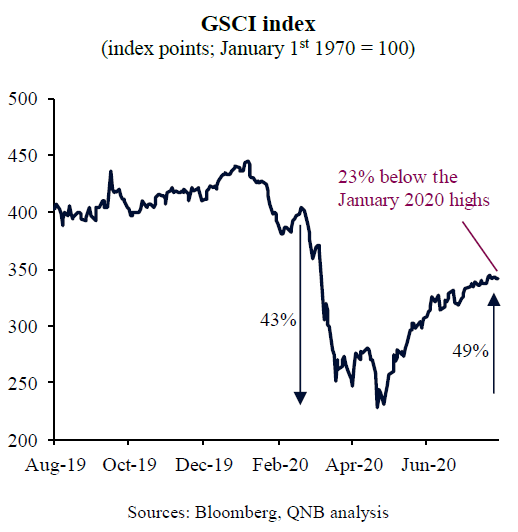

The fallout from the global spread of Covid-19 produced tremendous stress in commodity markets. The negative demand shock from the pandemic triggered deflationary pressures that rapidly pushed commodity prices to multi-decade lows. The Goldman Sachs Commodity Index (GSCI Index), a leading benchmark for general commodity price movements, which accounts for commodity index points since the 1970s, plummeted by almost 50% from January to late April 2020. During this period, falling prices were broad based, including energy, base metals, precious metals, grains, soft commodities and forest products.

But it is not all doom and gloom for commodities. After bottoming in April, the GSCI Index staged a significant recovery, re-gaining more than 50% of the recent losses by the time of writing. A closer look at such movements can shed light into important aspects of the ongoing global economic recovery.

The price development of key commodities conveys important macroeconomic information, including on sentiment and inflation trends, often leading or confirming cyclical turning points. Our analysis focuses on three main messages embedded into the recent recovery of commodity prices.

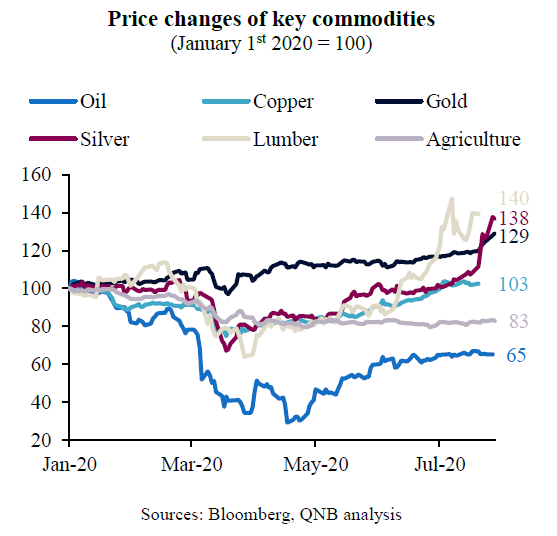

First, commodity prices confirm the recent success of monetary and fiscal authorities in stabilizing global economic conditions amid the Covid-19 shock. Liquidity measures and additional fiscal spending are already propping up aggregate demand, producing a recovery in activity. This is expressed in the rebound of highly cyclical commodities, including base metals, forest products and energy. Brent crude oil prices, while still significantly below the highs of January, are up by more than 123% from the lows of April. Copper and lumber prices, important proxies for activity in China and the US, have rebounded strongly to surpass the pre-Covid-19 January highs. Such price performance suggests that policymakers were able to bring deflationary pressures to a halt, which is a necessary condition for a lasting economic recovery.

Second, the price development of precious metals is pointing to further USD weakness. Gold prices have been recently outperforming long-dated US treasury bonds, suggesting that both foreigners and private domestic investors are favouring non-US issued safe-havens. Higher safe-haven demand for non-US assets such as gold implies lower potential demand for the USD. In fact, the US Treasury bond-to-gold ratio is an important proxy for USD sentiment, with a declining ratio often signalling a turning point of the USD cycle, from a USD bull market to a USD bear market that favours other currencies. A weaker USD is also a healthy sign of stronger non-US economic performance, and is particularly positive for emerging markets, given gains from both higher commodity prices and larger positive inflows of foreign capital.

Third, precious metals are also pointing to initial fears of inflation. Gold has reached all-time highs against all major currencies in recent months. Moreover, silver has advanced even more than gold, suggesting that global liquidity is quickly spilling over to the real economy, as silver is a key input for the new economy (technology and clean energy industries). A falling gold-to-silver ratio amid a strong gold performance across different currencies is a strong sign that inflation will pick up sooner rather than later. While this is a positive development after years of persistent deflationary pressures, this can only support a stable macro recovery if monetary and fiscal measures are maintained at adequate levels. An early withdrawal of policy stimulus would likely undermine the positive reflation story. On the other hand, too much stimulus for too long would potentially lead to disorderly inflation.

All in all, the recent recovery of commodity prices bodes well for the global economy. It indicates the beginning of a cyclical upswing and a much-needed breather for the strong USD. However, positive developments require an adequate continuation of policy stimulus. Monetary and fiscal measures should be well calibrated to maintain commodity prices supported, favouring a gradual and orderly pick up in inflation.

Download the PDF version of this weekly commentary in English or عربي