity from the normalisation of central bank balance sheets and restrictive interest rates will maintain tight financial conditions over the next several quarters. This will limit the availability of credit for firms and households, and contribute to below-trend economic growth.

Download the PDF version of this weekly commentary in English or عربي